TTD Drops 25% Over the Last Three Months: What’s the Best Way to Approach This Stock?

The Trade Desk: Recent Stock Performance and Market Context

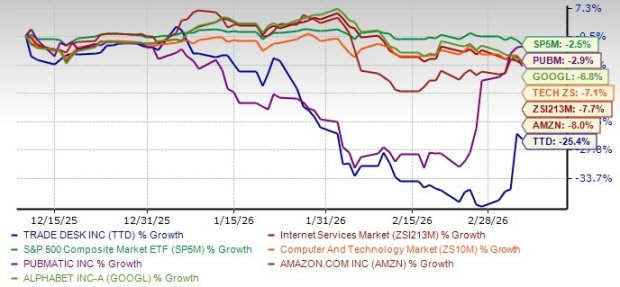

The Trade Desk (TTD), a major player in digital advertising technology, has experienced a significant decline, with its stock dropping 25.4% over the last quarter. This notable decrease comes despite the company's reputation as a leader in the ad tech industry.

Stock Movement Overview

This downward trend is not unique to The Trade Desk; the broader digital advertising sector has also been under pressure. The Zacks Internet Services industry index fell by 7.7% during the same period. Additionally, the Zacks Computer & Technology sector and the S&P 500 composite posted losses of 7.1% and 2.5%, respectively.

Given these declines, investors are left to consider whether the recent sell-off presents a potential buying opportunity for TTD shares.

Let’s take a closer look at what this recent performance means for those interested in The Trade Desk.

Long-Term Growth Drivers for The Trade Desk

Despite recent stock volatility, several factors continue to support The Trade Desk’s long-term outlook. These include the growth of connected TV (CTV), expansion in retail media, advancements in artificial intelligence (AI) and the Kokai platform, international expansion, and supply-chain improvements such as OpenPath. The company’s focus on the open internet—where competition and price discovery thrive—remains central to its strategy, with expectations that open platforms will continue to gain ground over closed advertising systems.

Rising digital ad spending in CTV, especially for premium content and live sports, is a major growth engine. The shift toward auction-based CTV advertising is accelerating, offering advertisers more flexibility and control compared to traditional models. CTV is now among The Trade Desk’s fastest-growing segments, with video (including CTV) making up about half of its business in Q4 2025.

Retail media is another rapidly expanding area. Over the past five years, The Trade Desk has partnered with global retailers to build what it calls the world’s largest and most comprehensive retail data marketplace. Management reports that participating retailers account for over half of global retail sales.

The company’s emphasis on AI is also paying off. Leadership sees the combination of proprietary AI tools and platform neutrality as a key differentiator.

Kokai, The Trade Desk’s next-gen AI-powered demand-side platform (DSP), is now the default for nearly all clients, further strengthening its competitive position. For example, IKEA was able to cut its cost per acquisition by 17% through Kokai’s AI-driven omnichannel optimization.

Another notable innovation is Audience Unlimited, which addresses advertiser concerns about the high cost and uncertain effectiveness of third-party data. Using AI, Audience Unlimited ranks third-party data segments for campaign relevance, drawing from hundreds of trusted sources. Instead of paying for each data segment individually, advertisers receive access to all relevant data at a simplified, lower rate, enabling precise targeting at scale without unpredictable costs.

Initiatives like OpenPath, Deal Desk, and OpenAds further enhance The Trade Desk’s ecosystem by directly connecting advertisers and publishers, improving transparency and supply-chain efficiency.

International growth is also accelerating, with markets outside North America expanding at a faster pace. The company reports strong momentum in EMEA and APAC, the result of years of investment. Currently, international business accounts for about 16% of total revenue, offering significant room for future expansion.

The Trade Desk has also deepened relationships with major advertisers through Joint Business Plans (JBPs), which represented over half of its business by the end of 2025, with the pipeline more than doubling year-over-year.

As digital advertising increasingly shifts toward AI-driven, results-focused campaigns, The Trade Desk’s strong cash position ($1.3 billion in cash and equivalents, with no debt) provides stability amid economic uncertainty. The company’s expanded $500 million share buyback program is another positive for investors.

Challenges and Risks Facing The Trade Desk

Spending on digital advertising is sensitive to broader economic trends. If macroeconomic conditions worsen, The Trade Desk’s revenue growth could be impacted by weaker demand for programmatic advertising.

The company has noted sluggish demand in key sectors such as consumer packaged goods and automotive, which remained weak in the fourth quarter and are expected to stay soft into 2026.

While The Trade Desk remains a leading independent DSP, competition is intensifying. Major platforms like Meta, Apple, Alphabet (GOOGL), and Amazon (AMZN) dominate the market by controlling their own inventory and user data, enabling highly targeted campaigns. The CTV space is also becoming more crowded, with smaller players like Magnite and PubMatic (PUBM) ramping up their efforts. Amazon’s growing DSP business is a particularly strong competitor in this area.

Expanding internationally brings its own set of challenges, as operating across diverse markets can be complex and risky. Regulatory changes and stricter privacy laws, such as the phase-out of cookies and Europe’s GDPR, add further complications.

The company’s commitment to integrating AI throughout its offerings will increase capital and operational expenditures. Management expects adjusted EBITDA margins in 2026 to be similar to 2025, as investments in AI, product development, and go-to-market strategies continue.

Although The Trade Desk is still growing, its growth rate has slowed compared to previous years. Fourth-quarter revenue rose 14%, but first-quarter growth is projected at 10%.

Valuation: TTD’s Current Pricing

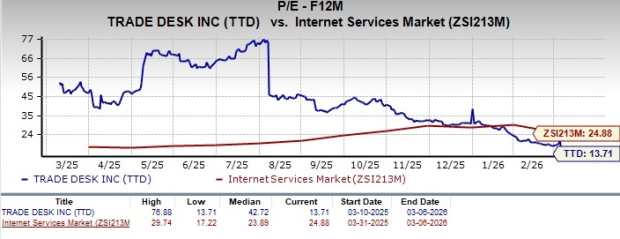

Looking at forward price-to-earnings ratios, The Trade Desk is trading at 13.71 times earnings, which is below the Internet Services industry average of 24.88.

For comparison, Amazon, PubMatic, and Alphabet are trading at 26.44x, 32.4x, and 25.04x earnings, respectively.

Over the past year, shares of Amazon, Alphabet, and PubMatic have declined by 8%, 6.8%, and 2.9%, respectively.

Final Thoughts: Is The Trade Desk a Buy, Sell, or Hold?

While The Trade Desk benefits from several long-term growth drivers—including the expansion of CTV, retail media, and the adoption of Kokai—short-term uncertainties remain. These include economic headwinds, rising costs, and increased competition from both major platforms and independent ad tech firms.

Given the company’s solid fundamentals but challenging near-term outlook, current shareholders may choose to hold their positions, while new investors might consider waiting for a more attractive entry point.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Nicox (NICXF) Raised to Buy: The Reasons Explained

BMY Wins FDA Nod to Expand Sotyktu Label for Psoriatic Arthritis

Monitoring gas and oil prices amid rising tensions in Iran conflict