Dave’s Trading Price Is Lower Than Industry Peers: Bargain Opportunity or Hidden Risk?

Dave Inc.: A Standout Value Opportunity

Dave Inc. (DAVE) is currently positioned as a compelling value stock. Its forward 12-month price-to-earnings ratio sits at 14.95, which is notably lower than the industry average of 23.57 and well beneath its own 12-month median of 24.49. The company’s trailing 12-month EV/EBITDA is 17.06, just above the industry’s 17.09, but still under its median of 20.46.

Competitive Pricing and Financial Strength

Compared to rivals like Affirm (AFRM) and SoFi Technologies (SOFI), Dave’s shares are trading at a discount. Affirm’s forward P/E is 31.83, while SoFi’s is 28.48. For trailing 12-month EV/EBITDA, Affirm stands at 84.94 and SoFi at 21.91, both higher than Dave’s figures.

Despite its undervalued status, some investors may wonder if Dave is a value trap. However, the company’s robust margins dispel this concern. In the fourth quarter of 2025, Dave reported an adjusted gross profit margin of 74%, with a four-quarter average of 72.5%.

Impressive Growth Metrics

Dave’s adjusted EBITDA and adjusted net income surged by 118% and 92% year-over-year in Q4 2025, highlighting the company’s operational strength and supporting the case against it being a value trap. Analyst sentiment remains positive for the stock.

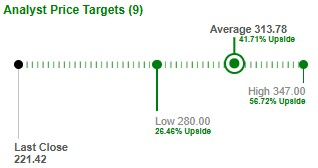

According to nine analysts, the average short-term price target for Dave is $313.8, representing a 41.7% increase from the previous closing price of $221.4. This outlook suggests that Dave is seen as both an innovative digital bank and an undervalued technology company, with significant growth potential as new products are launched.

Stock Performance and Valuation Gap

Over the past year, Dave’s stock has soared by 175.4%. Despite this substantial rise, the shares remain undervalued compared to industry peers. This discrepancy, combined with strong financials and a promising price target, points to continued upward momentum for Dave in the future.

Dave’s Forecasts and Value Rating

- Projected 2026 revenue: $694.9 million, a 25.4% increase from the prior year.

- Expected 2027 revenue growth: 20%.

- 2026 EPS estimate: $14.49, up 9.9% year-over-year.

- 2027 EPS forecast: 20.8% increase.

The consensus estimate for Dave’s 2026 earnings has risen by 3.5% in the past 60 days, while the 2027 estimate has decreased by 6% over the same period.

Dave holds a Value Score of C and is currently rated Zacks Rank #2 (Buy). For a full list of Zacks #1 Rank (Strong Buy) stocks, click here.

Quantum Computing: The Next Investment Frontier

Quantum computing is rapidly emerging as a transformative technology, potentially outpacing even artificial intelligence in its impact. Major tech companies—including Microsoft, Google, Amazon, Oracle, Meta, and Tesla—are racing to integrate quantum computing into their operations.

Kevin Cook, Senior Stock Strategist, has identified seven stocks poised to lead the quantum computing revolution in his report, Beyond AI: The Quantum Leap in Computing Power. Kevin, who recognized NVIDIA’s potential early on, now highlights quantum computing as the next major opportunity for investors. This is a unique chance to position your portfolio ahead of the curve.

Get More Investment Insights

For the latest stock recommendations from Zacks Investment Research, you can download the 7 Best Stocks for the Next 30 Days. Access the free report here.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Lucrative Stocks That Raise Our Concerns

Synopsys rolls out new software tools for designing AI chips

United Natural Q2 Results Surpass Expectations, Sales Outlook Reduced