Williams Companies Climbs 0.90% Even as Trading Volume Falls 25.96% Places 244th in Today's Trading Volume

Overview of Williams Companies Stock Performance

On March 10, 2026, Williams Companies (WMB) ended the trading session up 0.90%, closing at $73.84 per share. The day saw 6.86 million shares exchanged, marking a 25.96% decrease in volume compared to the previous session’s 8.90 million shares. Despite lighter trading, WMB ranked 244th in daily trading activity. The company’s market value reached $90.2 billion, with a price-to-earnings ratio of 34.50 and a 52-week price range between $51.58 and $76.87. Analysts have set an average target price of $77.41, reflecting a positive outlook, while the stock’s beta of 0.65 points to lower volatility relative to the overall market.

Main Influences on Stock Movement

Institutional Holdings and Analyst Revisions

During the third quarter of 2026, institutional investors made notable changes to their WMB positions. Russell Investments Group Ltd. expanded its holdings by 14.2%, acquiring an additional 166,782 shares. In contrast, Swiss National Bank trimmed its stake by 4.7%, selling 175,500 shares. These contrasting moves highlight differing short-term perspectives among major investors. Overall, institutional investors and hedge funds continue to hold a significant 86.44% of WMB shares, underscoring the stock’s appeal to large-scale investors.

Analyst sentiment has also shifted, with several firms revising their ratings and price targets. Scotiabank upgraded WMB to “sector outperform” and raised its price target to $84.00. UBS Group and Morgan Stanley followed suit, increasing their targets to $89.00 and $90.00, respectively, and assigning “buy” or “overweight” ratings. The consensus among analysts now stands at a “Moderate Buy” with an average target price of $75.86. These upgrades reflect growing confidence in Williams Companies’ long-term prospects, particularly as demand for natural gas and infrastructure rises.

Financial Results and Dividend Policy

In the first quarter of 2026, Williams Companies reported earnings of $0.55 per share, slightly below the consensus estimate of $0.57. However, the company surpassed revenue expectations, posting $3.2 billion—an increase of 3.2% over the projected $3.1 billion. Despite the minor earnings shortfall, Williams demonstrated strong operational performance with a return on equity of 17.32% and a net margin of 21.90%. The company also announced a 5% increase in its quarterly dividend, raising it to $0.525 per share and offering a 2.9% yield. This dividend boost, along with a forward payout ratio of 93.46%, signals management’s confidence in sustaining payouts even amid modest earnings growth.

Insider Trading and Market Perception

Recent insider transactions have sent mixed messages to the market. Senior executives such as SVP Terrance Lane Wilson and CAO Mary A. Hausman sold significant portions of their shares—Wilson reduced his holdings by 8.43%, while Hausman’s stake fell by 36.97%. Over the past 90 days, insiders sold a total of 41,107 shares valued at $3.01 million, representing a small fraction of the company’s outstanding shares. While these sales could indicate short-term liquidity needs or caution regarding near-term performance, their overall impact is limited, as insiders collectively own just 0.44% of the company.

Industry Landscape and Strategic Advantages

Williams Companies’ results are closely linked to broader trends in the energy sector for 2026. As a midstream company specializing in natural gas transportation and storage, Williams benefits from increased infrastructure demand and evolving energy policies. Analysts point to rising natural gas consumption, driven by industrial use and exports, as a key factor supporting the company’s fundamentals. With a debt-to-equity ratio of 1.83 and a beta of 0.63, Williams maintains a balanced risk profile, managing leverage in line with industry norms. While major oil producers face scrutiny over profitability, Williams’ focus on midstream logistics positions it to generate steady cash flows and secure long-term contracts.

Future Prospects and Valuation

Looking forward, Williams Companies projects full-year 2026 earnings between $2.20 and $2.38 per share, in line with analysts’ estimates of $2.08. The stock’s price-to-earnings growth ratio of 1.27 and 2.9% dividend yield make it appealing to income-oriented investors, though its elevated P/E ratio of 34.17 suggests that continued earnings growth will be necessary to support current valuations. With analysts highlighting Williams’ strategic role in the energy supply chain and institutional investors adjusting their positions, the company’s future performance will depend on its ability to meet guidance and execute expansion plans.

This analysis brings together insights from institutional activity, analyst opinions, and company developments to offer a thorough review of Williams Companies’ recent stock trends.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

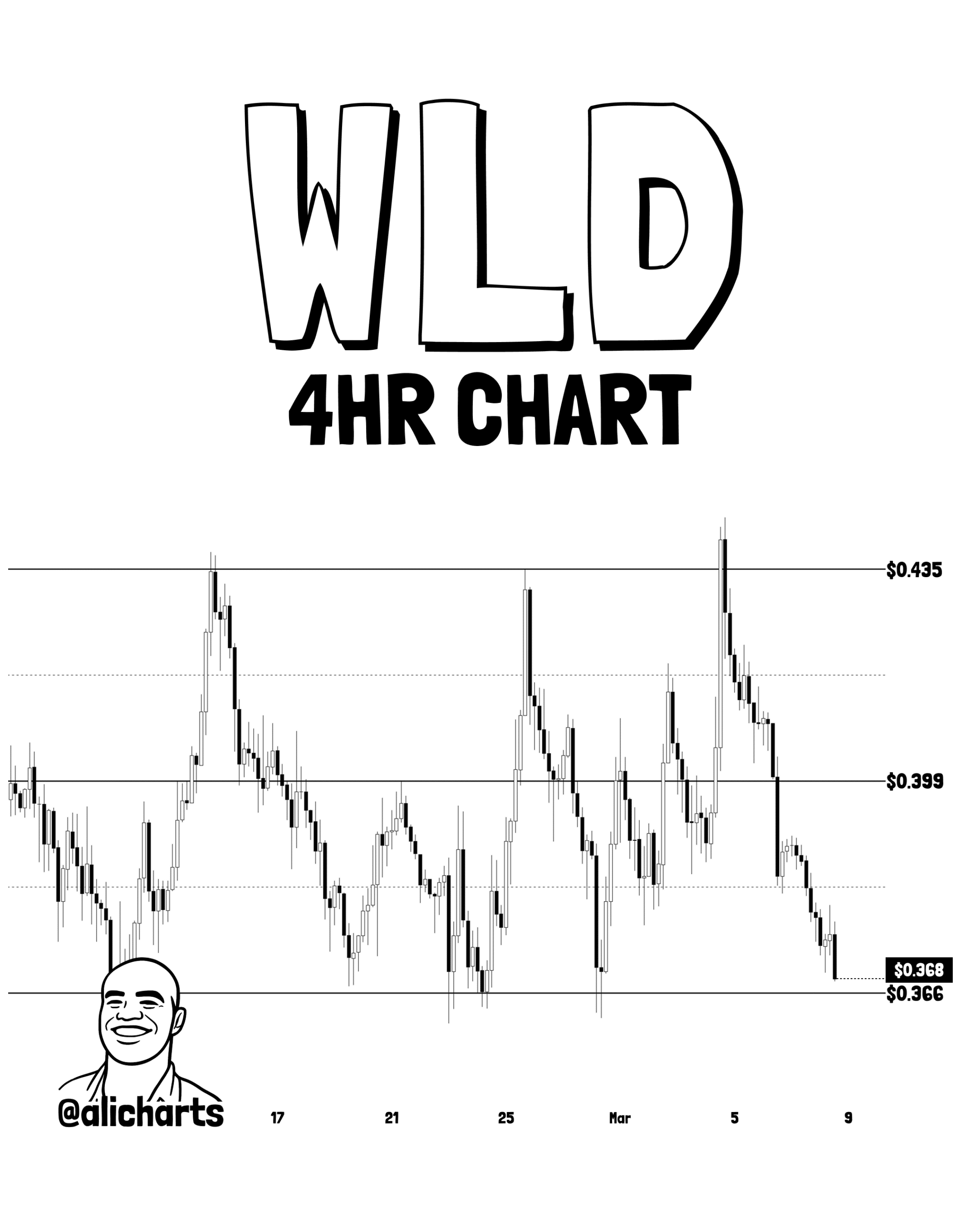

Worldcoin: Analyst spots KEY range level – WLD’s move to $0.435 possible IF…

Trending news

MoreITT's shares climb 1.95% following $1.14 billion fundraising, boosting optimism for SPX FLOW takeover; trading activity rises 86%, placing it at 444th in volume rankings

ITT shares climb 1.95% amid $1.14 billion issuance, boosting optimism for SPX FLOW takeover; trading volume soars 86%, reaching 444th place