3 Reasons Why LYV Carries Risk and One Alternative Stock Worth Considering

Live Nation’s Recent Performance: A Closer Look

In the past half-year, Live Nation’s stock price has slipped by 5.3%, currently sitting at $164.50 per share. This decline stands in stark contrast to the S&P 500’s 3% increase during the same period, leaving many investors questioning their next steps.

Should you consider adding Live Nation to your portfolio, or does it pose unnecessary risk? to help inform your decision.

Why Live Nation May Not Be the Best Bet

Although the stock’s lower price might seem appealing, our confidence in Live Nation remains limited. Here are three key reasons we believe there are more attractive investment options available right now.

1. Sluggish Revenue Expansion

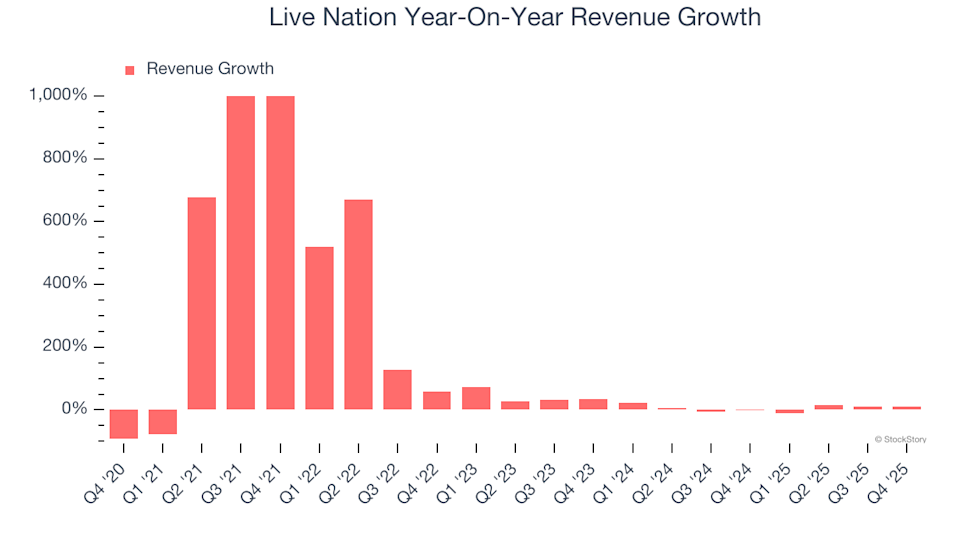

While long-term growth is crucial, companies in the consumer discretionary sector often face rapidly shifting trends and short product cycles, making consistent revenue growth challenging. Live Nation’s revenue has recently lost momentum, with annualized growth of just 5.3% over the past two years—well below its five-year average. The pandemic severely impacted the company in 2020 and early 2021, though it did experience a strong rebound afterward.

2. Margins Remain Under Pressure

Operating margin, which reflects the percentage of revenue left after covering core expenses, is a vital indicator of profitability. It also allows for fair comparisons between companies, as it excludes interest and taxes. Over the past year, Live Nation’s operating margin has improved, averaging 4.3% over the last two years. However, despite some efficiency gains, the company’s cost structure still limits its profitability compared to other consumer discretionary businesses.

3. Declining Free Cash Flow Margin

Free cash flow, though not always highlighted in financial reports, provides a clear picture of a company’s ability to generate cash after all expenses. This metric is difficult to manipulate and is crucial for assessing financial health. Analysts expect Live Nation’s free cash flow margin to dip from 6.6% over the past year to 5.3% in the coming year, indicating a potential weakening in its cash generation capabilities.

Our Verdict

While Live Nation is not fundamentally unsound, it fails to meet our standards for a high-quality investment. Following its recent decline, the stock trades at a forward P/E of 121.4 (or $164.50 per share). Although some may find value here, we don’t see a compelling opportunity at this time. We believe there are stronger alternatives in the market. For example, consider exploring a resilient company behind the popular Taco Bell brand.

Alternative Stocks Worth Considering

Don’t Miss: Top 5 Momentum Stocks. The ideal time to invest in a standout stock is when it’s gaining market attention. These companies not only boast strong fundamentals but are also experiencing significant momentum right now.

Discover which stocks our AI-driven platform is highlighting this week. Access the latest list of high-momentum stocks for free: .

Our selections have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Exlservice, which delivered a 354% return over five years. Start your search for the next breakout stock with StockStory.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Walmart’s Online Sales Rise 24%: Will the Digital Growth Persist?

USD Stablecoins Dominate On-Chain Activity as Regional Alternatives Gain Attention

Can Papa John's Boost Growth Through Digital Initiatives and Loyalty Program Expansion?