NVO Stock Loses Close to $50 Billion in Market Value Over a Month: Is It Time to Sell?

Novo Nordisk Faces Steep Market Decline

Over the past month, Novo Nordisk (NVO) has seen its stock price tumble by 22%, erasing close to $50 billion in market value. This sharp downturn follows a wave of disappointing clinical trial results and mounting pricing challenges, effectively wiping out most of the gains achieved since the 2021 approval of its flagship obesity drug, Wegovy (semaglutide).

Intensifying Rivalry with Eli Lilly

Eli Lilly (LLY) has solidified its position as Novo Nordisk’s primary challenger in the GLP-1 obesity treatment space. Since its 2023 approval, Lilly’s Zepbound (tirzepatide) has steadily captured market share from Wegovy, thanks to clinical evidence showing greater weight-loss effectiveness. Despite launching after Wegovy, Zepbound’s superior results have made it a formidable competitor.

Clinical Setbacks for Novo Nordisk

In February, Novo Nordisk reported that Zepbound’s 15 mg dose outperformed its own next-generation candidate, CagriSema (cagrilintide/semaglutide), in the 84-week phase III REDEFINE 4 trial. Patients on Zepbound lost 25.5% of their body weight, compared to 23% for CagriSema, causing Novo Nordisk’s drug to fall short of its primary goal and giving Lilly a decisive advantage.

These results underscore Zepbound’s stronger efficacy and represent a significant hurdle for Novo Nordisk as it attempts to regain ground in the obesity market. Although Novo Nordisk has submitted CagriSema for FDA review and is planning further studies, Zepbound currently holds a clear lead in direct comparisons.

Lilly’s Expanding Lead in Diabetes and Obesity

Lilly has also reported that its oral GLP-1 candidate, orforglipron, outperformed Novo Nordisk’s Rybelsus (oral semaglutide) in the phase III ACHIEVE-3 trial for type 2 diabetes. Orforglipron not only delivered greater reductions in A1C and weight over 52 weeks, but also improved cardiovascular risk markers and offered the convenience of no food or water restrictions, further strengthening Lilly’s position in the cardiometabolic field.

Pricing Pressures and Margin Concerns

In response to competitive pressures, Novo Nordisk plans to significantly lower U.S. list prices for Wegovy, Ozempic, and Rybelsus to $675 per month starting January 2027. While this move aims to broaden patient access, it could also squeeze profit margins as competition from Lilly intensifies.

Challenges Impacting Novo Nordisk’s Growth Outlook

With demand slowing, competition heating up, pricing under pressure, rising operational costs, and few near-term growth drivers, Novo Nordisk’s prospects are weakening on several fronts. To better understand the company’s position, let’s examine its strengths and vulnerabilities.

Semaglutide Remains Novo Nordisk’s Key Revenue Source

The company’s success has largely been built on the sales of Ozempic and Rybelsus for type 2 diabetes, and Wegovy for obesity. Novo Nordisk boasts one of the most comprehensive portfolios in diabetes and obesity care.

Ozempic and Wegovy continue to be major contributors to revenue. Novo Nordisk is working to expand Wegovy’s reach through partnerships with major U.S. pharmacies, telehealth services, and both proprietary and third-party platforms, aiming to ensure patients have access to authentic, FDA-approved treatments. These efforts are expected to address the issue of compounded alternatives by 2026. The company is also investing in new manufacturing facilities to boost production capacity for its current and future GLP-1 therapies.

Expanding Indications and Approvals

Novo Nordisk is broadening the use of semaglutide with new indications. Wegovy is now approved for reducing major cardiovascular events, alleviating symptoms of heart failure with preserved ejection fraction (HFpEF), and easing osteoarthritis-related knee pain in obese patients. The company has also launched oral Wegovy—the first GLP-1 pill for weight management—in the U.S. as of early 2026.

Rybelsus has received expanded labeling in the U.S. and EU to include cardiovascular benefits for type 2 diabetes patients. A 7.2 mg dose of Wegovy, which demonstrated up to 25% weight loss in the STEP UP study, has been approved in the EU and is under review in the U.S. Novo Nordisk is also seeking to expand Ozempic’s label to include treatment for peripheral artery disease.

Competition from Eli Lilly Remains Fierce

Eli Lilly’s tirzepatide-based products, Mounjaro (for type 2 diabetes) and Zepbound (for obesity), have quickly become top revenue generators, capturing significant market share from Novo Nordisk. In 2025, these two drugs generated a combined $36.5 billion in sales, accounting for about 56% of Lilly’s total revenue.

Expanding Beyond GLP-1: Rare Diseases and Liver Care

Novo Nordisk is also growing its presence in rare diseases, having filed for U.S. approval of Mim8 for hemophilia A and secured both U.S. and EU approvals for Alhemo to treat hemophilia A and B. Additionally, the FDA has granted accelerated approval to Wegovy as the first GLP-1 therapy for noncirrhotic metabolic dysfunction-associated steatohepatitis with moderate-to-advanced liver fibrosis, marking a milestone in liver disease treatment.

Advancing Next-Generation Obesity Treatments

The company is actively developing several new obesity therapies, particularly for the U.S. market. In addition to CagriSema, Novo Nordisk is preparing to launch a late-stage program evaluating cagrilintide as a standalone obesity treatment. The company is also moving amycretin, another next-generation candidate, into phase III trials for weight management, and is studying oral monlunabant in mid-stage obesity trials. Novo Nordisk has entered into major partnerships, including a $2.2 billion deal with Septerna and a $2.1 billion agreement with Vivtex, to develop innovative oral medicines for obesity, diabetes, and related conditions.

Stock Performance, Valuation, and Analyst Estimates

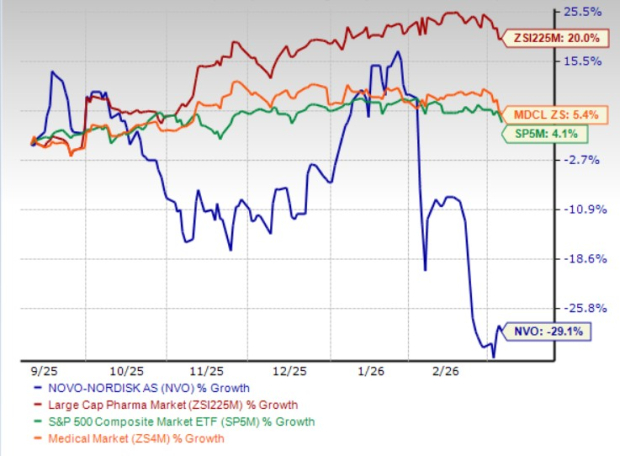

Over the last six months, Novo Nordisk’s stock has dropped 29.1%, significantly underperforming both its industry peers and the S&P 500, as illustrated below.

Source: Zacks Investment Research

The company’s shares are currently trading at a lower valuation compared to the industry average. Based on the price-to-earnings ratio, Novo Nordisk trades at 11.59 times forward earnings, well below the industry’s 17.90 and its own five-year average of 29.25.

Source: Zacks Investment Research

Analyst forecasts for 2026 earnings have slipped from $3.54 to $3.35 per share over the past two months, while 2027 estimates have fallen from $3.75 to $3.26 in the same period.

Source: Zacks Investment Research

Investment Outlook: Should You Buy, Hold, or Sell?

Given the mounting challenges, Novo Nordisk’s near-term prospects look uncertain. The company, currently rated as a Zacks Rank #4 (Sell), is contending with fierce competition from Eli Lilly’s expanding GLP-1 portfolio, unfavorable clinical comparisons, pricing headwinds, and declining earnings projections. With the obesity and diabetes markets becoming more crowded and few immediate growth catalysts, investor sentiment is likely to remain cautious. Short-term investors may want to avoid the stock until there is greater clarity on competitive dynamics, pricing, and pipeline progress.

Longer-term risks are also increasing. Novo Nordisk’s heavy reliance on the semaglutide franchise exposes it to market share losses, potential exclusivity challenges, and growing innovation-driven competition. Meanwhile, investments in its drug pipeline may take years to yield substantial returns. Ongoing estimate reductions, slowing growth in key markets, and an uncertain competitive landscape in obesity and diabetes all cast doubt on the sustainability of its earnings growth. Although the stock now trades at a discount, this appears to reflect weakening fundamentals rather than a compelling buying opportunity.

Rising Competition from Emerging Players

The obesity treatment market is attracting new entrants beyond the established leaders. Smaller biotech companies like Viking Therapeutics (VKTX) are developing GLP-1–based therapies to challenge the incumbents. Viking’s dual GIPR/GLP-1 receptor agonist, VK2735, is being developed in both oral and injectable forms for obesity, with plans to advance the oral version into phase III trials in the third quarter of 2026.

5 Stocks Poised for Major Gains

Each of these stocks was selected by a Zacks expert as a top pick with the potential to double in value over the next year. While not every recommendation will be a winner, past selections have delivered impressive returns of +112%, +171%, +209%, and +232%.

Many of these companies remain under the radar, offering investors a chance to get in early.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Bitway (BTW) 24-Hour Amplitude Reaches 88.0%: Speculative Rally Driven by Over $170 Million Surge in Trading Volume

Rocket Lab Surges 21.9% Over the Last Three Months: Is Now the Time to Invest?

Missouri's Cryptocurrency Tax Reduction: An Analytical Overview