Can Wells Fargo Turn Regulatory Relief Into Sustainable Growth?

For years, Wells Fargo & Company WFC operated under a regulatory constraint, a $1.95-trillion asset cap imposed by the Federal Reserve in 2018 following its fake account scandal. The restriction limited the bank’s ability to expand its balance sheet, constraining loan growth, deposit accumulation and overall business expansion.

Over the years, Wells Fargo invested heavily in strengthening internal controls, enhancing board oversight and addressing compliance deficiencies across its operations. The bank gradually resolved multiple regulatory orders, demonstrating steady progress in governance and risk oversight.

In June 2025, the Fed lifted the asset cap after confirming that Wells Fargo had met the conditions required under the 2018 enforcement action. The termination of the 2018 order last week marks the closure of the final remaining consent order linked to the fake-account scandal, ending nearly a decade of regulatory oversight.

The key question now is whether this regulatory relief can translate into sustainable long-term growth.

WFC: A Strategic Reset Post Regulatory Relief

The removal of the asset cap significantly expands Wells Fargo’s strategic flexibility. The bank can now grow its loan book, deposits and securities portfolio without regulatory constraints. This will lead to an increase in NII. By 2025-end, WFC’s loans increased nearly 7%, while deposits rose 6.4% since June 2025.

Equally important, Wells Fargo can now accelerate expansion in fee-generating businesses, including payment services, asset management and mortgage origination. WFC increased trading-related assets by 50% in 2025 as it is able to now utilize its balance sheet to accelerate growth in trading businesses. Additionally, the bank is strengthening its credit card portfolio, reflecting improved customer penetration and diversified fee income streams. These efforts will enhance the company’s profitability.

Operational efficiency initiatives also reinforce its growth prospects. Since 2020, Wells Fargo has streamlined its organizational structure, reduced headcount and optimized its branch network. Non-interest expenses have declined slightly over the past five years, reflecting disciplined cost management.

Reflecting this renewed flexibility and operational efficiency, management expects to achieve the medium-term return on tangible common equity (ROTCE) target of 17-18%. Achieving this level would signal stronger capital efficiency and improved profitability, suggesting that the bank’s restructuring efforts are beginning to unlock operational potential.

Other Banks’ Progress to Fix Regulatory Issues

In December 2025, Citigroup, Inc. C received notable regulatory relief after the Office of the Comptroller of the Currency removed the July 2024 amendment to the bank’s 2020 consent order. This original consent order was focused on longstanding deficiencies in risk management, data governance, internal controls and compliance. With regulatory easing, Citigroup is better-positioned to accelerate its growth and efficiency initiatives.

In September 2025, UBS Group AG UBS agreed to settle a long-running French tax case concerning its cross-border business activities between 2004 and 2012. The settlement follows years of appeals after a 2019 trial court found UBS guilty of illicit client solicitation and laundering the proceeds of tax fraud. The resolution reflects UBS Group AG’s strategy to address legacy matters while minimizing ongoing operational and financial risks.

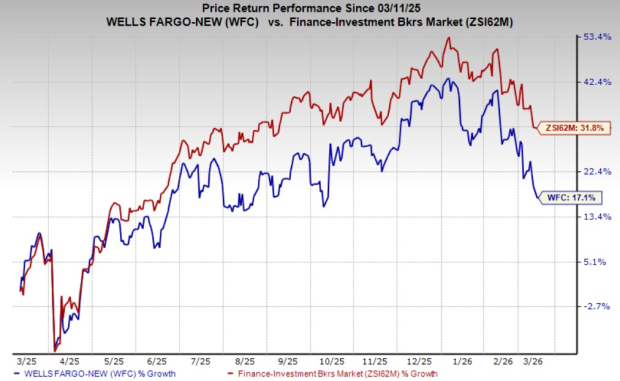

WFC’s Price Performance & Zacks Rank

Wells Fargo’s shares have gained 17.1% over the past year compared with the industry’s growth of 31.8%.

Image Source: Zacks Investment Research

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.