Can Shake Shack Maintain Its EBITDA Growth Through Operational Efficiency?

Shake Shack's Operational Efficiency Fuels Profit and EBITDA Growth

Shake Shack Inc. has demonstrated that streamlining operations is playing a crucial role in boosting both its profitability and EBITDA. In 2025, the company achieved a 15.4% increase in revenue, reaching $1.45 billion, while adjusted EBITDA climbed approximately 19.5% year-over-year to around $210 million. Leadership credits these gains to disciplined execution and a series of initiatives aimed at improving margins throughout the organization.

Labor Model Transformation Drives Results

Rather than reducing its workforce, Shake Shack revamped its labor strategy to better align staffing with peak demand periods. This approach led to a notable rise in creditable labor performance, with over 90% of locations hitting labor targets in 2025, compared to just half in mid-2024. Enhanced scheduling and less overtime contributed to lower labor expenses as a share of sales, all while maintaining high service standards.

Enhanced Restaurant Operations and Team Stability

Operational upgrades have also made restaurants more productive. Average customer wait times dropped from about seven minutes in 2023 to under six minutes in 2025. Employee retention improved as well, with tenure increasing by nearly 40%, signaling a more stable workforce and better in-store performance.

Supply Chain Improvements Support Margins

Shake Shack also strengthened its supply chain by broadening its supplier network, optimizing logistics, and conducting thorough sourcing reviews. These actions helped offset commodity cost pressures, such as double-digit beef price hikes in the latter half of 2025, ultimately protecting profit margins.

Future Outlook: Sustained EBITDA Growth

Looking forward, management expects that ongoing operational discipline will continue to drive earnings. For 2026, the company projects adjusted EBITDA growth in the low-to-high teens, supported by moderate price increases, supply chain efficiencies, and further operational enhancements. The longer-term vision for 2027 includes maintaining annual EBITDA growth in the low-to-high teens, alongside continued expansion reachable at the restaurant level.

If Shake Shack maintains its focus on labor optimization, supply chain improvements, and operational upgrades, these strategies could help the company sustain its EBITDA growth through 2026 and beyond.

How Do Competitors Stack Up on Profitability?

Shake Shack’s emphasis on efficiency reflects similar moves by other leading fast-casual brands, including Chipotle Mexican Grill and Restaurant Brands International.

- Chipotle Mexican Grill has achieved strong margins by streamlining kitchen operations, expanding digital ordering, and introducing the Chipotlane drive-thru. These initiatives have enabled higher order volumes and improved labor productivity, fueling consistent margin and EBITDA growth.

- Restaurant Brands International, which owns Burger King and other major chains, has focused on operational upgrades through its “Reclaim the Flame” turnaround plan. Investments in restaurant modernization, technology, and supply chain efficiency are designed to boost franchisee profitability and overall system performance.

In this competitive landscape, Shake Shack is pursuing similar operational strategies—labor optimization, supply chain diversification, and enhanced restaurant execution—to maintain its EBITDA momentum.

Shake Shack’s Stock Performance, Valuation, and Analyst Estimates

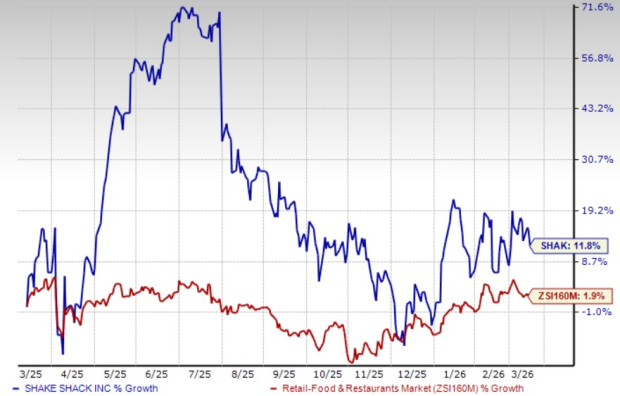

Over the past year, Shake Shack’s stock has risen 11.8%, outpacing the broader industry’s 1.9% gain.

Price Performance

Image Source: Zacks Investment Research

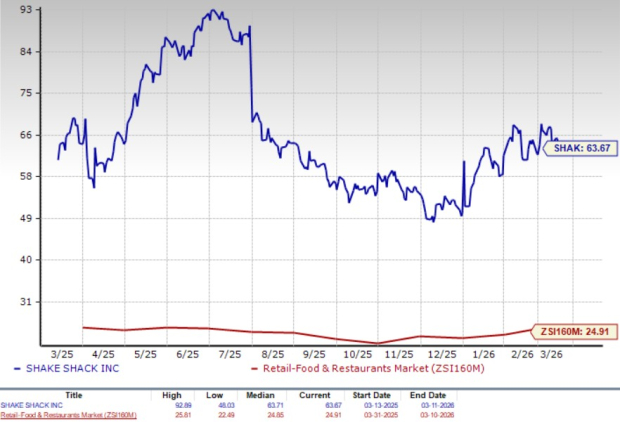

Currently, Shake Shack trades at a forward 12-month price-to-earnings (P/E) ratio of 63.67, compared to the industry average of 24.91.

Forward P/E Ratio (F12M)

Image Source: Zacks Investment Research

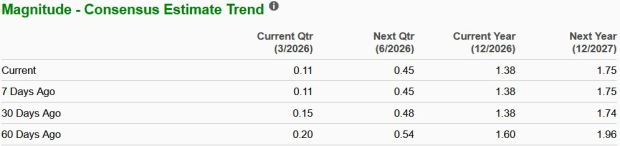

In the last 60 days, the Zacks Consensus Estimate for Shake Shack’s 2026 earnings per share has declined, as illustrated below.

Image Source: Zacks Investment Research

Shake Shack currently holds a Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

First Majestic Silver Crumbles 4.2% Amid Earnings Growth vs. Revenue Concerns Ranks 354th in Trading Volume

Centene Shares Drop 3.6% Despite Surpassing Earnings Estimates, Trading Volume Places 353rd for the Day