MELI Declines 13% in a Month: Should You Hold or Fold the Stock?

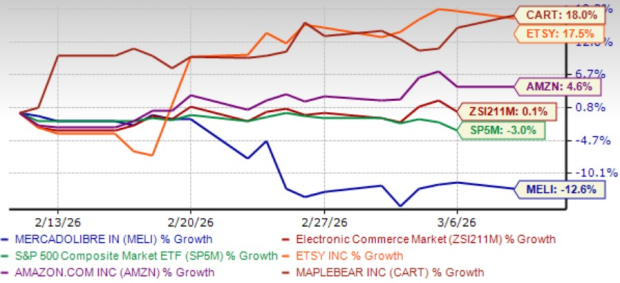

MercadoLibre’s MELI shares have lost 12.6% in the past month, much wider than the S&P 500 composite’s decline of 3% and the Internet – Commerce industry’s marginal 0.1% growth.

MercadoLibre’s recent decline reflects a few key investor concerns. The company continues to invest heavily in logistics, technology and financial services, which is putting pressure on margins in the near term. At the same time, the rapid expansion of its lending business increases the potential for credit risk if economic conditions weaken. In addition, broader macroeconomic volatility across Latin America could affect consumer spending and overall business performance, adding another layer of uncertainty for investors.

MercadoLibre has also lagged several of its peers, such as Maplebear Inc. CART, Etsy ETSY and Amazon AMZN. Over the same time frame, shares of Maplebear, Etsy and Amazon have gained by 18%, 17.5% and 4.6%, respectively.

The stock's recent decline has raised questions about investors' future performance. A closer look at the company’s strengths and challenges can help determine whether the dip is a risk or an opportunity for investors.

One Month Price Performance

Image Source: Zacks Investment Research

Aggressive Investments Weigh on MELI Margins

MercadoLibre’s recent profitability trends reflect the company’s deliberate strategy of investing heavily to strengthen its ecosystem and pursue long-term growth opportunities. Its operating income growth has been affected by substantial spending on strategic initiatives across commerce and fintech. In the fourth quarter of 2025, operating income reached $889 million, but margins declined 340 basis points year over year as the company stepped up investments in logistics, credit expansion and other growth initiatives. However, these investments aim to enhance market share and reinforce its competitive advantages throughout Latin America.

A major source of margin pressure stems from strategic initiatives, including lowering the free-shipping threshold in Brazil, expanding cross-border trade, scaling its first-party retail operations and accelerating the rollout of credit cards. The combined impact of these initiatives reduced operating margins by roughly five to six percentage points in the fourth quarter of 2025.

MELI’s Earnings Estimate Revision Trend Lower

MELI’s earnings estimate revisions reflect a downward trend, indicating cautious sentiment. The Zacks Consensus Estimate for first-quarter 2026 earnings is pegged at $11.11 per share, which has declined 17.9% over the past 30 days. A similar trend is seen for the full year 2026, as the estimate has been revised 0.5% downward over the same period to $59.21 per share.

Image Source: Zacks Investment Research

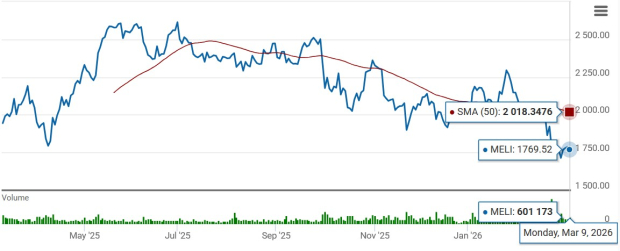

MELI is also trading below the 50-day moving average, indicating a bearish trend, suggesting limited upside in the near-term momentum for the stock.

MELI Trades Below 50-Day SMA

Image Source: Zacks Investment Research

Although these challenges exist, it does not imply that the company’s prospects are entirely negative.

MELI Gains From Rising Cross-Border Trade

MercadoLibre is benefiting from the rapid expansion of cross-border trade, which represents a significant long-term growth opportunity for the company. In Latin America, cross-border e-commerce is estimated to be a $10 billion market, where MercadoLibre currently holds only a small share but sees substantial room for expansion. To capture this opportunity, the company has been improving its value proposition by enabling easier access to free shipping on cross-border purchases, allowing buyers to build baskets across international products and offering more flexible pricing structures for sellers.

MercadoLibre’s cross-border initiatives are delivering encouraging results. Cross-border trade growth accelerated throughout 2025, culminating in 74% foreign exchange-neutral GMV growth in the fourth quarter. Demand is expanding across multiple markets, including Mexico, Chile, Colombia and Argentina, as MercadoLibre broadens its international product assortment. The company has also improved its global supply chain by increasing inventory in China and opening its first fulfillment center there.

MercadoLibre expects the China-Latin America corridor to become an important driver of growth as it scales its fulfilled-from-China model and continues investing in cross-border logistics and infrastructure. These initiatives are helping the company expand product variety for its more than 121 million active buyers, strengthening long-term revenue growth.

Growing AUM and Digital Banking Boost MELI Prospects

MercadoLibre’s expanding digital banking ecosystem, led by Mercado Pago, is becoming an increasingly important long-term growth driver for the company. A key indicator of this progress is the rapid growth in assets under management (AUM) within its fintech platform. Over the past three years, AUM has surged from roughly $2 billion to nearly $19 billion. This growth has been fueled by Mercado Pago’s strategy of offering attractive yields on funds held in the platform, which encourages users to deposit and retain money within the ecosystem rather than traditional banks.

The company’s fintech platform is also expanding its user base at a strong pace. Monthly active users of Mercado Pago have grown significantly, reaching about 78 million, more than doubling in recent years as consumers increasingly rely on the platform for payments, savings, investments and credit services. This expansion demonstrates MercadoLibre’s ability to deepen customer engagement. In the fourth quarter of 2025, the credit portfolio reached $12.5 billion, supported by almost 3 million new credit cards issued during the quarter.

Conclusion: Hold MELI for Now

MercadoLibre faces near-term headwinds from aggressive investments, margin pressure and macroeconomic uncertainty across Latin America. However, strong momentum in cross-border trade and the rapid expansion of its fintech ecosystem support long-term growth potential. Investors may consider holding MELI for now, given its strong long-term growth prospects despite near-term pressures.

MELI currently carries a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Scotiabank Lifts Verizon (VZ) to Outperform, Calls Shares "Cheap" at Current Levels

These Dividend Stocks Pay More Than 10-Year Treasury Bonds

Baird Upgrades Union Pacific (UNP) and Raises Target, Sees Upside from Potential Rail Deal

American Electric Power (AEP) Gets Price Target Hikes from Evercore ISI and Argus