3 Computer Storage Device Stocks Poised for Significant Growth—Ideal Picks During Market Pullbacks

Recent Challenges in the Computer Storage Sector

Over the past month, the computer storage device industry has faced significant setbacks. Uncertainty surrounding the ongoing artificial intelligence (AI) market and escalating geopolitical tensions in the Middle East have contributed to rising crude oil prices and heightened inflation concerns.

Long-Term Opportunities Amid Short-Term Declines

Despite these headwinds, the sector is poised for growth thanks to robust trends in AI, cloud computing, the Internet of Things (IoT), automotive technology, connected devices, and virtual reality. Below, we highlight three storage device companies whose shares have dropped over 10% recently, yet still offer considerable upside potential.

- Western Digital Corp.

- Seagate Technology Holdings plc

- Sandisk Corp.

Western Digital Corp.: Riding the AI and Cloud Wave

Western Digital is capitalizing on surging demand for cloud and AI solutions. The company has experienced increased orders from data centers and greater adoption of high-capacity hard disk drives (HDDs), demonstrating its ability to deliver scalable, reliable storage tailored to the needs of the AI-driven data economy.

As AI and cloud technologies become more prevalent, the need for higher-density storage is growing. Western Digital is addressing this through partnerships with hyperscale clients, providing advanced drives that combine performance with cost efficiency. The company is pushing forward with innovations in areal density, accelerating its HAMR and ePMR development, and expanding its portfolio of UltraSMR drives.

Key Growth Drivers

Western Digital anticipates that the expansion of generative AI will trigger a refresh cycle for client and consumer devices, boosting content creation and storage across smartphones, gaming, PCs, and consumer electronics. Increased AI adoption is expected to drive demand for both HDD and Flash storage at the edge and core, opening up new business opportunities.

Enterprise SSD sales are rising due to their superior speed and reliability compared to HDDs. The growing volume of AI-generated data is fueling SSD market expansion and reshaping storage needs. Agentic AI is expected to further accelerate data growth, and Western Digital’s platform business is gaining traction with native AI companies and SaaS providers.

Financial Outlook

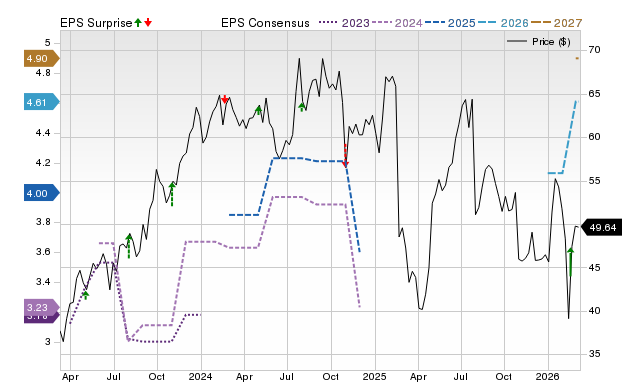

For the fiscal third quarter, Western Digital projects continued strength, supported by ongoing data center demand and broader adoption of high-capacity drives. The company expects non-GAAP revenues to reach $3.2 billion (plus or minus $100 million), marking a 40% increase year-over-year. Non-GAAP earnings per share are forecasted at $2.30 (plus or minus $0.15).

Analyst Upgrades and Price Targets

Western Digital is expected to see a revenue decline of 6.4% but an earnings increase of 81.7% for the current fiscal year ending June 2026. The Zacks Consensus Estimate for earnings has risen by 0.1% in the past month.

The average short-term price target from brokerage firms suggests a 29.8% upside from the last closing price of $245.25, with target prices ranging from $170 to $440. This implies a maximum potential gain of 79.4% and a possible downside of 30.7%.

Seagate Technology Holdings plc: Advancing Storage Solutions

Seagate Technology is also benefiting from heightened demand for cloud and AI storage. Management notes that modern data centers require solutions that balance performance and cost, a trend that aligns with Seagate’s strategic direction. The company’s focus on increasing areal density positions it well for sustained growth as AI-generated data continues to expand.

Future Growth Catalysts

Seagate’s production of high-capacity nearline drives is largely committed through 2026, with long-term contracts ensuring demand visibility into 2027. The company’s roadmap for aerial density provides a lasting total cost of ownership advantage for hard drives over competing technologies. Customers value Seagate’s HAMR drives as efficient solutions for growing AI-driven storage needs.

In September 2025, Seagate partnered with Acronis to deliver secure, scalable storage for AI-driven data growth. Their joint offering, Acronis Archival Storage, utilizes Seagate’s Lyve Cloud to provide enterprise-grade security, predictable costs, and compliance support for MSPs and regulated industries.

Financial Guidance

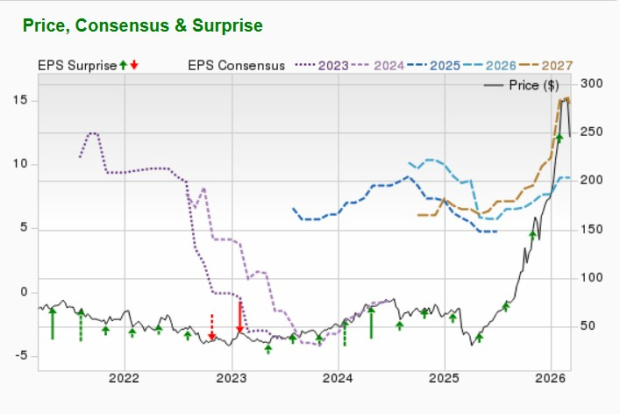

Seagate expects robust demand, especially from global cloud clients, to offset typical seasonal declines in Edge IoT markets. For the fiscal third quarter, projected revenues are $2.9 billion (plus or minus $100 million), representing a 34% year-over-year increase. Non-GAAP earnings per share are expected to be $3.40 (plus or minus $0.20), with operating expenses around $290 million and operating margins rising to approximately 30%. Free cash flow is anticipated to grow further in the March quarter.

Analyst Revisions and Price Targets

Seagate is forecasted to achieve revenue growth of 24.9% and earnings growth of 56.5% for the current fiscal year ending June 2026. The Zacks Consensus Estimate for earnings has improved by 0.4% over the past month.

The average short-term price target from brokers indicates a 32.4% upside from the last closing price of $352.80, with targets ranging from $270 to $700. This suggests a maximum upside of 98.3% and a downside of 23.5%.

Sandisk Corp.: Leveraging AI-Driven Storage Demand

Sandisk is thriving amid the shift toward AI computing, which requires much greater NAND flash storage compared to traditional workloads. AI models and inference applications generate vast amounts of data, necessitating high-performance enterprise SSDs and larger storage capacity in edge devices for on-device AI features.

This environment allows Sandisk to command premium pricing for its advanced products while maintaining disciplined supply management. In the fiscal second quarter, datacenter revenues soared 76% year-over-year, driven by adoption among cloud hyperscalers and enterprise clients.

Sandisk’s BiCS8 quad-level cell storage is progressing through qualification with two major hyperscalers and is expected to generate revenue soon. The extended joint venture with Kioxia Corporation through December 2034 strengthens Sandisk’s competitive position.

Positive Outlook and Financial Guidance

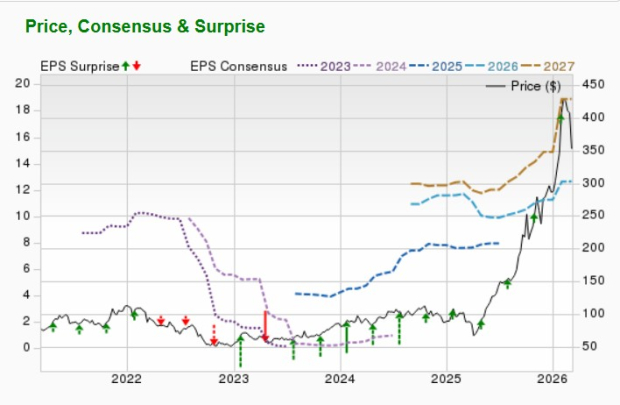

Sandisk projects continued growth for the third quarter of fiscal 2026, with expected revenues between $4.4 billion and $4.8 billion, marking another significant sequential increase. Gross margins are forecasted to expand to 65-67%, and earnings per share are expected to range from $12 to $14, reflecting strong pricing and an improved product mix. These results suggest that structural improvements in the NAND market are sustainable.

Analyst Upgrades and Price Targets

Sandisk is expected to achieve revenue growth of 94.1% and earnings growth exceeding 100% for the current year ending June 2026. The Zacks Consensus Estimate for earnings has improved by over 100% in the past two months.

The average short-term price target from brokers indicates a 32.9% upside from the last closing price of $527.33, with targets ranging from $235 to $1,000. This implies a maximum upside of 89.6% and a downside of 55.4%.

Five Stocks Poised for Significant Gains

Zacks experts have selected five stocks expected to potentially double in value over the next year. While not every pick will be a winner, past recommendations have delivered gains of 112%, 171%, 209%, and 232%.

Many of these stocks remain unnoticed by Wall Street, offering investors a unique opportunity to invest early.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Consensys-backed SharpLink reports $734 million loss as ETH holdings climb

Coeur Mining Shares Surge 340% Over the Last Year: What Factors Are Fueling This Growth?

JPY: Volatility shock could spur rebound – MUFG