Oracle's $7.53 Billion Trading Volume Ranks 9th as Cloud Growth Struggles with Debt and Market Volatility

Market Snapshot

Oracle (ORCL) experienced a surge in trading volume on March 10, 2026, with $7.53 billion in shares traded—a 61.74% increase from the prior day—ranking ninth in market activity. Despite this, the stock fell 1.43% to $152.96, reflecting ongoing investor caution. The decline came amid a broader context of a 22% year-to-date drop and a 56% fall from its September 2025 peak. The stock’s performance highlights a tug-of-war between strong cloud revenue growth and concerns over debt accumulation and macroeconomic risks.

Key Drivers

Oracle’s Q3 fiscal 2026 results are expected to show robust cloud growth, with OracleORCL-1.43% Cloud Infrastructure (OCI) expanding 68% year-over-year, driven by a $300 billion partnership with OpenAI. This collaboration, one of Oracle’s largest commercial agreements, underscores its strategic pivot to AI infrastructure. Cloud applications, including SaaS offerings, grew 11%, contributing to cloud revenue accounting for nearly half of total sales. However, this growth contrasts with forecasted declines in IaaS/PaaS segments (21.8% and 16.7%, respectively), creating a valuation gap between Oracle’s premium P/E ratio (27.96) and its ability to sustain cloud momentum amid macroeconomic headwinds like inflation and labor volatility.

The company’s aggressive capital expenditures have raised red flags. Debt and lease obligations surged $23 billion in the first half of 2026, with free cash flow turning negative at -$10 billion. Oracle announced plans to raise $45–$50 billion via equity and debt offerings to fund its cloud expansion, including the $500 billion Stargate project. While remaining performance obligations (RPO) skyrocketed 438% to $523 billion in Q2—a forward-looking indicator of future revenue—investors remain wary of Oracle’s ability to service its debt load. The stock’s negative free cash flow and halted buybacks further amplify concerns about financial sustainability.

Analyst sentiment is mixed. RBC Capital analyst Rishi Jaluria downgraded his price target to $160 from $195, citing overreliance on OpenAI and financing risks, while Piper Sandler’s Billy Fitzsimmons maintained a Buy rating with a $240 target, emphasizing untapped AI revenue potential. The Street consensus of 25 Buys and 6 Holds reflects optimism about Oracle’s cloud growth, but RBC and others highlight execution risks, including shelved OpenAI expansion plans and recent layoffs. Oracle’s management also redirected capital to existing AI infrastructure, signaling a shift in priorities as it navigates project delays and compute requirement disputes.

Oracle’s valuation hinges on its ability to outperform in AI-driven hardware demand and stabilize cloud margins. A “beat and raise” on Q3 earnings and cloud guidance could narrow the valuation gap, but weak IaaS/PaaS performance or macro-driven demand compression would likely trigger a sell-off. The stock’s premium P/E and debt load (including operating leases) amplify downside risks, particularly if cloud growth slows or macroeconomic pressures intensify. Investors are closely watching Oracle’s progress in AI partnerships, such as OpenAI updates, and its capacity to balance capital-intensive investments with profitability.

Outlook and Strategic Challenges

Oracle’s $523 billion RPO and $500 billion backlog highlight its long-term revenue potential, but short-term headwinds persist. The Stargate project, a critical component of Oracle’s AI infrastructure strategy, faces execution risks after disputes over financing and compute requirements led to OpenAI expansion delays. Meanwhile, competition from rivals like Anthropic and Amazon Web Services (AWS) intensifies, with RBC noting Anthropic’s growing enterprise market share. Oracle’s recent workforce reductions and capital reallocation underscore the urgency of cost management amid rising debt.

In the near term, Oracle’s stock is likely to remain volatile as investors weigh its aggressive AI investments against profitability timelines. The company’s ability to secure funding for its Stargate project and demonstrate cloud margin resilience will be pivotal. If Oracle can stabilize its debt trajectory and deliver consistent cloud growth, its premium valuation may be justified. However, any missteps in execution or macroeconomic deterioration could widen the valuation gap, prompting further sell-offs. The market’s reaction to Q3 earnings and subsequent guidance will be a key inflection point, with a 74% potential upside to $263.86 versus current levels, but downside risks remain significant.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

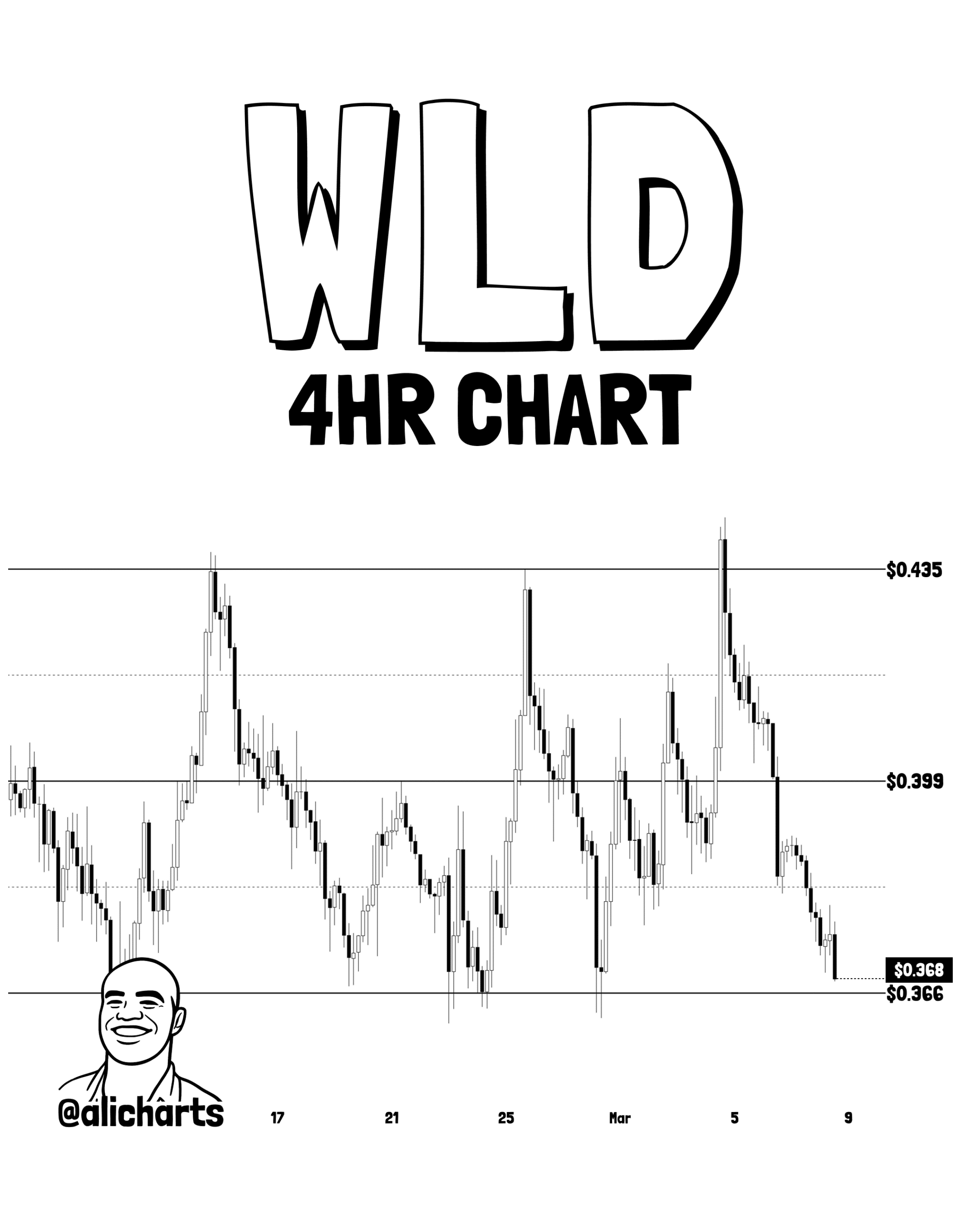

Worldcoin: Analyst spots KEY range level – WLD’s move to $0.435 possible IF…

Trending news

MoreITT's shares climb 1.95% following $1.14 billion fundraising, boosting optimism for SPX FLOW takeover; trading activity rises 86%, placing it at 444th in volume rankings

ITT shares climb 1.95% amid $1.14 billion issuance, boosting optimism for SPX FLOW takeover; trading volume soars 86%, reaching 444th place