EMCOR Stock Slides 12% Post Q4 Results: Buy the Dip or Wait?

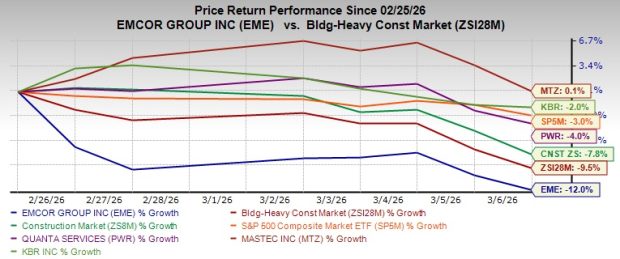

EMCOR Group, Inc. EME tumbled 12% since reporting its fourth-quarter 2025 earnings performance, underperforming the Zacks Building Products - Heavy Construction industry, but outperforming the broader Construction sector and the S&P 500 Index.

In the fourth quarter of 2025, the adjusted earnings and revenues of this Connecticut-based infrastructure service provider were $7.19 per share and $4.51 billion, topping the Zacks Consensus Estimate by 7.6% and 5.4%, respectively. On a year-over-year basis, the metrics grew 13.8% and 19.7%, respectively, attributable to strong demand in core end markets, including network and communications, water and wastewater, manufacturing and industrial. (read more: EMCOR's Q4 Earnings & Revenues Beat Estimates, Operating Margin Up Y/Y)

The investors’ sentiments are expected to have pulled back on a relatively conservative 2026 outlook, with the operating margin indicating a year-over-year decline despite robust market trends for public infrastructure projects.

Notably, since Feb. 26, EME stock has also underperformed a few of the renowned market players, including MasTec, Inc. MTZ, Quanta Services, Inc. PWR and KBR, Inc. KBR. During the said time frame, MasTec inched up 0.1%, while Quanta and KBR declined 4% and 2%, respectively.

Image Source: Zacks Investment Research

Factors Boosting EMCOR’s Growth

Strong Market Demand: Given the peak phase of the United States’ public infrastructure funding initiative, the demand across multiple sectors, particularly network and communications, institutional, water and wastewater, and manufacturing and industrial, has been robust. EMCOR has been witnessing increased activity in the network and communications sector, particularly data center construction projects, which is the largest market sector for the electrical construction business. Owing to these tailwinds, during 2025, revenues from the U.S. Electrical Construction and Facilities Services segment increased 51.8% year over year to $5.07 billion, while U.S. Mechanical Construction and Facilities Services revenues grew 10.1% to $7.05 billion.

Expanding demand across healthcare, manufacturing and industrial, institutional, and commercial markets also remains robust, reflecting broad-based construction activity across the United States. As of Dec. 31, 2025, Remaining Performance Obligations (RPOs) reached a record $13.25 billion, indicating 31% year-over-year growth, with acquisitions contributing about $1.61 billion. Overall, strong public infrastructure spending in the United States is currently benefiting EMCOR and is expected to support its growth over the medium and long term. Besides EME, these strong market trends also benefit its close peers, including Quanta, MasTec and KBR.

Strategic Inorganic Actions: EMCOR mainly indulges in acquisitions, with primary focus on smaller private businesses with strong management teams. However, apart from expanding its capabilities, geographic reach and exposure to high-growth markets, the company also focuses on streamlining its business for increasing efficiency.

On the acquisition front, during 2025, EMCOR acquired Florida-based Miller Electric (for $868.6 million cash) under its U.S. Electrical Construction and Facilities Services segment, strengthening its large-scale electrical construction capabilities and expanding its presence in the Southeast and Texas. In addition to Miller Electric, EMCOR acquired nine other companies for a total of $182.1 million. On the divestiture front, to further enhance its financial flexibility and ensure core focus on the U.S. operations, on Dec. 1, 2025, EME announced the sale of its U.K. Building Services operations (EMCOR Group (UK) plc) to the OCS Group UK Limited for a total value of approximately $250 million.

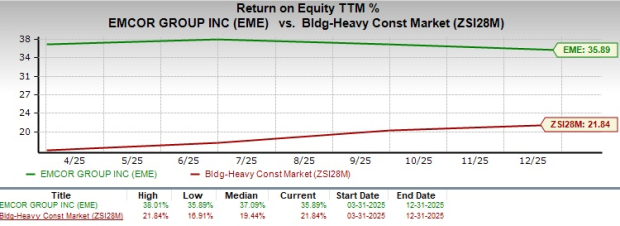

Ensuring Shareholder Value: One of EMCOR’s strengths lies in its utilization of its extra cash efficiently, be it for business expansion or shareholder value. The company has a current trailing 12-month ROE of 35.9%, which compares favorably with the industry's ROE of 21.8%. The factor mentioned above indicates the company’s efficiency in using its shareholders’ funds, along with its ability to generate profit with minimum capital usage.

Image Source: Zacks Investment Research

During 2025, EME returned $45 million through dividends and $586.3 million through share repurchases to its shareholders.

Earnings Estimate Revision of EME

EME’s earnings estimates for 2026 and 2027 have moved upward in the past seven days to $28.27 and $31.67 per share, respectively. The estimates for 2026 and 2027 imply year-over-year growth of 9.3% and 12.1%, respectively.

Image Source: Zacks Investment Research

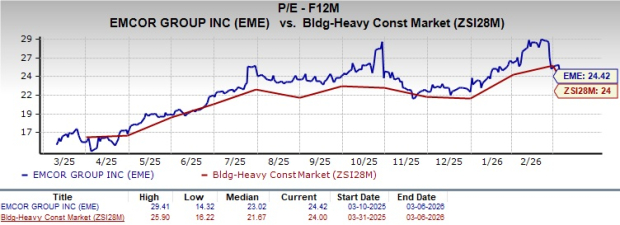

EME’s Premium Valuation

EME stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 24.42, as evidenced by the chart below.

Image Source: Zacks Investment Research

What is Pulling Down EMCOR’s Prospects

Macro Risks: EMCOR is sailing through an uncertain macro environment despite witnessing robust public infrastructure demand trends. Higher interest rates, geopolitical tensions and energy price volatility continue to create an unpredictable business environment. These factors can delay capital spending by customers and slow construction activity across several end markets. Besides, EMCOR serves customers across several industries, including commercial construction, manufacturing, healthcare, energy and government sectors. These industries are highly sensitive to economic conditions and capital spending cycles. The company’s revenue growth, therefore, depends heavily on the timing and funding of new project awards.

Conservative 2026 View: During the fourth-quarter 2025 financial results, EME posted a rather conservative 2026 outlook, as the market suggests, given the strong market fundamentals backing its near and mid term growth prospects. For 2026, EMCOR expects annual revenues to be in the band of $17.75-$18.5 billion compared with $16.99 billion reported in 2025. EPS is expected to be within $27.25-$29.25 compared with $28.19 reported in 2025. Operating margin is expected to be between 9% and 9.4%, down from 10.1% reported in 2025.

Does EME Stock Possess Any Upside Potential?

EMCOR remains supported by strong end-market demand across network and communications, data center construction, manufacturing, healthcare and water infrastructure, with RPOs up 31% year over year. Strategic acquisitions, including Miller Electric, and the divestiture of its U.K. business, are expected to streamline operations and strengthen the company’s focus on higher-growth U.S. markets. In addition, EMCOR’s strong balance sheet, robust cash generation and shareholder-friendly capital allocation continue to support long-term value creation.

However, EME’s outlook for 2026 implies some margin normalization after a strong 2025, which has tempered short-term sentiment. Macro uncertainties, project timing risks and a premium valuation also limit immediate upside potential.

While a strong backlog, improving earnings estimates and solid infrastructure demand support its long-term growth outlook, EMCOR stock’s near-term upside may remain modest until margin visibility improves. Thus, it is prudent for the existing investors to hold onto this Zacks Rank #3 (Hold) stock for now. New investors are advised to wait for now and look for a better entry point when the trends start favoring EME stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

2 Motives to Consider TTMI and 1 Reason for Caution

Oil is now the hottest topic on Crypto Twitter