Primerica (PRI): Should You Buy, Sell, or Keep After Q4 Results?

Primerica Stock: Recent Performance and Investor Considerations

In the past half-year, Primerica's stock price has dropped to $257.38, resulting in a 5.2% decline. This stands in sharp contrast to the S&P 500, which has gained 4.8% over the same period. Such underperformance may leave shareholders wondering about their next steps.

With this recent dip, is Primerica (PRI) now a smart investment?

What Makes Primerica a Topic of Discussion?

Primerica (NYSE: PRI) operates with a network of more than 140,000 licensed representatives, all working as independent contractors. The company specializes in term life insurance, investment solutions, and other financial products, serving middle-income families across the United States and Canada.

Key Strengths of Primerica

Exceptional Return on Equity Signals Strong Growth Potential

Return on equity (ROE) is a crucial indicator of how effectively an insurance company turns shareholder capital into profits. Firms with consistently high ROE tend to reward investors with better returns, thanks to prudent capital allocation.

Primerica has maintained an average ROE of 27.7% over the past five years. This figure is well above the industry average of 12.5%, and companies exceeding 20% are considered top performers. Such results highlight Primerica's competitive edge in its sector.

A Notable Concern

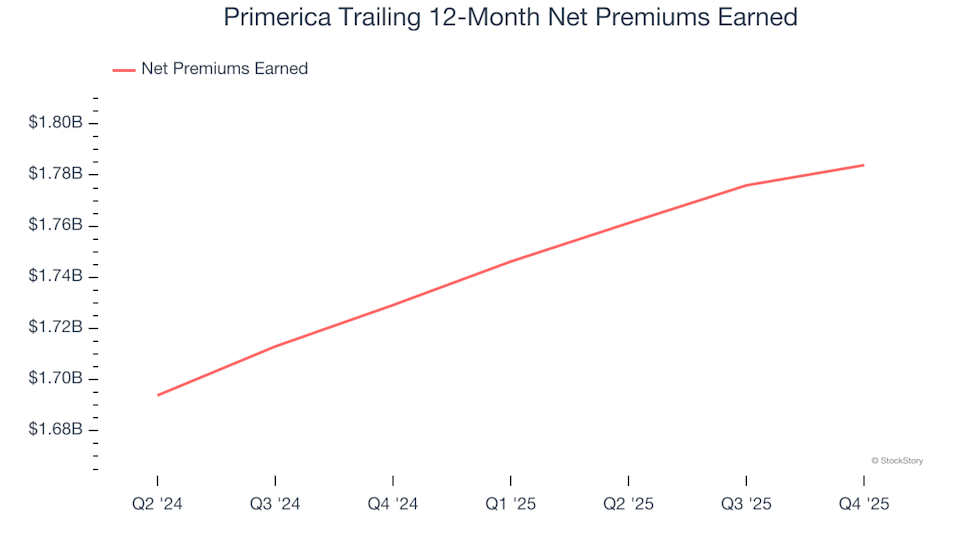

Sluggish Growth in Net Premiums Earned

Insurance providers often use reinsurance to shield themselves from large or unexpected losses, passing some of their risk to other insurers. Net premiums earned reflect the total premiums collected, minus those transferred to reinsurers.

Over the last two years, Primerica's net premiums earned have grown at an annualized rate of just 3.7%. This pace lags behind both the broader insurance industry and the company’s own overall revenue growth.

Primerica Trailing 12-Month Net Premiums Earned

Overall Assessment

Despite some challenges, Primerica's strengths appear to outweigh its weaknesses. Following the recent decline, the stock is trading at 3.2 times its forward price-to-book ratio, or $257.38 per share. Is this a buying opportunity?

Other Stocks With Even Greater Potential

Don't Miss: Top 5 Growth Stocks

Many of the market’s biggest winners, such as Meta, CrowdStrike, and Broadcom, shared one trait before their meteoric rise: explosive revenue growth. Our AI identified all three, which have since delivered returns of 315%, 314%, and 455%, respectively.

Curious about which five stocks are on our radar this month?

Our recommendations have included well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Tecnoglass, which achieved a 1,754% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gold prices rise but remain rangebound with focus on Iran war de-escalation

Iran’s IRGC warns it could block oil exports if US, Israel attacks continue

Solana maintains $1,45 billion in ETF flows while the price targets $100.

Oil prices fall and Dow Jones, S&P 500 and Nasdaq futures decline.