CRWD shares jump 10% after Q4 earnings: Is it time to buy, sell, or hold?

CrowdStrike Shares Surge Following Strong Q4 Results

Shares of CrowdStrike Holdings (CRWD) have climbed 9.6% since the company released its fourth-quarter fiscal 2026 earnings on March 3. This uptick is largely due to the company exceeding expectations in its latest quarterly report.

For the fourth quarter of fiscal 2026, CrowdStrike posted non-GAAP earnings per share of $1.12, beating the Zacks Consensus Estimate by 1.6%. This figure also marks an 8.7% increase compared to the same period last year. Revenue for the quarter reached $1.31 billion, surpassing estimates by 0.68% and reflecting a 23.6% year-over-year growth.

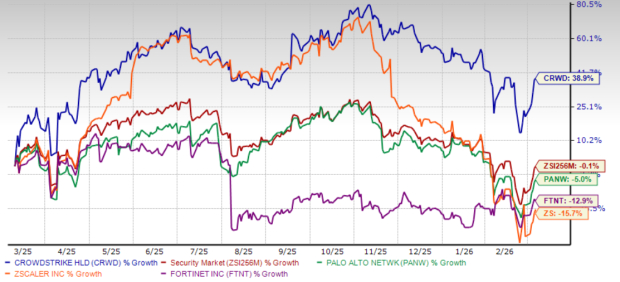

Over the past year, CrowdStrike’s stock has soared 38.9%, outperforming the Zacks Security industry, which saw a slight decline of 0.1%. The company has also outpaced competitors such as Palo Alto Networks (PANW), Zscaler (ZS), and Fortinet (FTNT), whose shares dropped 5%, 15.7%, and 12.9% respectively over the same period.

One-Year Price Return Performance

Image Source: Zacks Investment Research

The company’s impressive performance is fueled by robust demand for AI-powered cybersecurity solutions. With its stock outperforming both the industry and its peers, investors may wonder whether there’s further upside or if it’s time to lock in gains. Let’s take a closer look.

Falcon Flex Model Accelerates Subscription Growth

CrowdStrike’s subscription-based approach continues to drive its revenue growth. In the fourth quarter of fiscal 2026, the company achieved over $1 billion in revenue for the sixth straight quarter, representing a nearly 23% increase year over year. This success is partly due to the widespread adoption of the Falcon Flex Subscription Model, which enables customers to commit upfront and later select modules, streamlining the purchasing process.

By the end of the second quarter, half of CrowdStrike’s subscription clients were using at least six cloud modules. Additionally, 34% had adopted seven or more modules, and 24% were using eight or more as of January 31, 2026. In Q4, Annual Recurring Revenue (ARR) from Falcon Flex customers reached $1.69 billion, more than doubling from the previous year. Management highlighted that Falcon Flex has become a preferred method for clients to buy and expand their use of the Falcon platform.

The Falcon Flex model allows customers to quickly add new modules without lengthy contract negotiations, resulting in faster platform adoption. This has also led to a surge in contract expansions, with over 380 customers increasing their Flex agreements in Q4. The company added more than 350 new Flex customers during the quarter, ending fiscal 2026 with over 1,600 Falcon Flex adopters.

This flexible structure has paved the way for larger deals. For example, a major enterprise software client started with CrowdStrike’s threat intelligence module and, after embracing Falcon Flex, expanded to 25 modules, committing to a total contract value of $86 million.

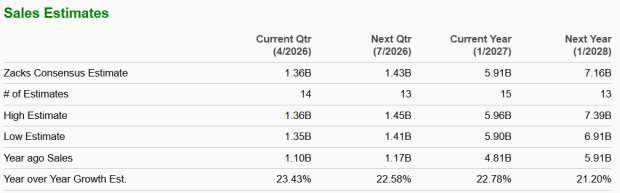

If these trends persist, Falcon Flex could remain a key growth engine for CrowdStrike into fiscal 2027 and beyond. According to Zacks Consensus Estimates, revenues are projected to grow by approximately 23% in fiscal 2026 and 21% in fiscal 2027.

Image Source: Zacks Investment Research

High Valuation Suggests Caution

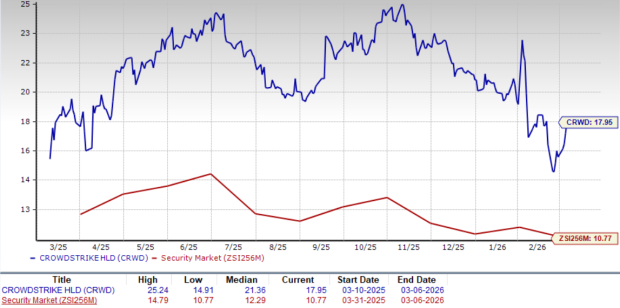

CrowdStrike’s stock currently trades at a premium price-to-sales (P/S) ratio, well above the industry average. Its forward 12-month P/S stands at 17.95, compared to the Zacks Security industry’s 10.77. The Zacks Value Score of F further indicates that CRWD shares may be overvalued at current levels.

Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

Compared to its peers, CrowdStrike’s P/S ratio is also higher. Palo Alto Networks, Fortinet, and Zscaler have forward P/S multiples of 10.79, 8.03, and 7.12, respectively.

Should You Hold CrowdStrike Stock?

As organizations continue to prioritize AI-driven security, CrowdStrike’s expertise in threat detection, response, and recovery positions it well for ongoing success. The company’s recurring subscription revenue model should help maintain steady growth, even in the face of economic and geopolitical uncertainties.

However, given the stock’s elevated valuation, investors may want to approach with caution.

CrowdStrike currently holds a Zacks Rank #3 (Hold). For a full list of today’s Zacks #1 Rank (Strong Buy) stocks, click here.

5 Stocks Poised to Double

Zacks experts have identified five stocks with the potential to gain 100% or more in the next year. While not every pick will be a winner, past selections have delivered gains of 112%, 171%, 209%, and even 232%.

Many of these stocks are still under the radar, offering investors a unique opportunity to get in early.

Discover these 5 high-potential stocks today >>

Looking for the latest stock recommendations from Zacks Investment Research? Download the 7 Best Stocks for the Next 30 Days for free. Get your copy here.

- Fortinet, Inc. (FTNT): Free Stock Analysis Report

- Palo Alto Networks, Inc. (PANW): Free Stock Analysis Report

- Zscaler, Inc. (ZS): Free Stock Analysis Report

- CrowdStrike (CRWD): Free Stock Analysis Report

This article was originally published by Zacks Investment Research.

Zacks Investment Research

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

EUR/USD: Sentiment pressure and fragile support – Scotiabank

Newmont’s Alpha Strategy: Ensuring Long-Term Cash Generation Through the Cerro Negro Investment

Trade Desk’s CTV solution aims for top-tier streaming advertising budgets

Consensys-backed SharpLink reports $734 million loss as ETH holdings climb