3 Reasons to Steer Clear of WSO and One Alternative Stock Worth Buying

Watsco’s Recent Stock Performance

Watsco shares are currently valued at $393.14 each, and over the past six months, the stock has experienced a modest decline of 2.2%. During the same timeframe, the S&P 500 advanced by 4.8%, meaning Watsco has lagged behind the broader market.

Should investors consider adding Watsco to their portfolios, or does it pose unnecessary risk?

Reasons We Expect Watsco to Underperform

Our outlook for Watsco is cautious. Below are three key factors that lead us to believe there are more attractive investment options than WSO, along with a stock we prefer.

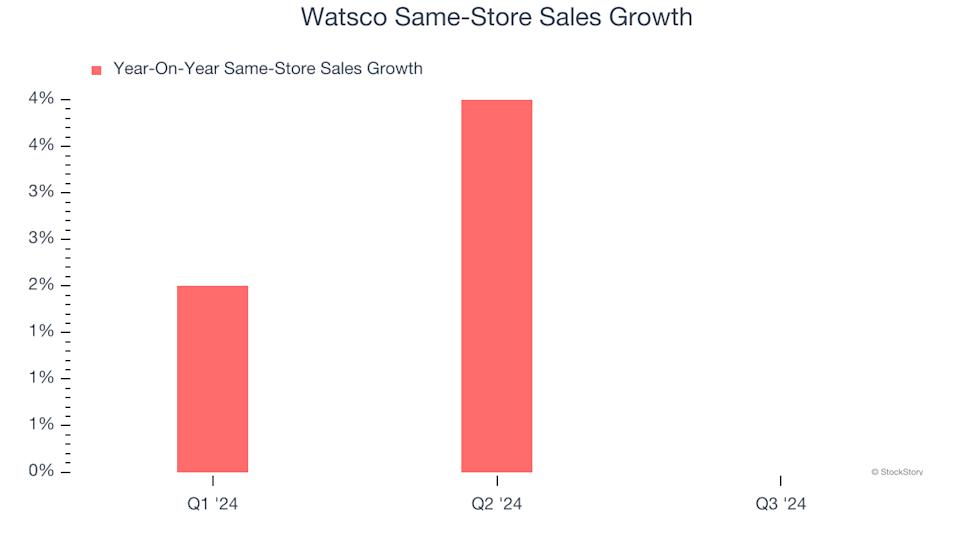

1. Same-Store Sales Growth Trails Industry Peers

Same-store sales, which track revenue changes at established locations open for at least a year, provide insight into a company’s core demand. For infrastructure distributors like Watsco, this metric is particularly telling.

In the past two years, Watsco’s same-store sales have grown by an average of just 2% annually. This lackluster growth suggests the company may need to reconsider its approach or pricing, which could disrupt its operations.

Watsco Same-Store Sales Growth

2. Earnings Per Share Have Declined

While long-term earnings trends are important, short-term EPS changes can reveal shifts in a company’s performance. Over the last two years, Watsco’s EPS has dropped by an average of 5.8% per year, even as revenue remained flat. This indicates the company has had difficulty adapting to fluctuating demand.

Watsco Trailing 12-Month EPS (Non-GAAP)

3. Declining ROIC Signals Unsuccessful Investments

Return on invested capital (ROIC) measures how efficiently a company generates operating profit from its capital base. While high ROIC is attractive, the direction of this metric is often more important for stock performance.

Unfortunately, Watsco’s ROIC has seen a notable decline in recent years. Although management has made strong decisions in the past, the downward trend in returns may reflect a shortage of profitable growth opportunities.

Watsco Trailing 12-Month Return On Invested Capital

Our Verdict

We appreciate companies that strive to improve their customers’ lives, but in Watsco’s case, we’re choosing to remain observers. The stock has underperformed the market recently and currently trades at a forward P/E of 32.1 (or $393.14 per share), suggesting that much optimism is already reflected in the price. We believe there are more compelling opportunities available. For example, consider a rapidly expanding restaurant franchise known for its top-rated ranch dressing.

Alternative Stocks Worth Considering

WHILE YOU’RE HERE: Discover 9 Top-Performing Stocks. The most successful stocks consistently outpace the market, boasting strong revenue growth, increasing free cash flow, and exceptional returns on capital. These companies have already earned the market’s recognition.

But according to our AI-driven platform, their growth stories are far from over. See which 9 stocks made our list this week—absolutely free.

Our selections include well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Comfort Systems, which delivered a 782% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Medline (MDLN) Q4 Net Sales Rise 14.8% to $7.8B Following Completion of IPO

H.C. Wainwright Reiterates Buy Rating on BigBear.ai (BBAI)

Neumora Therapeutics (NMRA) Positioned to Capitalize on Blockbuster Opportunity

C4 Therapeutics (CCCC) Well Positioned With Cemsidomide Trial Data