Alcoa Shares Approach Yearly Peak: What’s the Best Strategy for This Stock?

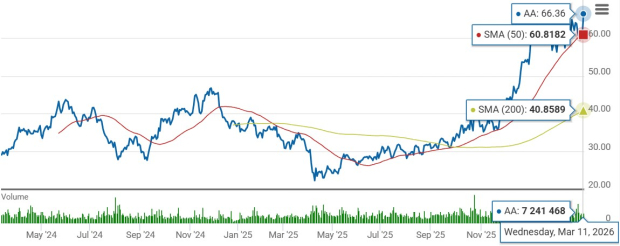

Alcoa Corporation Approaches 52-Week High

Alcoa Corporation (AA) has recently experienced significant upward momentum, with its share price nearing its 52-week peak of $68.40. The stock ended the previous trading session at $66.36, just 3% below its highest mark. Over the past half-year, Alcoa’s stock has soared by 97.5%, outperforming both the Zacks metal products sub-industry, which rose 75.4%, and the S&P 500, which gained 3.3% in the same period.

Other companies in the sector, such as Century Aluminum Company (CENX) and Constellium SE (CSTM), have also posted strong returns, climbing 123% and 67%, respectively, during this timeframe.

AA Surpasses Industry and Market Benchmarks

Image Source: Zacks Investment Research

Alcoa’s shares are currently trading above both their 50-day and 200-day moving averages, signaling robust upward momentum and price stability. This trend points to positive investor sentiment and confidence in the company’s financial outlook and long-term strategy.

AA Maintains Position Above Key Moving Averages

Image Source: Zacks Investment Research

Key Drivers Behind Alcoa’s Growth

Alcoa has benefited from rising aluminum prices, which have been driven higher by geopolitical tensions in the Middle East, particularly between Israel and Iran. Disruptions in the Strait of Hormuz—a vital shipping route—have impacted regional aluminum supply, pushing global prices upward.

Strong demand for aluminum, coupled with increased tariffs on imports, has further supported domestic producers. In June 2025, the U.S. government raised tariffs on imported aluminum to 50% to address trade imbalances and strengthen the local industry, benefiting companies like Alcoa.

Robust demand from the electrical and packaging sectors continues to fuel growth in Alcoa’s Aluminum segment. The company has also boosted its production capacity by restarting smelters in San Ciprián (Spain), Alumar (Brazil), and Lista (Norway). For 2026, Alcoa anticipates producing between 2.4 and 2.6 million tons of aluminum, with shipments expected to reach 2.6 to 2.8 million tons.

The Alumina segment is set to gain from increased productivity at the company’s refineries, though the closure of the Kwinana refinery has weighed on output and shipments. Alcoa projects alumina production in 2026 to range from 9.7 to 9.9 million tons, with shipments between 11.8 and 12.0 million tons.

Looking ahead, Alcoa is well-positioned to capitalize on rising demand for lightweight materials in electric vehicles, rechargeable batteries, and advanced aluminum alloys for the aerospace industry.

Short-Term Challenges Remain

Despite its strengths, Alcoa faces several near-term obstacles. Operating costs have risen, with the cost of sales increasing by 6% year-over-year in 2025 and accounting for 82.9% of net sales. Selling, general, and administrative expenses also climbed by 9%. If these expenses are not managed effectively, the company’s profit margins could come under pressure in the coming quarters.

Additionally, Alcoa’s debt load remains high. At the end of the fourth quarter, the company reported total debt of $2.44 billion, while cash and cash equivalents stood at $1.6 billion, raising concerns about its financial flexibility.

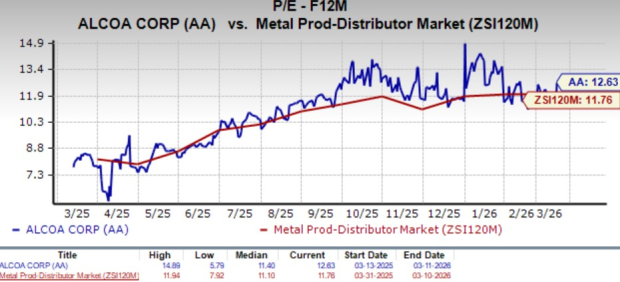

Valuation Overview

Alcoa’s current valuation is relatively high, with the stock trading at a forward 12-month price-to-earnings (P/E) ratio of 12.63, above the industry average of 11.76. This premium valuation could expose the stock to downside risk if market sentiment shifts.

In comparison, Century Aluminum (CENX) and Constellium (CSTM) are trading at lower forward P/E ratios of 8.57 and 11.98, respectively, making them more attractively valued relative to Alcoa.

Forward Price-to-Earnings Comparison

Image Source: Zacks Investment Research

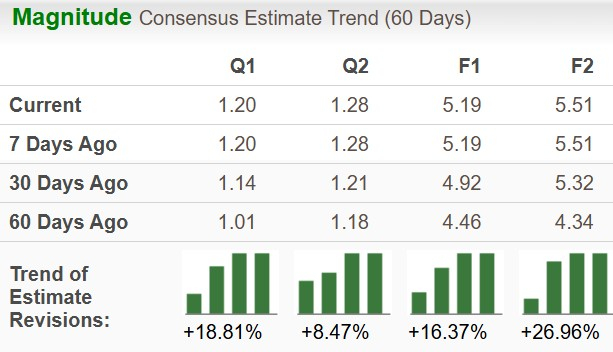

Upward Revisions in Earnings Estimates

Analysts have become more optimistic about Alcoa’s future performance, as reflected in upward revisions to earnings estimates over the past two months. Projections for 2026 earnings per share have increased by 16.4% to $5.19, while estimates for 2027 have risen by 27% to $5.51 per share.

Image Source: Zacks Investment Research

Conclusion: Should You Buy AA Stock?

While Alcoa demonstrates solid growth drivers and improved earnings forecasts, short-term risks such as elevated costs and a high valuation limit its immediate upside. Current shareholders may consider holding their positions, but potential investors might want to wait for a price pullback before entering.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Petrol price surge is unlikely to boost electric vehicle sales, automakers claim

Italy fines Intesa Sanpaolo 18 million euros for illicit processing of customer data

DXP Enterprises (DXPE) Stands Out as a Remarkable Growth Stock: Here Are 3 Key Reasons

Shiba Inu (SHIB) Records Surprise 4.2% Rally to Overtake Zcash (ZEC) Among Top 30 Cryptocurrencies