3 Key Reasons to Offload CSCO and One Alternative Stock Worth Buying

Cisco’s Recent Performance: Outpacing the Market

Over the past six months, Cisco has delivered an impressive 11.6% return, surpassing the S&P 500 by 8.5%. Its stock price has reached $76.02 per share, driven in part by strong quarterly earnings. This notable performance may leave investors considering their next move.

Is this a good opportunity to invest in Cisco, or should you exercise caution before adding it to your portfolio?

Why We’re Not Enthusiastic About Cisco

Despite recent gains, we remain hesitant about Cisco’s prospects. Below are three key reasons we’re steering clear of CSCO, along with a stock we prefer instead.

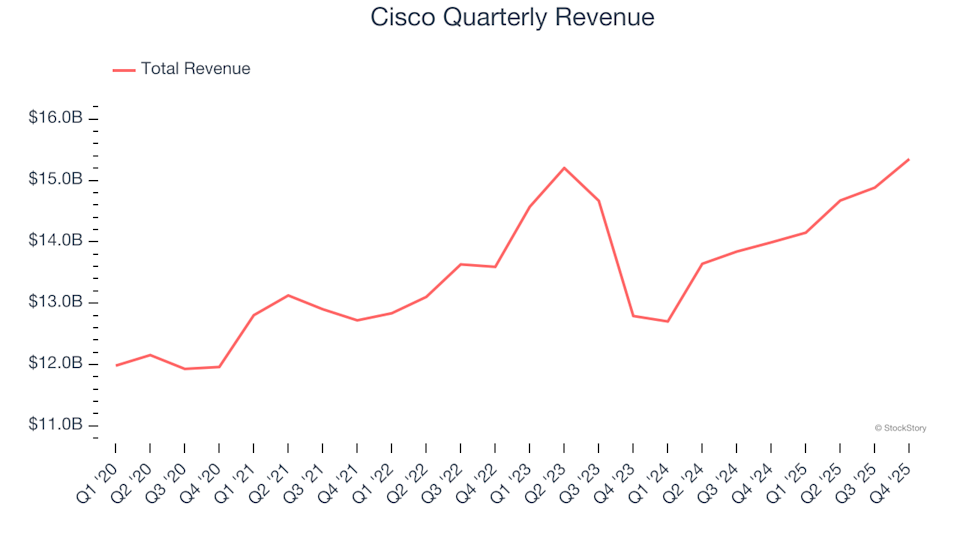

1. Underwhelming Long-Term Revenue Growth

Evaluating a company’s sales trajectory over several years offers valuable insight into its underlying strength. While any business can post strong results in the short term, sustained growth is what sets the best apart. Cisco’s revenue has increased at a modest 4.2% compound annual growth rate over the past five years—falling short of our expectations for the business services sector.

Cisco Quarterly Revenue

2. Declining Free Cash Flow Margins

At StockStory, we place significant emphasis on free cash flow, as it ultimately determines a company’s ability to cover expenses and invest in growth. Over the last five years, Cisco’s free cash flow margin has dropped by 5.9 percentage points. If this downward trend persists, it could indicate rising capital requirements and greater investment needs. For the trailing twelve months, Cisco’s free cash flow margin stood at 20.7%.

Cisco Trailing 12-Month Free Cash Flow Margin

3. Diminishing Returns on New Investments

Return on invested capital (ROIC) measures how efficiently a company generates operating profit from its total capital base. While we favor businesses with robust returns, the direction of ROIC is often what surprises investors and influences share prices. Unfortunately, Cisco’s ROIC has seen a notable decline in recent years. Although management has made sound decisions in the past, this downward trend may reflect a shortage of lucrative growth opportunities.

Cisco Trailing 12-Month Return On Invested Capital

Our Verdict

While Cisco remains a solid company, it doesn’t meet our investment criteria. The stock, currently trading at 18.3 times forward earnings (or $76.02 per share), has outperformed the market lately. However, our analysis suggests the potential rewards do not outweigh the risks. We believe there are more attractive opportunities available. For example, take a look at our top pick in the semiconductor sector.

Stocks We Prefer Over Cisco

ALSO RECOMMENDED: Top 5 Momentum Stocks. The ideal moment to invest in a standout stock is when the market begins to recognize its potential. These companies not only boast strong fundamentals but are also experiencing significant momentum right now—offering a compelling combination for investors.

Discover which stocks our AI-driven platform is highlighting this week. Explore the latest Strong Momentum stocks—completely free.

Our list features well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Exlservice, which delivered a 354% return over five years. Start your search for the next breakout stock with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Echostar Drops 1.29% as Industry Uncertainty Grows; $660M Trading Volume Places at 182nd

Altseason 3.0 Setup? OTHERS/BTC Retests Historic Launchpad as 4 Altcoins Prepare for Potential 5× Expansion

Intuitive Surgical Shares Drop 1.56% as $750M Trading Volume Ranks 157th Post-European Expansion

Workday Stock Drops 3.81% Even After Posting Record Profits and Achieving $740M in Trading Volume, Ranking 160th