Howmet Aerospace Slides to 248th in Trading Activity as Earnings Beat Clashes with Insider Sales and Institutional Skepticism

Market Snapshot

Howmet Aerospace (HWM) closed on March 10, 2026, with a 0.09% decline in its stock price, reflecting modest downward pressure amid mixed investor sentiment. Trading volume fell sharply to $0.50 billion, a 24.34% drop from the prior day, ranking the stock 248th in market activity. Despite the earnings beat in February—reporting $1.05 per share (EPS) against a $0.97 consensus and $2.17 billion in revenue—the stock struggled to maintain momentum. Institutional ownership dynamics added complexity, with LGT Group Foundation boosting its stake by 58.3% in Q3 to $3.96 million, while Capital International Sarl and Korea Investment CORP reduced holdings by 11.8% and 48.2%, respectively. Analysts remain cautiously optimistic, with a "Moderate Buy" consensus and a $252.95 average price target, though insider sales by executives like VP Barbara Shultz and EVP Neil Marchuk hinted at internal caution.

Key Drivers of Stock Movement

Institutional Investor Activity and Mixed Ownership Trends

Institutional investor behavior highlighted divergent views on HWM’s outlook. LGT Group Foundation’s 58.3% stake increase in Q3 signaled confidence in the aerospace sector’s long-term potential, while Traub Capital and Winnow Wealth entered new positions in Q2 with $25,000 investments each. Conversely, Korea Investment CORP’s 48.2% reduction and Richard Bernstein Advisors’ 46.1% sell-off underscored skepticism about short-term valuation. These contrasting actions reflect broader debates about Howmet’s exposure to cyclical aerospace demand versus its robust earnings performance. With 90.46% of shares held by institutions, such movements can amplify market volatility.

Analyst Optimism and Elevated Price Targets

Analysts largely reinforced a bullish narrative, with six major firms raising price targets in late January–February 2026. Bank of America, JPMorgan, and Deutsche Bank increased targets by 16–20% to $300–$278, citing Howmet’s 14.6% revenue growth, 30.41% return on equity, and FY 2026 guidance of $4.35–$4.55 EPS. Citigroup and Truist also upgraded to "Buy," aligning with a "Moderate Buy" consensus. However, the absence of HWMHWM-0.09% in top analysts’ "must-buy" lists (as noted by MarketBeat) suggested lingering caution about valuation multiples, given the stock’s 68.48 P/E ratio and 2.32 P/E/G ratio. This optimism contrasted with the 29.67% insider sell-off by EVP Marchuk, which may have introduced short-term uncertainty.

Earnings Strength and Strategic Guidance

Howmet’s Q4 2025 results provided a strong foundation for its 2026 outlook. The company exceeded expectations with $1.05 EPS (up from $0.77 in the prior year) and $2.17 billion in revenue, driven by 14.6% year-over-year growth. Management reiterated ~10% revenue growth to $9.1 billion and a 30.3% adjusted EBITDA margin for 2026, emphasizing investments in Engine Products, Fastening Systems, and Forged Wheels. These strategic moves align with market drivers like commercial aviation recovery and gas turbine demand, reinforcing confidence in its ability to outperform industry peers. However, the stock’s muted response to these updates—despite a $0.12 quarterly dividend (0.2% yield)—suggested that investors were pricing in these factors ahead of the February 12 earnings release.

Insider Sales and Market Sentiment

Insider transactions added nuance to the stock’s narrative. VP Barbara Shultz sold 1,000 shares at $260 each, reducing her stake by 4.02%, while EVP Marchuk’s 29.67% sell-off of 45,150 shares at $251.70 raised questions about executive confidence. Though insider ownership remains at 1.12%, these sales could signal tactical portfolio adjustments rather than fundamental concerns. Meanwhile, the broader market context—Howmet’s 1.20 beta and 1.21 volatility—suggested it mirrored aerospace sector trends, which were themselves influenced by defense spending and global supply chain dynamics.

Dividend and Capital Allocation Strategy

Howmet’s $0.12 quarterly dividend (12.94% payout ratio) offered a modest yield but aligned with its capital allocation strategy. The $0.48 annualized dividend, coupled with $1.6 billion in projected free cash flow for 2026, demonstrated management’s focus on balancing shareholder returns with reinvestment in high-growth segments. This approach resonated with analysts, who highlighted the company’s 18.27% net margin and 0.53 debt-to-equity ratio as indicators of financial resilience. However, the dividend’s relatively low yield (0.2%) may have limited its appeal to income-focused investors compared to peers in the aerospace sector.

Conclusion: Balancing Optimism and Caution

Howmet Aerospace’s stock movement on March 10 reflected a tug-of-war between institutional optimism, analyst upgrades, and insider caution. While strong earnings, strategic guidance, and elevated price targets provided a solid foundation, divergent institutional flows and executive sales introduced short-term uncertainty. The stock’s performance will likely hinge on its ability to execute on capacity expansions in high-margin segments and navigate macroeconomic risks, including interest rate volatility and global aerospace demand cycles. For now, the "Moderate Buy" consensus captures this duality, positioning HWM as a candidate for long-term growth but with near-term execution risks.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

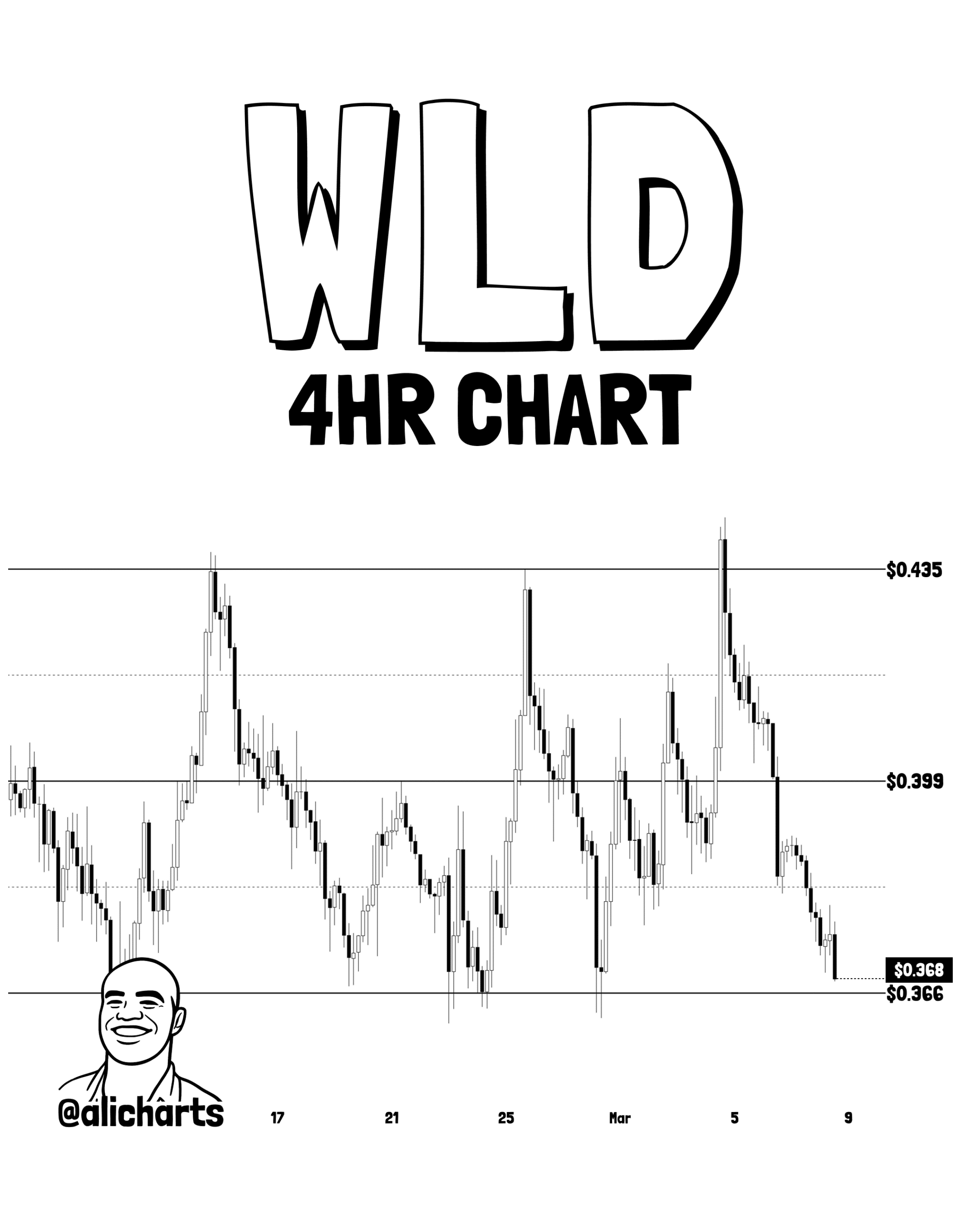

Worldcoin: Analyst spots KEY range level – WLD’s move to $0.435 possible IF…

Trending news

MoreITT's shares climb 1.95% following $1.14 billion fundraising, boosting optimism for SPX FLOW takeover; trading activity rises 86%, placing it at 444th in volume rankings

ITT shares climb 1.95% amid $1.14 billion issuance, boosting optimism for SPX FLOW takeover; trading volume soars 86%, reaching 444th place