Is Now the Moment to Consider Selling Blackstone Shares as Private Credit Concerns Grow?

Blackstone Faces Headwinds Amid Private Credit Market Turbulence

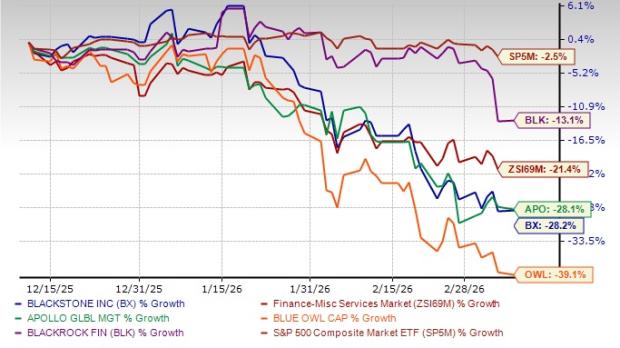

Alternative asset managers, including Blackstone Inc. (BX), have come under pressure in recent months due to growing worries about the private credit sector, capital outflows, and broader economic challenges. Over the past quarter, Blackstone's stock has dropped 28.2%, outpacing the 21.4% decline seen across its industry peers.

Market confidence was shaken when Blackstone’s flagship $82 billion private credit fund (BCRED) experienced a surge in redemption requests, with withdrawals surpassing normal quarterly limits. This raised alarms about the fund’s liquidity and the overall stability of private credit vehicles. In response, Blackstone increased its redemption cap from 5% to 7% earlier this month.

The spike in withdrawals was largely attributed to recent high-profile bankruptcies and credit issues in sectors like auto suppliers and subprime lenders, fueling fears of rising loan defaults within private credit portfolios. Additionally, investors have grown cautious about exposure to software and technology companies, which are facing uncertainty from AI-driven disruption and slower growth rates.

Rising bond yields and fluctuating interest rates have also made leveraged buyouts and real estate investments—key areas for Blackstone—less appealing, contributing to the company’s stock decline.

These challenges are not unique to Blackstone. Other major alternative asset managers, such as BlackRock (BLK), Apollo Global (APO), and Blue Owl Capital Inc. (OWL), have also seen their shares fall, with losses of 13.1%, 28.1%, and 39.1% respectively over the past three months.

3-Month Stock Performance

Source: Zacks Investment Research

Industry Responses and Investor Considerations

Recently, Blue Owl Capital limited withdrawals from one of its retail-focused funds, while Apollo Global’s CEO, Marc Rowan, cautioned that the private credit industry may face a shakeout due to increasing defaults among software borrowers. BlackRock also imposed restrictions on redemptions from its HPS Corporate Lending Fund after a spike in withdrawal requests.

Given the challenging environment for alternative asset managers, investors must weigh whether to retain or exit their positions. Before making any decisions, it’s crucial to evaluate Blackstone’s financial health and growth outlook to determine if the stock still presents attractive long-term potential.

Blackstone’s Core Strengths

Strong Asset Growth

Blackstone has maintained a robust asset base, with total assets under management (AUM) and fee-earning AUM growing at compound annual rates of 15.6% and 14.4%, respectively, over the past five years. By the end of 2025, the firm’s total AUM reached a record $1.27 trillion.

This growth has been fueled by steady capital inflows, strategic investments in high-growth sectors like infrastructure and technology, and successful fundraising efforts. Blackstone’s focus on areas such as digital infrastructure, AI, energy transition, and life sciences has provided significant momentum. Expanding into private wealth and insurance platforms has further diversified revenue streams, while innovative products like perpetual vehicles have broadened the investor base.

The company’s diverse product offerings and leading position in alternative investments are expected to continue supporting AUM expansion.

Effective Fundraising

Despite a tough fundraising climate, Blackstone has continued to attract capital. As of December 31, 2025, the firm had $198.3 billion in available capital (“dry powder”) for new investments. In 2024 and 2025, Blackstone deployed $133.9 billion and $138.2 billion, respectively, positioning itself to capitalize on market disruptions. The company also sees promising opportunities in markets like India and Japan.

In April 2025, Blackstone, alongside Wellington and Vanguard, formed a partnership to create simplified multi-asset solutions that combine public and private markets, aiming to enhance investor access to institutional-quality portfolios and address long-term diversification needs.

Valuation Overview

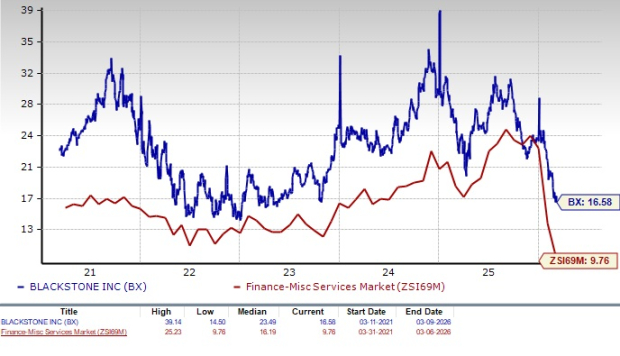

Currently, Blackstone’s shares trade at a premium compared to industry averages. The company’s forward 12-month price-to-earnings (P/E) ratio stands at 16.58, notably higher than the industry average of 9.76.

Forward P/E Ratio Comparison

Source: Zacks Investment Research

Should You Buy, Hold, or Sell Blackstone Now?

Blackstone’s elevated valuation relative to its peers raises caution about its near-term prospects. The company faces challenges from tighter credit conditions, higher interest rates, subdued deal activity in private equity and real estate, and concerns about exit opportunities—all of which may impact performance in the short run.

While immediate credit losses are not the primary concern, ongoing uncertainty in the private credit market may continue to affect Blackstone through investor sentiment, potential redemptions, and slower fundraising. Retail and wealth-channel investors remain cautious about semi-liquid credit vehicles, which could result in continued outflows or slower inflows, putting some pressure on AUM and fee-related earnings.

Recent analyst estimate revisions suggest a less optimistic outlook for Blackstone’s earnings growth. Although projections for 2026 and 2027 show year-over-year growth of 14% and 26.8%, respectively, both estimates have been revised downward in the past month.

Earnings Estimate Trends

Source: Zacks Investment Research

Long-Term Perspective

Despite current challenges, Blackstone’s diversified platform—spanning private equity, real estate, credit, infrastructure, and hedge fund solutions—enables the company to generate multiple revenue streams. As the largest alternative asset manager in the U.S., Blackstone’s strong brand and deep institutional relationships are likely to support ongoing growth in AUM and fee-related earnings over time.

Conservative investors may prefer to avoid Blackstone stock at present due to valuation concerns, but existing shareholders might consider holding their positions, as the company’s long-term prospects remain solid. Investors should monitor developments in the private credit market and Blackstone’s strategic responses before making new investment decisions.

Currently, Blackstone holds a Zacks Rank #3 (Hold).

Exploring Opportunities Beyond the Mainstream AI Stocks

The artificial intelligence boom has already created significant wealth, but the best returns may come from lesser-known companies addressing major global challenges. These emerging AI firms could offer substantial upside in the coming months and years.

Additional Resources

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Ethena: Is 4.47M ENA accumulation quietly sparking a recovery?

Advertising Software Companies Q4 Earnings: LiveRamp (NYSE:RAMP) Performance Comparison

Visa, Mastercard speed up the rollout of AI solutions for enterprises