China’s iron ore imports jump due to policy-induced early purchases rather than a rebound in demand — Trade stockpiling rises ahead of potential quota implementation

Iron Ore Imports Surge Amid Structural Weakness in China’s Steel Sector

China’s recent spike in iron ore imports must be understood within the context of a deeper, ongoing transformation: the country’s appetite for steel is steadily diminishing. This is not a short-term fluctuation, but rather a significant change in China’s industrial landscape. The clearest evidence is the decline in steel output—2025 saw China produce only 960.1 million metric tons of crude steel, the lowest in seven years and the first time production has dipped below one billion tons since 2019. This drop, a result of deliberate efforts to reduce excess capacity, marks a turning point for the industry.

Looking forward, prospects for steel consumption remain bleak. After a sharp 5.4% decrease in 2025, demand is forecasted to fall another 1% this year. The main culprit is the ongoing downturn in the property sector, which has long been a cornerstone of steel demand. Although the government is redirecting infrastructure spending toward sectors like transportation and high-tech manufacturing—which use less steel—these efforts are not enough to counterbalance the slump in traditional construction. As a result, domestic steel consumption is contracting, even as exports reach new highs.

This disconnect between robust exports and weakening local demand is crucial. Despite exporting a record 119.02 million tons of steel in 2025, profit margins for Chinese steelmakers have narrowed. This margin squeeze highlights the fragility of the domestic market; mills are forced to sell overseas at lower prices to clear excess inventory, underscoring the lack of local demand. The resilience in iron ore imports is therefore more about restocking and supporting export-driven production than any real recovery in China’s core economy. The bearish outlook for iron ore is rooted in the expectation that domestic weakness will persist, keeping long-term prices in check even as global supply grows.

Policy-Driven Inventory Buildup: Anticipating Export Quotas

The latest jump in iron ore imports is best explained by inventory strategies, not a resurgence in steel demand. The trigger is a new regulatory framework: as of January 2026, China introduced an export quota system for steel and related products. This policy requires exporters to secure quotas, motivating mills to accelerate production and shipments before restrictions fully take hold. In anticipation, steelmakers are ramping up output and exports, driving a surge in raw material imports.

This restocking trend is evident in trade data. While finished steel exports have started to slow, iron ore imports have soared—January saw a 10% year-on-year increase to 105 million metric tons, with February up another 7%. In contrast, finished steel exports dropped 8.1% year-on-year in the first two months. This divergence shows that mills are importing more iron ore to produce steel for export, but the overall volume of exports is shrinking. This points to a temporary, policy-induced inventory build, rather than a genuine rebound in global demand for Chinese steel.

This scenario creates a cyclical imbalance. Mills are stockpiling iron ore ahead of the quota system, which may help buffer against future export limits. However, this front-loading is happening against a backdrop of weak domestic demand and a controlled reduction in steel output. The policy is simply shifting production and inventory cycles forward, without addressing the underlying pressures on steel margins and consumption. As a result, the current import surge is likely to be short-lived, fading as the quota system stabilizes and domestic weakness resurfaces.

Market Dynamics and the Outlook for Sustainability

The sustainability of this import boom depends on market forces that suggest it is a short-term phenomenon. Globally, iron ore shipments rose 8% year-on-year in January and February, but nearly all of this growth was driven by China. Shipments to other regions increased only modestly—1% in January and 11% in February, mainly to Japan, Korea, and Europe. This concentration underscores that the surge is unique to China and not reflective of a broader global upswing.

Within China, the picture is more nuanced. Record imports are being matched by rising inventories, creating a bearish technical setup. Elevated stockpiles, combined with significant put options activity in derivatives markets, signal limited potential for price increases ahead of the usual restocking season. The market appears to have already priced in the front-loading of demand, leaving little room for further gains unless there is a fundamental shift in consumption.

The long-term bearish outlook remains unchanged. New, high-quality supply from Guinea’s Simandou mine is beginning to enter the market, and its influence is expected to grow. This additional supply, together with seasonal constraints that limit Brazilian exports during the wet season, will reshape the Atlantic iron ore market. Over time, this increased supply flexibility could ease market tightness and cap prices, even as China’s domestic demand continues to weaken. For now, the import surge is a cyclical inventory event. Concentrated flows, high inventories, and the prospect of new supply all suggest that this is a temporary anomaly, likely to dissipate as policy-driven front-loading ends and structural demand pressures return.

Key Factors to Monitor

The central question is whether the import surge is a short-lived inventory adjustment or the start of a broader cyclical shift. The answer depends on several critical indicators that will reveal the underlying trend.

- Steel Production Trends: Monitor Chinese steel output for signs of ongoing restocking versus a one-off inventory build. Evidence shows crude steel production hit a seven-year low in 2025, and this downward trend is expected to persist. If the import surge is cyclical, it should eventually lead to higher output. If production remains subdued or declines further, it confirms the surge is policy-driven, not a sign of demand recovery. Recent data already show imports rising while finished steel exports fall, indicating front-loading is underway.

- Impact of Export Quotas: The new quota system, launched in January, requires exporters to apply for quotas covering at least 100 steel products. Early evidence suggests mills are rushing to export before restrictions tighten. The key is whether this leads to a sustained increase in exports or a sharp drop once the system is in place. If trade flows quickly normalize, it will confirm the temporary nature of the import spike. If the quota system creates lasting bottlenecks, it could reshape trade flows for years.

- New Supply Dynamics: Track the pace of new supply as the Atlantic market adjusts. The Simandou mine in Guinea has begun shipping, with 344,000 metric tons sent in January alone. This new supply, combined with seasonal limits on Brazilian exports, will influence the global iron ore market. Faster-than-expected increases in Simandou shipments or an early end to Brazil’s wet season could ease market tightness and cap prices, even as Chinese demand wanes. High port inventories in China suggest the market is already anticipating this new supply, which could further limit price gains.

In summary, the current surge in iron ore imports is a cyclical inventory event, not a fundamental shift in demand. The factors above will determine whether this episode fades quietly or triggers a broader adjustment in the market.

Strategy Spotlight: Absolute Momentum Long-only Approach

This momentum-based strategy for IAU involves entering positions when the 252-day rate of change is positive and the price is above the 200-day simple moving average. Exits are triggered if the price falls below the 200-day average, after 20 days, or if a take-profit of +8% or a stop-loss of −4% is reached.

Backtest Summary

- Strategy Return: 74.44%

- Annualized Return: 29.67%

- Maximum Drawdown: 10.21%

- Profit-Loss Ratio: 0.81

Trade Analysis

- Total Trades: 16

- Winning Trades: 13

- Losing Trades: 3

- Win Rate: 81.25%

- Average Hold Days: 14.19

- Max Consecutive Losses: 1

- Average Win Return: 6.07%

- Average Loss Return: 6.46%

- Max Single Return: 11.42%

- Max Single Loss Return: 10.21%

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Blackstone-owned AirTrunk secures record $1.24B loan for Tokyo AI data center

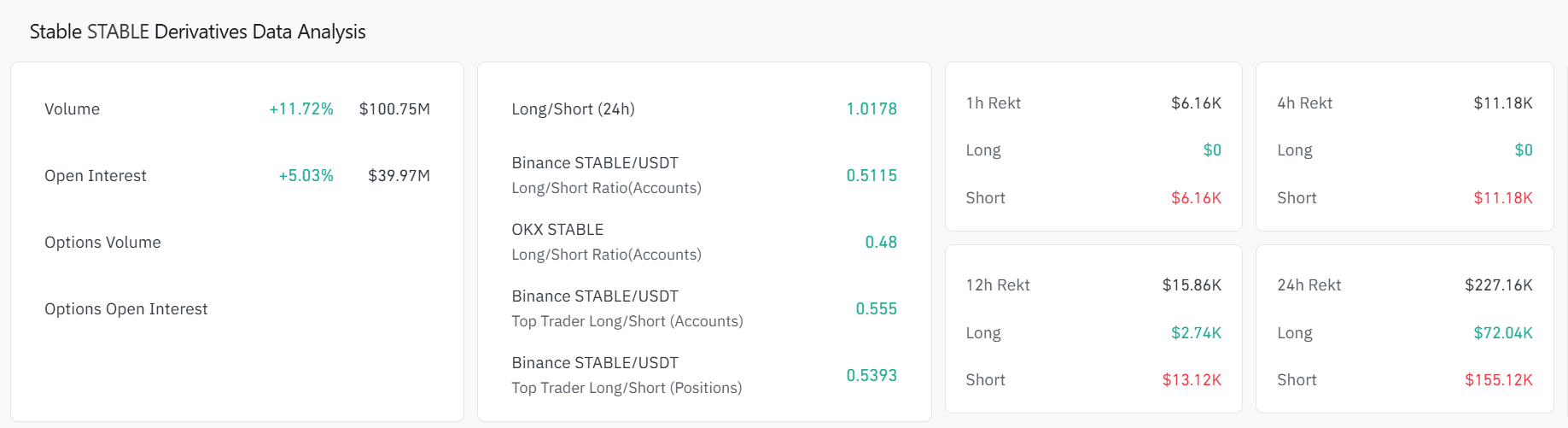

STABLE surges 14% – Here’s how shorts can trigger another rally

Sharplink Reports $734 Million Loss: An Accounting Outcome Influenced by Pricing

AUD/USD is starting to target this year's peak as market sentiment improves