February CPI: Met Expectations, but Concerns Remain

Morning FX

The first CPI data after the US-Iran conflict has been released. Whether overall or core, year-on-year or month-on-month, all perfectly matched expectations, making it one of the most uneventful inflation figures in recent years.

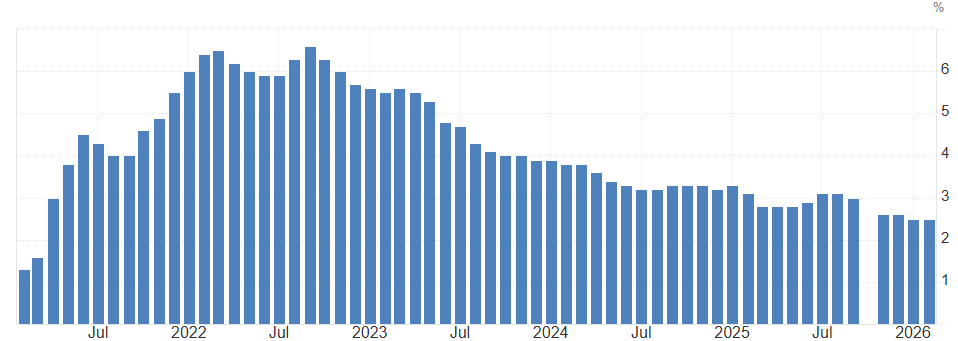

Chart: Core inflation hits a five-year low

At least before the war began, the disinflation trend has been continuing. February CPI grew by 2.4% year-on-year, while core CPI recorded the slowest year-on-year growth in five years at 2.5%. The core month-on-month figure dropped to 0.2%, indicating no sign of accelerating inflation.

I. Current Inflation Is Getting Closer to the Fed’s Target

Since the second quarter of 2024, the year-on-year CPI growth rate has officially entered the “2” era, with CPI growth at ≤3% for 20 consecutive months. Core CPI is cooling down simultaneously and is approaching the Fed's 2% target.

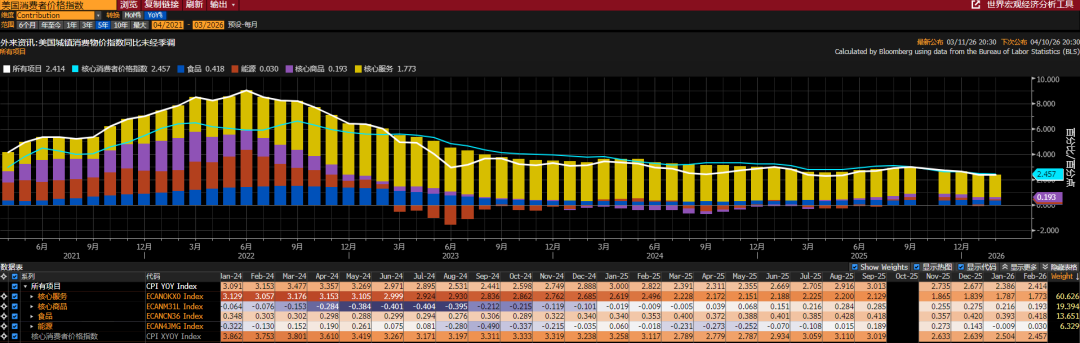

Chart: Inflation Subcategories

According to the latest data, the most stubborn core services contributed only 1.77% to CPI growth—a new low. Housing, which carries the highest weight among core services, as well as transportation and medical prices, have lost upward momentum, weakening inflation resilience.

Goods price increases have been mild as well, with core goods contributing just 0.19% to CPI growth. This means that as long as energy prices are under control, the potential for prices to rebound on their own is very weak.

II. Where Are Future Inflation Risks?

With employment visibly weakening, it should not hinder the Fed’s rate cuts. However, the market’s focus is clearly on soaring oil prices, and with fears of an inflation rebound, the room for rate cuts this year is very limited.

Chart: Rate Cut Room Remains Restrained

Trump launched a strike on Iran at the end of February so the oil price surge may only reflect in next month’s CPI. The Strait of Hormuz remains closed, and Saudi Arabia and the UAE are rerouting their crude oil exports.

Although the International Energy Agency (IEA) plans to release a massive amount of oil from strategic reserves, Brent crude has still climbed above $90. LNG shipments have plummeted to zero, which will undoubtedly continue to drive up overall energy prices.

Chart: Oil Prices Remain High

According to Citi's observations, in the first two weeks of March, US gasoline prices rose by 17%, which may push the March energy sub-index’s month-on-month increase to 7%; producer prices and airfares are also expected to rise.

III. Summary

(1) February inflation continued its favorable trend, with core services price increases moderating and coming closer to the Fed’s target.

(2) However, the market has become numb to the data, focusing instead on skyrocketing oil prices. With the energy choke point at the Strait of Hormuz still blocked, the March CPI energy component is expected to be significantly affected, limiting the Fed’s ability to cut rates.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Optimism's OP Labs cuts 20% of staff to 'do fewer things well'

SEC, CFTC Reach Agreement to Align Cryptocurrency Regulations and Supervision

Microsoft's Aggressive AI Infrastructure Play in Africa: A Race Against DeepSeek and the Compute Paradox

Hackers Hijack Bonk.fun Domain, Deploy Wallet-Draining Phishing Prompt