ABM (NYSE:ABM) Surpasses Q4 CY2025 Projections

ABM Industries Q4 CY2025 Financial Overview

ABM Industries (NYSE:ABM), a leading provider of facility services, posted fourth-quarter revenue that surpassed analyst forecasts, reaching $2.24 billion—a 6.1% increase compared to the same period last year. However, adjusted earnings per share came in at $0.83, falling short of consensus expectations by 4.8%.

Curious whether ABM is a good investment right now?

Quarterly Highlights

- Revenue: $2.24 billion, beating analyst projections of $2.20 billion (6.1% year-over-year growth, 2.1% above estimates)

- Adjusted EPS: $0.83, below expectations of $0.87 (4.8% shortfall)

- Adjusted EBITDA: $117.8 million, compared to estimates of $126.7 million (5.3% margin, 7% under projections)

- Management reaffirmed its full-year Adjusted EPS guidance at $4 (midpoint)

- Operating Margin: 3.3%, consistent with the prior year’s quarter

- Free Cash Flow: $48.9 million, a significant improvement from -$122.9 million a year ago

- Organic Revenue: Up 5.5% year-over-year

- Market Cap: $2.54 billion

Scott Salmirs, President and CEO, commented, “ABM has started fiscal 2026 on a strong note, achieving robust organic revenue growth of 5.5% and notable gains in operating and free cash flow.”

About ABM Industries

Founded in 1909 as a window cleaning business, ABM Industries now delivers integrated facility management, infrastructure, and mobility solutions to sectors such as commercial, manufacturing, education, and aviation.

Revenue Trends

Consistent sales growth over time is a hallmark of a resilient business. While any company can have a few strong quarters, those with sustained expansion stand out.

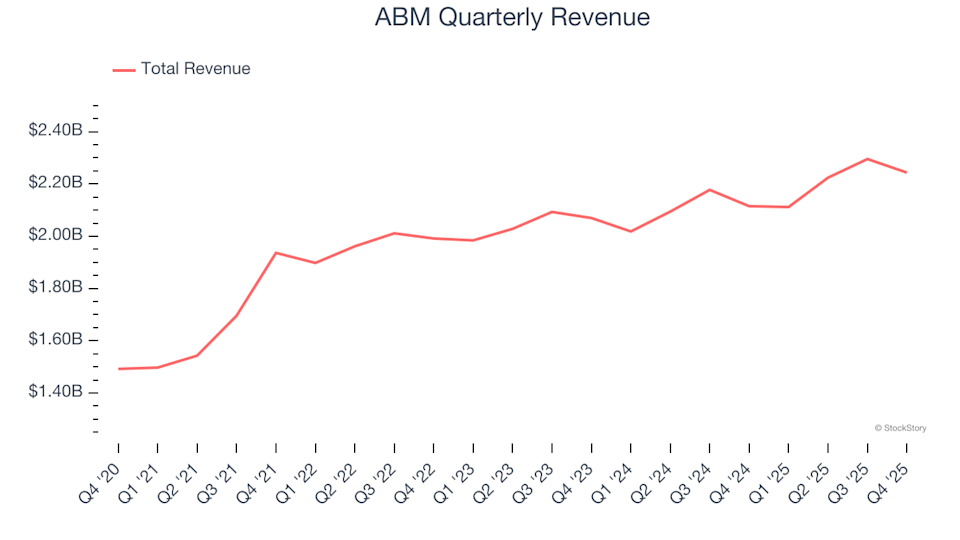

ABM generated $8.87 billion in revenue over the past year, positioning it among the largest players in the business services space. Its established reputation gives it an edge in influencing customer choices.

Over the past five years, ABM’s sales have grown at an annualized rate of 8.6%, indicating steady demand and providing a solid foundation for further analysis.

While long-term growth is crucial, a five-year perspective may overlook recent shifts or innovations. ABM’s latest results show a slowdown, with annualized revenue growth of 4.2% over the past two years—below its five-year average. This deceleration could reflect changing customer preferences and low barriers to switching providers in the industry.

Examining organic revenue, which excludes acquisitions and currency effects, ABM’s core business averaged 3.6% year-over-year growth over the last two years. This aligns with its overall revenue trend, suggesting that its main operations—not external factors—drove performance.

Recent Performance and Outlook

This quarter, ABM’s revenue increased 6.1% year-over-year, exceeding Wall Street’s expectations by 2.1%.

Looking forward, analysts anticipate ABM’s revenue will grow by 4.5% over the next year, mirroring its recent pace. This forecast suggests that new offerings may not significantly boost top-line growth in the near term.

Bonus Insight: Three Emerging Platforms Outpacing Amazon, Google, and PayPal

Amazon, Google, and Meta succeeded by dominating overlooked markets, building strong competitive advantages, and scaling rapidly. Now, three new platforms are following this strategy. Early investors in these companies could see substantial gains.

Profitability: Operating Margin

ABM’s operating margin has remained relatively steady, averaging 3.6% over the past five years. This level of profitability is considered weak for the industry and is largely due to its less-than-optimal cost structure.

Despite revenue growth, ABM’s operating margin has not improved, raising questions about its ability to leverage fixed costs and achieve greater efficiency.

This quarter, ABM reported an operating margin of 3.3%, matching last year’s figure and indicating stable expenses.

Earnings Per Share Analysis

Tracking earnings per share (EPS) over time helps assess whether a company’s growth translates into profitability. ABM’s EPS has increased at a modest 2.1% annualized rate over the past five years, lagging behind its revenue growth. The unchanged operating margin suggests that factors like interest and taxes have impacted net earnings.

In the last two years, ABM’s annual EPS declined by 2.4%, reflecting ongoing underperformance.

For Q4, adjusted EPS was $0.83, down from $0.87 a year ago and below analyst expectations. Wall Street projects ABM’s full-year EPS will rise to $3.39 over the next 12 months, representing a 20% increase.

Summary of Q4 Results

ABM exceeded forecasts for organic revenue and overall sales this quarter, but missed on EPS. The mixed results led to a 2.4% rise in the stock price, closing at $44.34 after the announcement.

Should you consider investing in ABM now? The latest quarter is just one aspect of the company’s long-term quality. Evaluating both business fundamentals and valuation is key to making an informed decision.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Meta purchased Moltbook, the AI-driven social platform that gained widespread attention due to fabricated posts

Here’s Why The PNC Financial Services Group (PNC) Is an Excellent Choice for ‘Buying the Dip’ Right Now

Crescent Capital BDC (CCAP) May Soon Establish Support—Reasons to Consider Purchasing the Stock Now

BankUnited (BKU) Displays 'Hammer Chart Pattern': Is It an Opportunity to Buy at the Bottom?