nVent Electric Shares Climb 1.8% on Earnings Beat but Volume Ranks 463rd

Market Snapshot

nVent Electric (NVT) rose 1.80% on March 11, 2026, with a trading volume of $260 million, ranking 463rd in market activity for the day. The stock’s performance followed a strong quarterly earnings report, where the company exceeded both revenue and profit expectations. Despite the positive momentum, the volume remains moderate compared to broader market benchmarks, suggesting limited short-term speculative activity.

Key Drivers

The stock’s rise was primarily fueled by nVentNVT-- Electric’s Q4 2025 earnings report, which highlighted a 42% year-over-year revenue increase to $1.07 billion, surpassing the $1 billion analyst forecast. Earnings per share (EPS) came in at $0.90, outperforming the $0.89 consensus. This marked a significant improvement from the $0.59 EPS in the same period in 2024. The company also reported a net margin of 18.25% and a return on equity of 15.18%, underscoring its profitability. Analysts noted the 7% revenue surprise and 0.37% EPS beat as key catalysts for investor optimism.

nVent Electric’s forward guidance further bolstered confidence. The firm projected full-year 2026 adjusted EPS of $4.00–$4.15, aligning with sell-side estimates of $3.04. For Q1 2026, it set a narrower range of $0.90–$0.93 EPS, reflecting management’s confidence in sustained demand. The company also highlighted a 30% year-over-year revenue increase in 2025, reaching $3.9 billion, alongside a 21% rise in adjusted operating income to $786 million. These metrics suggest robust operational momentum, particularly in data center and infrastructure markets, which now account for 45% of its vertical exposure.

Analyst sentiment played a supporting role in the stock’s trajectory. While UBS Group and Glj Research maintained “buy” ratings with price targets of $128 and $151, respectively, other firms like Weiss Ratings and Zacks Research downgraded their outlooks to “hold.” The mixed ratings reflect cautious optimism about nVent’s ability to sustain growth amid macroeconomic uncertainties. However, the company’s recent dividend announcement—a $0.21 per share payout with an 0.8% yield—provided additional appeal to income-focused investors.

Operational improvements also contributed to the positive sentiment. nVent ElectricNVT-- reported a record free cash flow of $561 million in 2025, up 31% year-over-year, and expanded its product portfolio with 86 new offerings focused on liquid cooling technologies. The CEO emphasized “outstanding performance” in infrastructure verticals, with order backlogs tripling to $2.3 billion. These developments indicate strong positioning in high-growth sectors, particularly as global demand for data center infrastructure accelerates.

Despite the positive news, the stock faced pre-market pressure, falling 4.15% before the open, likely due to profit-taking following a 15.39% surge in October 2025 after a 3.41% EPS beat. This volatility underscores the market’s sensitivity to earnings surprises and guidance adjustments. However, the company’s ability to consistently exceed revenue forecasts—averaging a 6.05% surprise in recent quarters—suggests a resilient business model capable of navigating sector-specific challenges.

In summary, nVent Electric’s stock performance reflects a combination of strong earnings execution, optimistic guidance, and strategic operational progress. While mixed analyst ratings introduce some uncertainty, the company’s financial metrics and market positioning in high-growth infrastructure segments provide a solid foundation for continued investor interest.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

On-Chain Bitcoin Data Reveals Signs Of Fatigue In Prolonged Sideways Phase

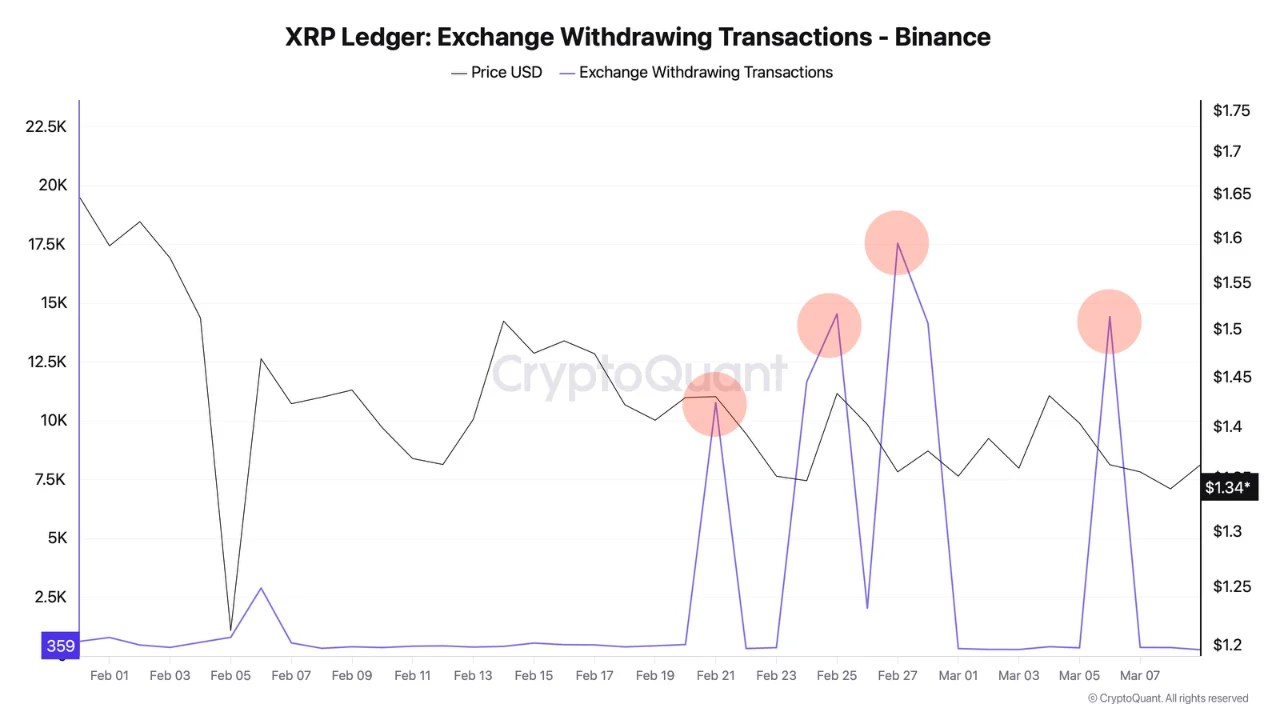

XRP Withdrawal Surge Meets $1.4B ETF Inflows as Capital Returns to Select Altcoins

Russia Becomes The Primary Beneficiary In The Middle East Conflict

HIMS 1W: Subscription growth meets corrective math