C's Recovery Boosts Growth Prospects: Is Now the Time to Invest in This Stock?

Citigroup Reaffirms Growth Strategy Amid Economic Uncertainty

Citigroup Inc. has restated its core objectives and financial goals, emphasizing promising expansion prospects despite ongoing global and economic challenges. CEO Jane Fraser addressed these topics and more at the 2026 RBC Capital Markets Global Financial Institutions Conference.

Fraser highlighted that robust economic indicators are fueling the bank’s positive outlook. U.S. corporate activity remains vibrant, driven by investments in artificial intelligence, automation, technology upgrades, and a healthy trend in mergers and acquisitions. Increased consumer spending, along with a supportive corporate environment bolstered by deregulation and tax incentives, is further propelling business growth.

She also pointed out that merging the U.S. Retail Bank with the Wealth Management division is expected to improve client services, boost market share, and foster revenue growth through a more integrated referral system and expanded investment options, including alternative and traditional wealth products. These enhancements are likely to strengthen Citigroup’s performance in the near future.

Looking ahead to the first quarter of 2026, Citigroup anticipates mid-teen percentage growth in investment banking fees and market revenues, supported by strong activity in mergers, acquisitions, and equity capital markets. The company has reaffirmed its goal of achieving 60% operating efficiency in 2026, though initial severance costs from ongoing restructuring may impact early results.

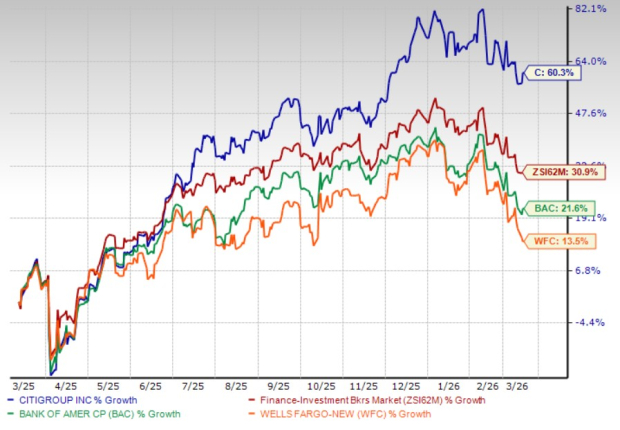

Citigroup’s turnaround is evident in its stock’s performance. Over the past year, shares have surged by 60.3%, outpacing the industry’s 30.9% gain. The bank has also outperformed major competitors, with Bank of America rising 21.6% and Wells Fargo increasing 13.5%.

Stock Price Performance

Source: Zacks Investment Research

With Citigroup reaffirming its growth trajectory and executing its strategic overhaul, investors are questioning whether the stock’s rally can continue or if optimism is already reflected in its price. To assess this, it’s important to review the main growth drivers, risks, and valuation factors influencing Citigroup’s outlook.

Key Considerations for Citigroup

Streamlining Operations and Strategic Focus

CEO Jane Fraser is advancing a multi-year plan to simplify operations and concentrate on core business areas. Since April 2021, Citigroup has been exiting consumer banking in 14 markets across Asia and EMEA.

In February 2026, Citigroup finalized the sale of its Russian banking subsidiary, AO Citibank, to Renaissance Capital, strengthening its capital position and simplifying its balance sheet. This transaction is expected to add approximately $4 billion to the company’s Common Equity Tier 1 capital in Q1 2026. Additionally, Citigroup has secured agreements for investors to acquire a combined 24% equity stake in Grupo Financiero Banamex, following a previous 25% stake sale in December 2025. Preparations are underway for an IPO of its Mexican consumer and SME banking units.

Further divestitures include the sale of its consumer banking business in Poland (May 2025) and its China-based consumer wealth portfolio (June 2024). The bank is also winding down its Korea consumer banking operations. At the RBC Conference, Citigroup reported that its transformation program has reached over 80% of its target state.

These actions are freeing up capital, enabling investments in wealth management and investment banking, which are expected to drive fee income growth. Citigroup projects a 4-5% compound annual revenue growth rate through 2026.

Efficiency Initiatives and Technological Advancements

The bank is prioritizing process optimization, platform simplification, and automation to minimize manual intervention. Citigroup is increasingly leveraging AI tools to enhance productivity, revenue opportunities, and client service. At the RBC Conference, management emphasized AI’s central role across business lines.

This week, Citigroup entered a multi-year partnership with LSEG to modernize its data infrastructure across markets, investment banking, wealth management, trading, and risk functions. The goal is to improve data quality, standardization, and accessibility, enabling more informed decisions and operational efficiencies.

Citigroup has also reorganized its management structure, eliminating layers of bureaucracy to align with its strategy of broader spans of control and reduced complexity.

In January 2024, the bank announced plans to reduce its workforce by 20,000 employees, about 8% of its global staff, by 2026. More than 10,000 positions have already been eliminated, with stranded costs decreasing due to exits in Russia, China, and other markets.

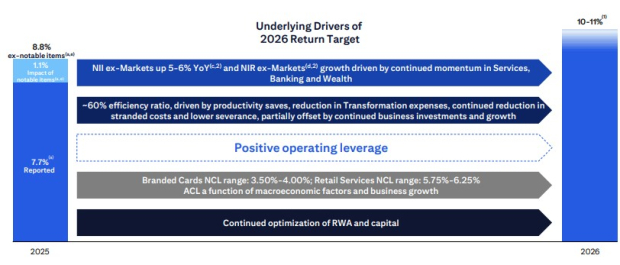

These measures are expected to generate $2-2.5 billion in annualized savings by 2026. The bank aims for a return on tangible common equity (ROTCE) of 10-11% in 2026.

ROTCE Outlook

Source: Citigroup, Inc.

Interest Rate Environment and Loan Growth

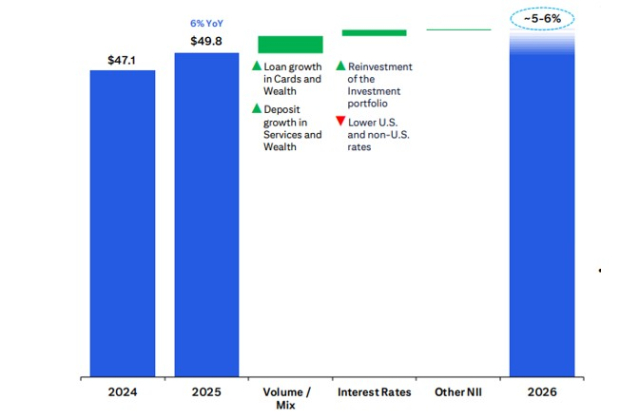

After initial rate reductions in 2024 and three more cuts in 2025, interest rates are currently at 3.50-3.75%. Lower rates are expected to stimulate lending activity, and relaxed regulatory capital requirements will allow more capital to be directed toward loan growth, especially in resilient commercial and consumer sectors. This should support expansion in net interest income (NII).

NII achieved a three-year CAGR of 6.2% through 2025. Management anticipates NII, excluding markets, to grow 5-6% year-over-year in 2026, driven by reduced funding costs, higher loan volumes, and repricing of assets at better yields.

NII Projections

Source: Citigroup, Inc.

Strong Liquidity Supports Capital Returns

Citigroup maintains a robust liquidity position. As of December 31, 2025, its cash, bank balances, and total investments totaled $476.7 billion, while total debt stood at $335.8 billion.

After successfully passing the 2025 Fed stress test, Citigroup increased its dividend by 7.1% to 60 cents per share. Over the past five years, dividends have been raised three times, with a payout ratio of 30% and a yield of 2.3%. Wells Fargo and Bank of America have also increased their dividends multiple times in recent years.

In January 2025, Citigroup’s board approved a $20-billion common stock repurchase program with no expiration date. By year-end 2025, $6.8 billion remained authorized. The bank’s strong capital and liquidity position supports ongoing capital distribution activities.

Asset Quality Concerns

Citigroup’s asset quality has declined, with provisions rising sharply after 2021 due to a deteriorating economic outlook. Provisions grew at a CAGR of 24.5% from 2022 to 2025. Asset quality is unlikely to improve soon, as trade policy impacts and the U.S.-Iran conflict are expected to keep inflation elevated.

Accelerating Growth Momentum for Citigroup

Consensus estimates from Zacks suggest Citigroup’s earnings will increase by 27.9% in 2026 and 18.4% in 2027. The 2026 estimate has remained steady over the past month, while the 2027 estimate has been revised upward.

Estimate Revision Trends

Source: Zacks Investment Research

From a valuation perspective, Citigroup trades at a forward P/E ratio of 10.32, below the industry average of 13.01. Bank of America and Wells Fargo have P/E multiples of 10.94 and 11.04, respectively.

Price-to-Earnings Comparison

Source: Zacks Investment Research

Citigroup Stock: Outlook and Considerations

Citigroup is positioned for sustained growth, supported by its strategic transformation, cost-saving measures, and improved revenue prospects across investment banking, markets, and wealth management. The bank benefits from favorable macroeconomic trends, including robust corporate activity, resilient consumer spending, and the potential for increased loan demand as interest rates decline. Investments in technology and AI, along with workforce optimization, are expected to drive long-term efficiency and productivity gains.

Valuation-wise, Citigroup’s stock trades at a discount compared to the broader banking sector and major peers, suggesting further upside if the bank successfully implements its strategy and achieves projected earnings growth.

However, investors should remain cautious about risks such as deteriorating asset quality, geopolitical tensions, and broader economic uncertainties, which could impact credit costs and profitability in the short term.

Overall, Citigroup’s strengthening fundamentals, solid capital base, and attractive valuation make it a compelling option for long-term investors. Those considering new investments may benefit from waiting for a more favorable entry point.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Lucrative Stocks That Raise Our Concerns

Synopsys rolls out new software tools for designing AI chips

United Natural Q2 Results Surpass Expectations, Sales Outlook Reduced