Here’s What You Should Understand About Intuit Inc. (INTU) Besides Its Popularity

Intuit: A Closer Look at Recent Performance

Intuit (INTU) has recently become a focal point for many investors, prompting an examination of factors that could influence its short-term trajectory.

Over the past month, Intuit—known for products like TurboTax and QuickBooks—has seen its stock rise by 10.2%, contrasting with a 2.3% decline in the Zacks S&P 500 composite. The Zacks Computer - Software sector, which includes Intuit, posted a modest 0.6% gain during the same period. This raises the question: What might be next for Intuit?

While news and speculation can spark immediate price shifts, long-term investment decisions are ultimately shaped by fundamental company metrics.

Updates on Earnings Projections

At Zacks, the primary focus is on changes to a company’s earnings outlook, as these projections are key to determining a stock’s intrinsic value. Our approach centers on tracking how analysts adjust their earnings forecasts in response to evolving business conditions. When these estimates rise, so does the stock’s fair value, often leading to increased investor interest and upward price movement. Research consistently shows a strong link between earnings estimate revisions and short-term stock price changes.

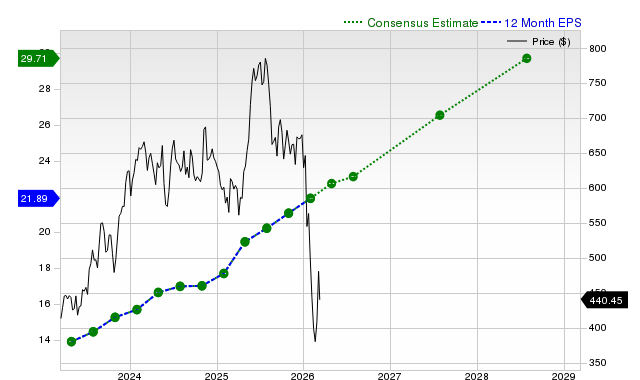

- For the current quarter, Intuit is anticipated to report earnings of $12.48 per share, a 7.1% increase from the same period last year. The consensus estimate has decreased by 2.6% in the past month.

- For the full fiscal year, the consensus estimate stands at $23.14 per share, up 14.8% from the previous year, with a 1.2% increase over the last 30 days.

- Looking ahead to the next fiscal year, the estimate is $26.54 per share, reflecting a 14.7% rise from the prior year, and a 0.4% increase in the past month.

Our proprietary Zacks Rank system, which leverages earnings estimate revisions and other related factors, currently rates Intuit as Rank #2 (Buy), suggesting a positive outlook for the stock.

The following chart illustrates the progression of Intuit’s forward 12-month consensus EPS estimate:

Revenue Growth Forecasts

While earnings growth is a strong indicator of financial health, sustained revenue expansion is essential for long-term profitability. Understanding a company’s revenue potential is therefore critical.

- For the current quarter, Intuit’s consensus sales estimate is $8.52 billion, representing a 9.9% increase year-over-year.

- Projected sales for the current fiscal year are $21.17 billion, and $23.8 billion for the next fiscal year—both reflecting a 12.4% annual growth rate.

Recent Results and Earnings Surprises

Intuit’s most recent quarterly report showed revenues of $4.65 billion, up 17.4% from the previous year. Earnings per share reached $4.15, compared to $3.32 a year earlier.

- Revenue exceeded the Zacks Consensus Estimate by 2.75%.

- EPS surpassed expectations by 13.39%.

- Intuit has consistently beaten consensus EPS and revenue estimates in each of the last four quarters.

Valuation Insights

Assessing a stock’s valuation is vital for making informed investment choices. Comparing current valuation multiples—such as price-to-earnings, price-to-sales, and price-to-cash flow—to historical averages and industry peers helps determine whether a stock is fairly priced.

The Zacks Value Style Score evaluates stocks using both conventional and unconventional metrics, grading them from A to F. Intuit currently receives a D, indicating it trades at a premium compared to its peers.

Summary

The information presented can help investors decide whether Intuit deserves attention amid current market trends. Its Zacks Rank #2 suggests the stock may outperform the broader market in the near future.

Top Semiconductor Stock Highlight

A lesser-known company in the semiconductor sector is poised for significant growth, offering products that industry giants like NVIDIA do not. Positioned to capitalize on the next wave of market expansion, this company is gaining recognition at an opportune time.

With robust earnings and a growing customer base, it stands to benefit from surging demand in Artificial Intelligence, Machine Learning, and the Internet of Things. Global semiconductor manufacturing is expected to soar from $452 billion in 2021 to $971 billion by 2028.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Is Callaway’s Exclusive Focus on Golf Indicating the Start of a New Expansion Period?

Should You Consider Adding Cresco Stock to Your Portfolio After Q4 Results?

Tempus AI Broadens Clinical Assessment of AI-Driven Cancer Diagnostic Tools

Nuclear ETFs Gain Attention Amid Escalating Energy Crisis Driven by Middle East Tensions