HCA Healthcare Shares Surge on Analyst Upgrades and Dividend Hike as Trading Volume Soars to $790M Ranking 177th in Market Activity

Market Snapshot

HCA Healthcare (HCA) surged 2.31% on March 9, 2026, as trading volume spiked 97.82% to $0.79 billion, ranking 177th in the day’s market activity. The stock’s performance followed a series of analyst upgrades and a dividend increase, though management highlighted potential near-term EBITDA headwinds. The company’s market capitalization stands at $119.33 billion, with a price-to-earnings ratio of 18.80 and a 12-month price range of $310.18 to $552.90.

Key Drivers

Zacks Research’s revised Q1 2026 earnings estimate of $7.11 (up from $6.93) and a $33.18 full-year 2027 forecast provided a near-term boost to HCA’s stock. The firm maintained a “Hold” rating despite the upward revision, reflecting cautious optimism about the company’s ability to meet its FY2026 guidance of $29.10–$31.50 in earnings per share. HCAHCA-- also announced a quarterly dividend hike to $0.78 (or $3.12 annually), signaling confidence in its capital return strategy. These actions align with the company’s broader focus on long-term growth, including a $10 billion stock repurchase authorization and expanded capital expenditures, which analysts view as supportive of shareholder value.

Analyst sentiment remained largely bullish, with 16 “Buy” ratings and eight “Hold” ratings, driving a consensus price target of $534.50. Institutional investors reinforced this optimism, with entities like Swiss National Bank and National Pension Service increasing their stakes in Q3 2025. However, insider sales by executives such as Michael Cuffe and Michael McAlevey—totaling $7.8 million over 90 days—introduced some ambiguity. While these transactions did not directly impact the stock’s valuation, they highlighted internal uncertainty amid broader market volatility.

The stock’s gains were tempered by risks flagged by management, including $600–$900 million in potential EBITDA headwinds from insurance-exchange and state payment changes. These challenges, combined with slightly below-estimate revenue growth in the prior quarter ($19.51 billion vs. $19.67 billion), underscored near-term operational pressures. Zacks Research’s trimmed FY2028 EPS forecast and Morgan Stanley’s “Underweight” rating further reflected skepticism about long-term margin expansion despite strong short-term earnings.

Demographic tailwinds, however, remain a key long-term catalyst. MarketBeat and analysts highlighted HCA’s positioning to benefit from the aging U.S. population, with the company’s FY2026 EBITDA guidance and expanded healthcare infrastructure seen as critical to capturing demand for inpatient and outpatient services. This narrative was reinforced by positive coverage from Argus, Barclays, and Deutsche Bank, which raised price targets to $560, $551, and $558, respectively.

While HCA’s stock price and analyst ratings suggest confidence in its strategic direction, the interplay of near-term operational risks and long-term demographic opportunities will likely dictate its trajectory. Investors remain focused on the company’s ability to navigate insurance and regulatory shifts while maintaining its dividend and repurchase programs, which are pivotal to sustaining shareholder returns in a competitive healthcare landscape.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Iran’s Oil Embargo Strategy Ignites Intense Energy Power Play in Global Trade

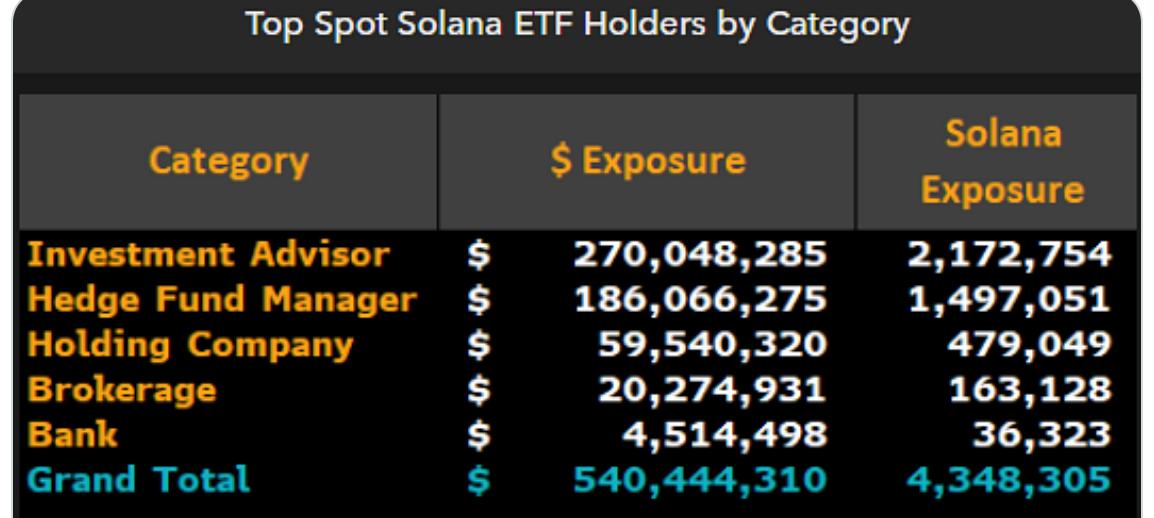

Wall Street funneled $540M into US Solana ETFs in Q4: Bloomberg

European freight truck makers brace for wave of low-cost Chinese rivals