MRVL Jumps 18.4% After Q4 Results: Should You Keep or Sell the Stock?

Marvell Technology's Recent Performance and Stock Movement

Shares of Marvell Technology (MRVL) have climbed 18.4% since the release of its fiscal fourth-quarter 2026 results on March 5. The company posted revenue of $2.22 billion for the quarter, marking a 22% increase compared to the same period last year.

For the fourth quarter, Marvell reported earnings of $0.80 per share, reflecting a 33.3% year-over-year improvement. Both revenue and earnings surpassed analyst expectations as measured by the Zacks Consensus Estimate.

Marvell Technology: Price, Analyst Estimates, and Earnings Surprises

With these strong results and the stock's recent rally, investors may be wondering whether now is the right time to buy, sell, or hold MRVL shares.

Surging Demand for Marvell's AI-Focused Solutions

Marvell Technology is benefiting from increased global investment in artificial intelligence infrastructure. The company's data center division saw a 46% year-over-year jump in fiscal 2026, surpassing $6 billion in revenue as major cloud providers and high-performance computing clients expanded their spending. This growth has fueled demand for Marvell's networking, optical interconnect, and custom silicon products.

The company is also capitalizing on the need for faster connectivity, such as 800G and 1.6T optical interconnects, which are becoming essential as AI workloads require rapid data transfer between GPUs and data centers. Marvell anticipates that its interconnect business will expand by over 50% in fiscal 2027, based on current momentum.

Marvell's custom silicon segment reached $1.5 billion in revenue for fiscal 2026 and is expected to grow further, driven by demand from hyperscale customers. New opportunities in areas like XPU integration, CXL memory expansion, and advanced networking are opening up additional revenue streams. Recent acquisitions, including Celestial AI and XConn Technologies, have enhanced Marvell's capabilities in AI networking and PCIe/CXL switching. Despite these advantages, the company faces several headwinds.

Challenges: Economic Uncertainty and Competitive Pressures

Marvell is navigating a complex environment marked by global economic and geopolitical risks. Ongoing trade disputes, changes in U.S. chip export policies, and tariffs pose challenges for the company, especially given its dependence on large cloud providers and international supply chains.

The company's rapid expansion in AI-related custom silicon is heavily reliant on a small group of hyperscale clients, creating a concentration risk. In the third quarter of fiscal 2026, data center sales accounted for 74% of total revenue, with over 90% of that tied to AI and cloud demand. Marvell also faces stiff competition from industry leaders such as Broadcom (AVGO), Astera Labs (ALAB), and Advanced Micro Devices (AMD).

- Broadcom is a major player in custom silicon for data centers, with advanced packaging technology that boosts AI chip performance and efficiency.

- AMD is well-established in the custom silicon and AI accelerator space, offering semi-custom SoCs and Instinct Accelerators for data centers.

- Astera Labs provides Leo CXL smart memory controllers, enabling memory expansion up to 2TB and enhancing AI and cloud computing performance.

These challenges, combined with a slowdown in Marvell's earnings growth over the past three quarters, have raised concerns among investors. The Zacks Consensus Estimate for the first quarter of fiscal 2027 points to 19.4% earnings growth, indicating a further deceleration. This estimate has been revised downward in the past week.

Image Source: Zacks Investment Research

Valuation: Marvell Stock Remains Expensive

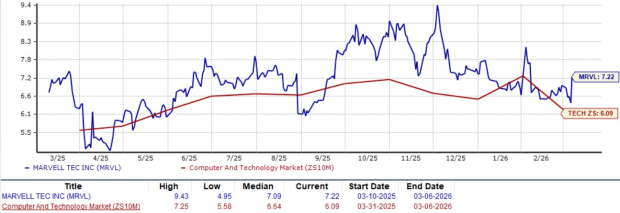

Marvell Technology currently trades at a forward price-to-sales ratio of 7.22, which is higher than the Computer and Technology sector average of 6.09, according to Zacks. The company's premium valuation is further reflected in its Zacks Value Score of D.

Forward 12-Month Price-to-Sales Valuation

Image Source: Zacks Investment Research

Final Thoughts: Caution Advised on MRVL Stock

While Marvell Technology has delivered impressive quarterly results and its shares have rallied on strong demand for AI-driven data center products, investors should be wary. The company faces significant risks from economic uncertainty, customer concentration, and fierce competition. Additionally, the ongoing slowdown in earnings growth and recent downward revisions to estimates suggest further challenges ahead. The stock also appears overvalued at current levels. Given these factors, it may be wise for investors to avoid Marvell Technology stock for now, as indicated by its Zacks Rank #4 (Sell).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

UNH Implements AI within Optum Rx to Address Pharmacy Fraud and Prevent Cost Losses

Hochschild Mining (HCHDF) Raised to Buy: Key Information You Need

Q4 Top Performers: Grocery Outlet (NASDAQ:GO) and Other Essential Retail Stocks

Netflix’s Pure-Play Growth Story Is Now on the Clock—Can It Justify the Rally?