Insurers Pull Back from Covering Iran Strait, Hinting at $100 Oil Expectations

Global Markets Brace for Economic Turbulence Amid Middle East Tensions

While headlines focused on the threat of a regional conflict, financial insiders were already anticipating a worldwide economic jolt. The first decisive actions came not from governments, but from the leadership of major oil corporations and international insurance firms. On March 2, mere hours after Iran announced the closure, several leading oil companies and trading firms halted shipments through the Strait of Hormuz. This was not a media event, but a strategic move to safeguard assets, effectively shutting down a vital channel for global commerce.

However, the most telling development emerged from the insurance sector. The real mechanism behind the shutdown was financial rather than military. On March 5, marine insurers Gard, Skuld, and NorthStandard publicly declared they would withdraw war-risk coverage, prompting four additional major insurers to follow suit. Without insurance, shipping through the Strait became untenable—risks were simply too high and losses uninsurable. When the insurance industry pulls back, the rest of the market quickly follows suit.

The magnitude of this disruption underscores the pessimistic outlook among market professionals. The closure has stalled nearly 20% of the world’s petroleum shipments. The crisis escalated further as Houthi forces renewed attacks on the Suez/Bab el-Mandeb corridor, resulting in about one-third of global seaborne crude being jeopardized at once. This is not a minor supply issue but a profound shock to the global energy system. Investors are not expecting a swift resolution; instead, they are preparing for a drawn-out crisis that could push oil prices above $100 per barrel and heighten recession risks for major economies. The swift reactions in oil and insurance markets are clear evidence of these expectations.

How Corporate Leaders Are Responding to the Crisis

Market signals are mixed. The FTSE 100 posted modest gains, but Asian markets such as South Korea and Thailand experienced sharp declines, triggering trading halts after drops exceeding 8%. This divergence is an early warning sign.

ATR Volatility Breakout (Long-only) Strategy Overview

- Entry: Initiate a long position when the 14-day ATR exceeds its 60-day average and the price closes above the 20-day high.

- Exit: Close the position if the price falls below the 20-day low, after 20 trading days, or if a 10% profit or 5% loss threshold is reached.

- Instrument: CL=F (Crude Oil Futures)

- Risk Controls: Take-profit at 10%, stop-loss at 5%, maximum holding period of 20 days.

Backtest Performance

- Total Return: 13.41%

- Annualized Return: 4.32%

- Maximum Drawdown: 2.77%

- Profit-Loss Ratio: 3.09

- Total Trades: 9

- Winning Trades: 6

- Losing Trades: 3

- Win Rate: 66.67%

- Average Hold Days: 17.89

- Max Consecutive Losses: 1

- Average Win Return: 2.53%

- Average Loss Return: 0.78%

- Largest Single Gain: 4.33%

- Largest Single Loss: 1.19%

Investors are not convinced by claims of market resilience; instead, they are preparing for a sustained period of instability. The UK’s slight market uptick is largely due to its domestic energy resources, while the turmoil in Asian markets highlights the vulnerability of export-driven economies that depend heavily on Middle Eastern oil passing through the Strait of Hormuz.

The United States enjoys some protection thanks to its own oil and gas production, a buffer not available to many of its allies. Nevertheless, the U.S. is not immune—global disruptions in trade, pricing, and investment could still negatively impact American growth. The real challenge for U.S. corporate leaders is whether their optimism can withstand these external shocks. Recent surveys indicate that while CEO confidence has risen, nearly 60% now view geopolitical instability as a significant threat—a clear warning from those most familiar with their supply chains.

All eyes are on the Bank of England’s upcoming interest rate decision on March 19. The ongoing conflict injects considerable uncertainty into projections for inflation and economic growth. The central bank must balance surging energy costs against the risk of a global slowdown. This unpredictable environment could force a shift in monetary policy. While markets expect the U.S. Federal Reserve to maintain its current stance, the Bank of England faces a more difficult decision. Prolonged conflict may require either a more accommodative approach to support growth or tighter policy to combat imported inflation. Investors are closely monitoring the Bank of England as a bellwether for the depth of global economic fractures.

Key Triggers and What Investors Are Watching

Market participants are not simply betting on turmoil—they are waiting for specific developments that will either confirm their concerns or prompt a reversal. The scenario is clear: a sustained dual chokepoint crisis. The first major milestone is a hard deadline; economic models suggest that if the Strait of Hormuz remains closed for more than 30 days, the likelihood of a global recession among major importers becomes extremely high. Oil prices could surge to between $100 and $200 per barrel, depending on the situation’s severity. Any indication that the closure will be prolonged is likely to spark a dramatic repricing in oil markets, confirming the initial moves by insurers and shippers.

The most immediate risk is the absence of diplomatic progress. The initial military strikes and leadership losses were shocking, but the conflict’s direction depends on whether negotiations can resume. Investors are watching closely for any credible signs of de-escalation. If such signals are missing and hostilities continue, the worst-case scenario of a protracted war becomes more likely, potentially pushing oil prices from a manageable spike into territory that could trigger a global recession. Current market volatility reflects this uncertainty.

Looking further ahead, the long-term question is whether this crisis will permanently alter global trade routes. Initiatives like the India-Middle East-Europe Economic Corridor (IMEC) are being put to the test. These projects were designed to withstand shocks, not indefinite blockades. Investors will be watching to see if this event accelerates the adoption of alternative routes or exposes their shortcomings. A permanent shift in shipping patterns would signal a major transformation in global logistics, while underutilization would suggest greater resilience in existing networks. Either outcome will have significant implications for those invested in shipping, logistics, and energy infrastructure.

In summary, the market’s current positioning is both time-sensitive and conditional. Investors are bracing for the possibility that a temporary 30-day disruption could become a lasting reality. The critical factors to watch are the duration of the Strait’s closure, the reaction of oil prices, and whether global trade routes are permanently altered. These events will determine whether the pessimistic outlook is justified or if the world’s supply chains prove more robust than expected. For now, both regulatory filings and market behavior suggest a wait-and-see approach until the next major catalyst emerges.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

IonQ: £1.675M Donation, 2.56M Shares Issued, $12.8B Valuation

Insider Sales at Oil-Dri Indicate Savvy Investors Exit While Institutions Increase Their Holdings

Why Expand Energy (EXE) Stands Out as a Leading Long-Term Growth Stock

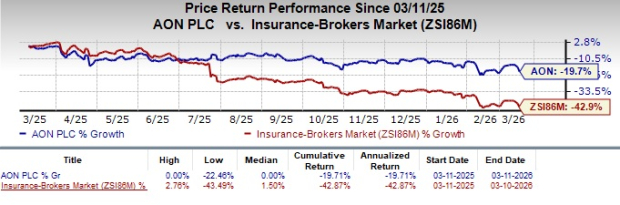

Aon Increases Technology Commitments Through VIPR Collaboration in Reinsurance