Archrock Shares: Should You Purchase Now Despite the Premium or Hold Out for a More Favorable Opportunity?

Is Archrock Inc. Worth Its Premium Valuation?

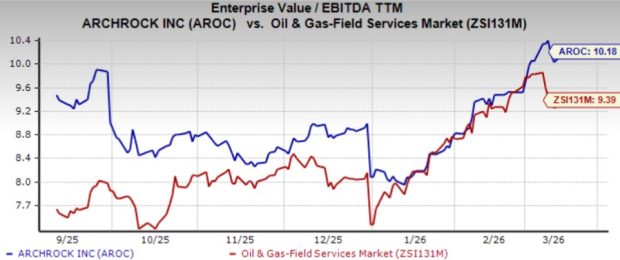

Archrock Inc. is currently trading at a higher valuation compared to its peers, with a trailing 12-month EV/EBITDA ratio of 10.18. This figure surpasses the industry average of 9.39, indicating that investors are paying a premium for the stock.

When compared to other companies in the sector, such as EQT Corporation and Antero Resources, Archrock remains more expensive. Both EQT and AR are also influenced by trends in clean energy demand. Currently, EQT trades at an 8.56x EV/EBITDA, while Antero Resources is valued at approximately 8.83x.

Image Source: Zacks Investment Research

This higher valuation suggests that the market has strong expectations for Archrock’s future. However, investors should carefully evaluate the company’s financial health, growth prospects, and market trends to determine if the premium is warranted.

Archrock Positioned to Benefit from Growing Clean Energy Needs

As the world shifts toward cleaner energy sources to address climate change, the demand for natural gas continues to rise. The expansion of data centers globally is driving up the need for electricity generated from natural gas. Additionally, increasing U.S. LNG exports highlight the growing international appetite for natural gas. These trends create a favorable environment for companies like Archrock, which specializes in natural gas compression services.

According to the latest short-term outlook from the U.S. Energy Information Administration, natural gas spot prices are projected to reach $3.76 per million BTU in 2026, up from $3.53 last year. Higher prices are expected to boost exploration and production activities, which in turn should support demand for compression services.

Stable Revenue Streams and Attractive Dividend Policy

Archrock secures its revenue through fee-based contracts with high-quality clients, ensuring a reliable income stream. With rising demand for its services and these stable agreements, the company is well-positioned to deliver strong cash flows to its shareholders.

Archrock’s dividend coverage ratio stands at an impressive 4.9x, suggesting that its dividend payments are well-supported and likely to remain steady, even if market conditions become less favorable.

Image Source: Archrock Inc

Investment Outlook: Should You Buy Archrock?

Over the past six months, Archrock has surged by 46.1%, outpacing the industry’s 42.2% gain. In comparison, EQT and Antero Resources have seen increases of 22% and 15.4%, respectively.

Image Source: Zacks Investment Research

Given the positive industry trends and the company’s strong performance, paying a premium for Archrock may be justified. The stock currently holds a Zacks Rank #1 (Strong Buy), making it an appealing option for investors seeking exposure to the clean energy sector.

Quantum Computing: The Next Big Opportunity

Quantum computing is rapidly emerging as a transformative technology, potentially surpassing even artificial intelligence in its impact. Major tech companies like Microsoft, Google, Amazon, Oracle, Meta, and Tesla are racing to incorporate quantum computing into their operations.

Kevin Cook, a Senior Stock Strategist, has identified seven companies that are well-positioned to lead in the quantum computing space in his report, Beyond AI: The Quantum Leap in Computing Power. Having previously recognized NVIDIA’s potential early on, Cook now highlights quantum computing as the next significant investment opportunity. Investors have a unique chance to get ahead of this trend.

Additional Resources

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Top Performing Stocks Set for Significant Growth at This Moment

Bitcoin to $78K? Pro traders price in less than 17% odds of a breakout

Q32 Bio Breaks Out — But Can It Hold the Momentum?