Spotting Top Performers: Penske Automotive Group (NYSE:PAG) and Auto Retail Stocks in the Fourth Quarter

Q4 Earnings Review: Vehicle Retailers Face Mixed Results

Quarterly earnings reports often provide valuable insight into a company's future trajectory. Now that the fourth quarter has concluded, let's examine how Penske Automotive Group (NYSE:PAG) and its industry peers have performed.

Purchasing a car is a significant financial commitment for most individuals, often second only to buying a home. To attract buyers, auto retailers—whether selling new or pre-owned vehicles—focus on offering variety, convenience, and excellent customer service. Although online platforms play a growing role, especially for research, the car sales industry remains highly fragmented and largely local due to the complexity and cost of transporting vehicles over long distances. Ultimately, many people depend on cars for daily transportation, and dealerships are well aware of this essential demand.

Among the five vehicle retailers we monitor, the fourth quarter was generally sluggish. Collectively, their revenues matched analyst forecasts.

In light of these developments, share prices across the group have struggled, with an average decline of 11.8% since the most recent earnings announcements.

Penske Automotive Group (NYSE:PAG): Global Reach, Modest Growth

Penske Automotive Group operates an extensive international network, with dealerships in the United States, United Kingdom, Canada, Germany, Italy, Japan, and Australia. The company sells both new and used vehicles, and also provides services, parts, and financing solutions.

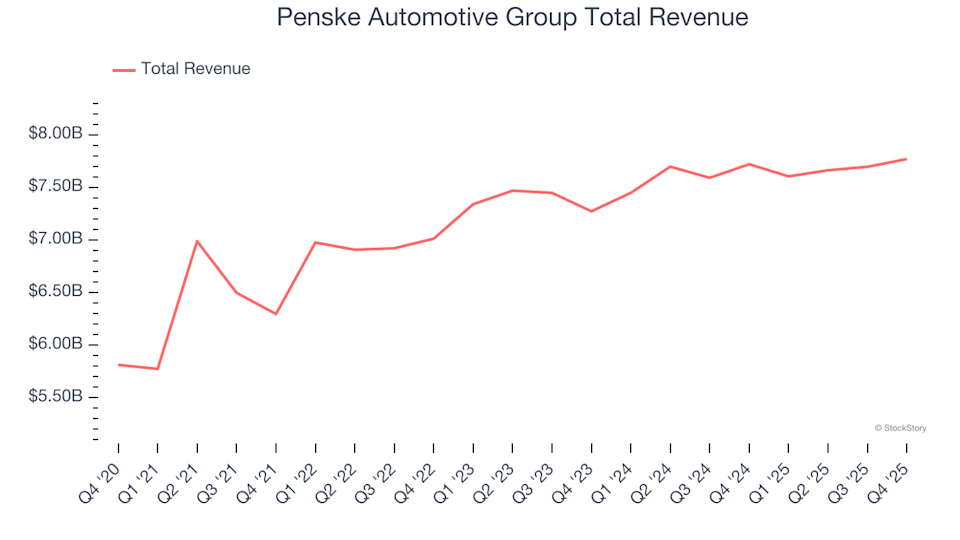

For the fourth quarter, Penske Automotive Group reported revenue of $7.77 billion, which was unchanged from the previous year and surpassed analyst expectations by 2.2%. Despite this revenue beat, the company fell short of analyst projections for both EBITDA and gross margin, making it a softer quarter overall.

While Penske posted the strongest revenue growth among its peers, investor sentiment remained cautious. The stock has declined 2.8% since the earnings release and is currently trading at $156.02.

CarMax (NYSE:KMX): Q4 Standout

CarMax, recognized for its transparent and customer-focused approach, is the largest automotive retailer in the U.S., offering a vast selection of vehicles.

In the fourth quarter, CarMax generated $5.79 billion in revenue—a 6.9% decrease year over year—but still exceeded analyst forecasts by 3.3%. The company delivered a strong performance, beating analyst estimates for both earnings per share and EBITDA.

CarMax outperformed its peers in surpassing analyst expectations. The market responded positively, with shares rising 2.8% since the earnings announcement. The stock is now priced at $42.21.

Is CarMax a buy right now?

Camping World (NYSE:CWH): Q4 Laggard

Established in 1966 as a single RV dealership, Camping World now offers recreational vehicles, boats, and a range of outdoor products.

Camping World reported fourth-quarter revenue of $1.17 billion, a 2.6% year-over-year decline, but still managed to beat analyst expectations by 1.2%. However, the company missed projections for both EBITDA and gross margin, resulting in a weaker quarter.

Reflecting these results, Camping World’s stock has dropped 31.3% since the report and is currently valued at $7.45.

AutoNation (NYSE:AN): Facing Headwinds

AutoNation operates one of the largest dealership networks in the U.S., with over 300 locations primarily in the Sunbelt region. The company sells new and used vehicles, as well as parts and services across multiple brands.

For the fourth quarter, AutoNation posted revenue of $6.93 billion, a 3.9% decrease from the previous year and 3.6% below analyst expectations. The company also missed forecasts for both EBITDA and revenue, marking a challenging quarter.

AutoNation had the weakest performance relative to analyst estimates among its peers. The stock has fallen 4.6% since the earnings release and is now trading at $194.68.

Lithia Motors (NYSE:LAD): Mixed Results

Lithia Motors, with a strong footprint in the Western United States, offers a broad selection of new and pre-owned vehicles, including luxury models from various manufacturers.

In the fourth quarter, Lithia reported revenue of $9.20 billion, unchanged from the prior year and 0.6% below analyst expectations. The company delivered a solid EBITDA beat but missed earnings per share estimates, resulting in a mixed performance.

Since the earnings announcement, Lithia’s stock has declined 20.5% and is currently priced at $259.50.

Looking for Strong Performers?

If you’re interested in companies with robust fundamentals and growth potential, explore our Strong Momentum Stocks list. These businesses are well-positioned to thrive regardless of broader economic or political shifts.

The StockStory analyst team, comprised of experienced investment professionals, leverages quantitative analysis and automation to deliver timely, high-quality market insights.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.