Should You Consider Purchasing, Retaining, or Selling Tempus AI Shares as 2026 Approaches?

Tempus AI’s Strategic Vision for 2026

Tempus AI (TEM) is charting a course for 2026 that emphasizes the expansion of its AI-powered precision medicine platform. The company aims to scale its diagnostics division, enhance its data and artificial intelligence infrastructure, and deepen collaborations with both healthcare providers and pharmaceutical firms. Backed by a robust commercial pipeline with contracts exceeding $1.1 billion in total value, Tempus has strong visibility into future revenue streams, supporting its ongoing growth momentum.

Financial Highlights and Segment Performance

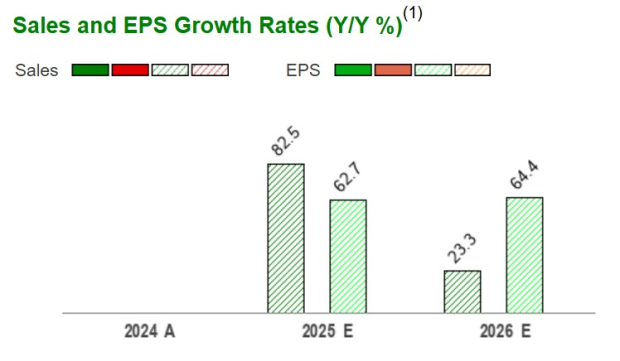

Tempus’ optimistic outlook is reinforced by impressive results in 2025. The company reported an 83.4% year-over-year surge in total revenue, reaching $1.3 billion. The Diagnostics segment led this growth, generating $955.4 million—a 111.5% increase—driven by higher demand for Oncology and Hereditary testing. Meanwhile, the Data and Applications segment saw revenues climb to $316.4 million, up 30.9% from the previous year, fueled by the success of its Insights data licensing business.

Industry Peers and Competitive Landscape

Other industry players, such as Inspire Medical Systems (INSP) and 10x Genomics (TXG), are also expected to maintain strong growth into 2026. Inspire Medical Systems continues to benefit from increased adoption of its sleep apnea devices, while 10x Genomics is advancing through growing interest in single-cell and spatial genomics technologies.

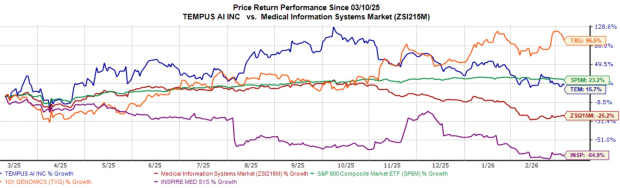

TEM Stock Performance Overview

Over the past year, shares of TEM have appreciated by 15.7%, marking a significant turnaround compared to the Zacks Medical Info Systems sector, which declined by 25.2%. In contrast, INSP’s stock dropped 64.9%, while TXG soared with a 96.5% gain. The S&P 500 also posted a 23.2% increase during this period.

Image Source: Zacks Investment Research

Oncology Diagnostics: A Key Growth Engine

Tempus anticipates robust expansion in its oncology diagnostics business, propelled by the growing use of genomic sequencing in cancer treatment. The company’s comprehensive test suite—including xT (DNA tumor profiling), xR (RNA profiling), xF (liquid biopsy), xH (hematologic cancer testing), and xE (whole exome sequencing)—is integrated with molecular and clinical data, leveraging AI to deliver actionable insights for physicians. Increasing adoption among healthcare professionals further supports this growth.

Currently, Tempus partners with more than 5,500 hospitals and 8,500 oncologists who regularly utilize its tests, embedding insights directly into clinical workflows. Broader trends toward precision oncology and genomic testing are also fueling demand for sequencing-based diagnostics. These factors position Tempus to sustain approximately 30% annual growth in its core oncology diagnostics segment.

Expanding Minimal Residual Disease (MRD) Testing

Another strategic priority for Tempus is scaling its Minimal Residual Disease (MRD) testing, which detects lingering cancer cells post-treatment. MRD test volumes grew 56% quarter-over-quarter in Q4 2025, despite limited commercialization as only a fraction of the sales team is currently focused on this product. The company is gradually expanding MRD’s market presence while working to secure broader reimbursement, aiming to make MRD a significant growth contributor as coverage improves.

Advancing Clinical Applications and Healthcare Software

Tempus is also investing in clinical applications and healthcare software for providers. Key initiatives include TIME, an AI-powered solution for streamlining clinical trial enrollment in oncology, and Next, an AI-driven platform for optimizing care pathways. Additional AI-based decision support tools are under development, offering clinicians actionable insights and expanding Tempus’ footprint within hospital systems. These efforts also generate valuable clinical data, further enhancing the company’s data and AI ecosystem.

Revenue and Earnings Outlook

According to Zacks Consensus Estimates, Tempus is projected to achieve a 25.4% increase in revenue for 2026. While earnings per share are expected to remain negative, they are anticipated to improve by 39.3% compared to 2025.

Challenges Facing Tempus AI

Geopolitical tensions, particularly between Iran and the United States, could disrupt global medical supply chains, cause logistical delays, and drive up raw material and energy costs due to volatile oil prices. These risks may also result in fluctuating medicine prices and increased regulatory complexity as international pressures impact trade and operations.

Despite reporting positive adjusted EBITDA, Tempus continues to post GAAP losses, primarily due to significant stock-based compensation, higher amortization from the Ambry acquisition, and a one-time debt extinguishment loss. As a result, profitability remains reliant on non-GAAP measures, and the absence of GAAP net loss guidance makes it difficult to predict when the company will achieve sustained GAAP profitability.

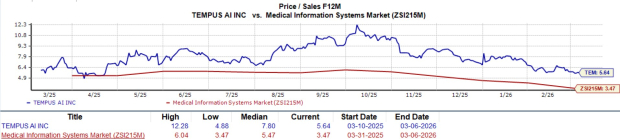

Valuation: Is TEM Overpriced?

Tempus shares appear expensive, as indicated by a Value Score of F. The stock trades at a 12-month forward price-to-sales ratio of 5.64, which is above the industry median of 5.47.

Investment Considerations for TEM

Although Tempus AI is experiencing strong revenue growth and expanding its role in precision medicine, the current risk-reward balance may not favor investors. The stock’s premium valuation, coupled with geopolitical and cost-related headwinds, could pose challenges for the broader medical sector.

With earnings estimates trending negatively and limited clarity on when profitability will improve, the current valuation leaves little margin for error. Investors might consider taking profits and reallocating funds to more attractive opportunities, as reflected by the Zacks Rank #4 (Sell) rating for TEM.

For a full list of today’s Zacks #1 Rank (Strong Buy) stocks, click here.

5 Stocks Poised to Double

Zacks experts have identified five stocks with the potential to gain 100% or more in the coming year. While not every pick will be a winner, past recommendations have delivered returns of 112%, 171%, 209%, and 232%.

Many of these stocks are not yet widely recognized on Wall Street, offering investors a chance to get in early.

Looking for the latest stock recommendations from Zacks Investment Research? Download the 7 Best Stocks for the Next 30 Days for free. Get your free report here.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

2 Motives to Consider TTMI and 1 Reason for Caution

Oil is now the hottest topic on Crypto Twitter