Crocs (CROX): Should You Buy, Sell, or Hold After Q4 Results?

Crocs Stock: Limited Growth and Cautious Outlook

Currently, Crocs is priced at $80.50 per share and has delivered a modest 4% return over the past half year, showing little momentum.

Is Crocs a smart addition to your portfolio, or does it carry more risk than reward?

Reasons We Expect Crocs to Lag Behind

We remain skeptical about Crocs’s prospects. Here are three key factors why we believe there are more attractive investment options than CROX, along with a stock we prefer.

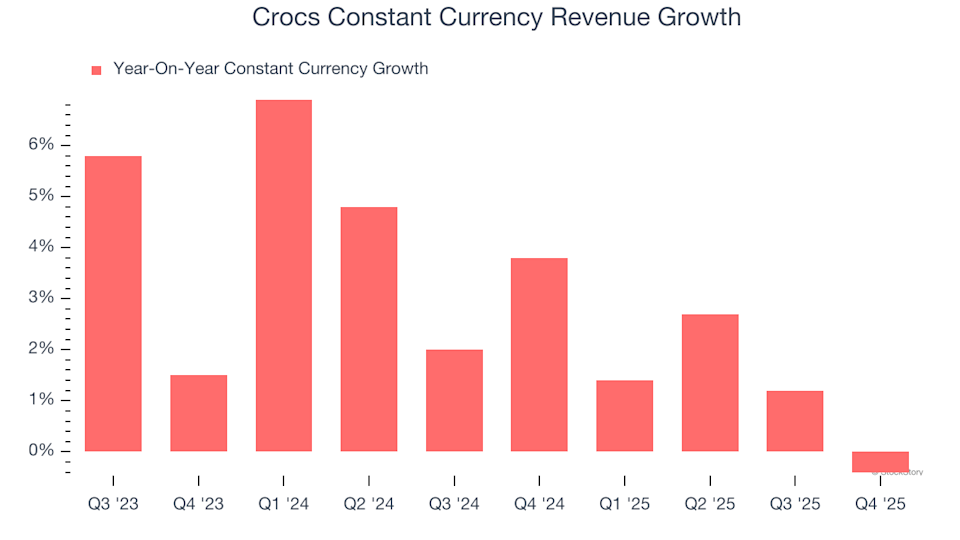

1. Sluggish Constant Currency Revenue Signals Weak Demand

For footwear companies, constant currency revenue is a valuable measure as it strips out the impact of currency fluctuations, offering a clearer view of true demand. Over the past two years, Crocs’s constant currency revenue has grown at an average annual rate of just 2.8%. This lackluster performance suggests the company may need to cut prices or enhance its products to reignite growth—moves that could pressure short-term profits.

2. Free Cash Flow Expected to Improve Marginally

While free cash flow isn’t always highlighted in earnings reports, it’s a crucial metric because it reflects all operational and capital expenditures, making it difficult to manipulate. Cash flow is a true indicator of financial health.

Analysts anticipate a slight uptick in Crocs’s cash conversion over the coming year. Consensus forecasts suggest its free cash flow margin, which stood at 16.3% over the past year, will rise to 18.1%. This improvement could provide more room for investments, share repurchases, and dividends.

3. Declining ROIC Undermines New Investments

We favor companies that consistently generate high returns, but the direction of a company’s return on invested capital (ROIC) often signals future business quality. Unfortunately, Crocs’s ROIC has dropped sharply in recent years. Combined with already modest returns, this trend indicates that lucrative growth opportunities are becoming scarce for the company.

Our Verdict

Crocs does not meet our standards for quality investments. Although the stock trades at a seemingly low forward P/E of 6.2 (or $80.50 per share), its weak fundamentals suggest significant downside risk. We believe there are stronger opportunities elsewhere. Consider exploring a leading Aerospace company with a proven M&A track record instead.

Top Stocks for Any Market Environment

ALSO RECOMMENDED: Top 5 Momentum Stocks. The best time to own outstanding companies is when the market starts to recognize their potential. These businesses not only have strong fundamentals but are also experiencing positive momentum right now—an ideal combination for investors.

Discover which stocks our AI platform is highlighting this week. Check out the latest Strong Momentum stocks—free access available.

Our list features well-known names like Nvidia (up 1,326% from June 2020 to June 2025) as well as lesser-known companies such as Exlservice, which delivered a 354% five-year return.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

DEXTools’ PerpTools Raises $3M to Bring On-Chain Perps to 30 Million Built-In Users

Did Cardano Whales Bet $35 Million on a Token Listing Event Despite Bearish ADA Charts?

CFTC Breaks Silence on Prediction Markets With First Staff Guidance

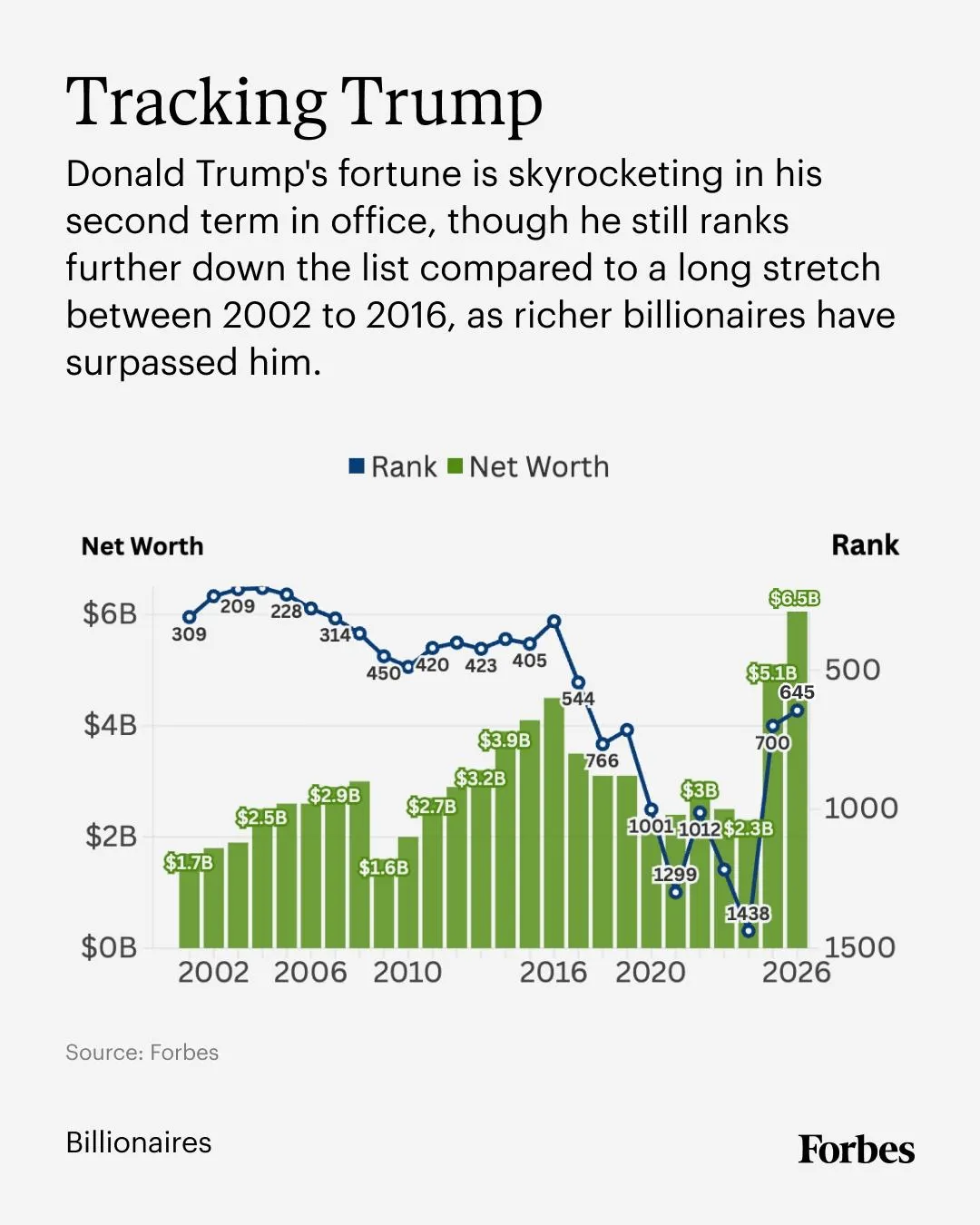

Donald Trump’s Net Worth Climbs to $6.5 Billion as Crypto Ventures Drive Wealth