(Kitco News) – While precious metals investors might worry about depleting gold mines or massive new discoveries impacting supply, and the potential for collusion among gold miners to control prices, there are a number of very good reasons why none of these scenarios will actually come to pass, according to the World Gold Council (WGC).

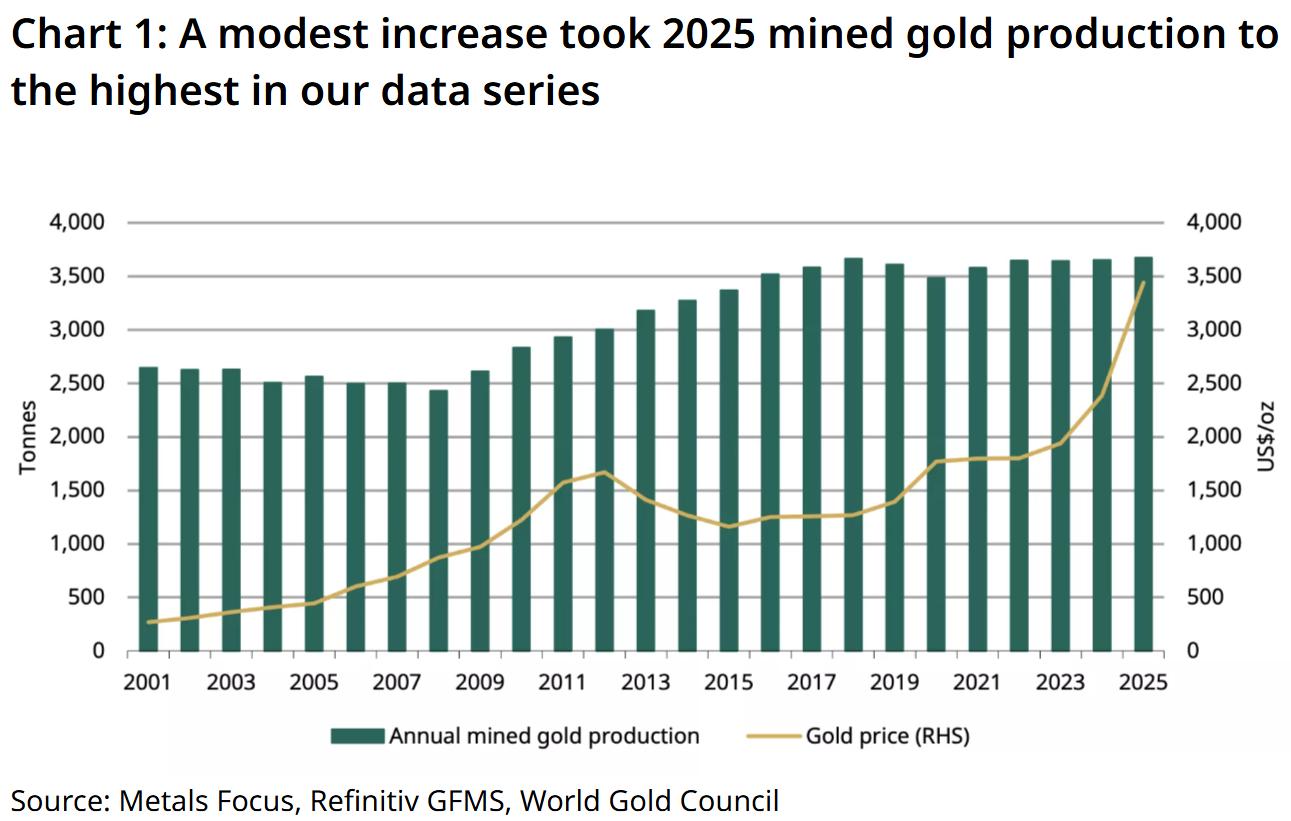

In a detailed analysis published on Thursday, WGC Senior Market Strategist John Reade and Head of Research, Asia Pacific, Ray Jia begin by noting that mined gold production reached its highest level on record in 2025 as prices hit all-time highs.

“Global miners produced 3,672t of gold, a modest y/y increase of 1% and the highest in our data series – albeit this may be subject to revisions when more data becomes available,” they wrote. “And we expect mined gold production to further increase in 2026 – at a mild pace – as operations resume at two major mines.”

“Based on the annual reports of major gold mining companies, the 2026 production outlook is generally cautious – most forecast declines compared to 2025,” they warned. “Without more discoveries, current reserves naturally deplete – perhaps at a faster pace should the gold price keep rising – which could possibly encourage production to accelerate.”

The authors said this has raised several concerns from investors: Are we approaching a structural shortage of mineable gold?; If not, when can a meaningful supply response be expected?; Should any major discoveries be found, will they suppress the gold price?; and Could gold supply be manipulated?

“There are two parts related to this question – the broader gold supply and mined production,” they wrote. “Our answer to both is: not likely.”

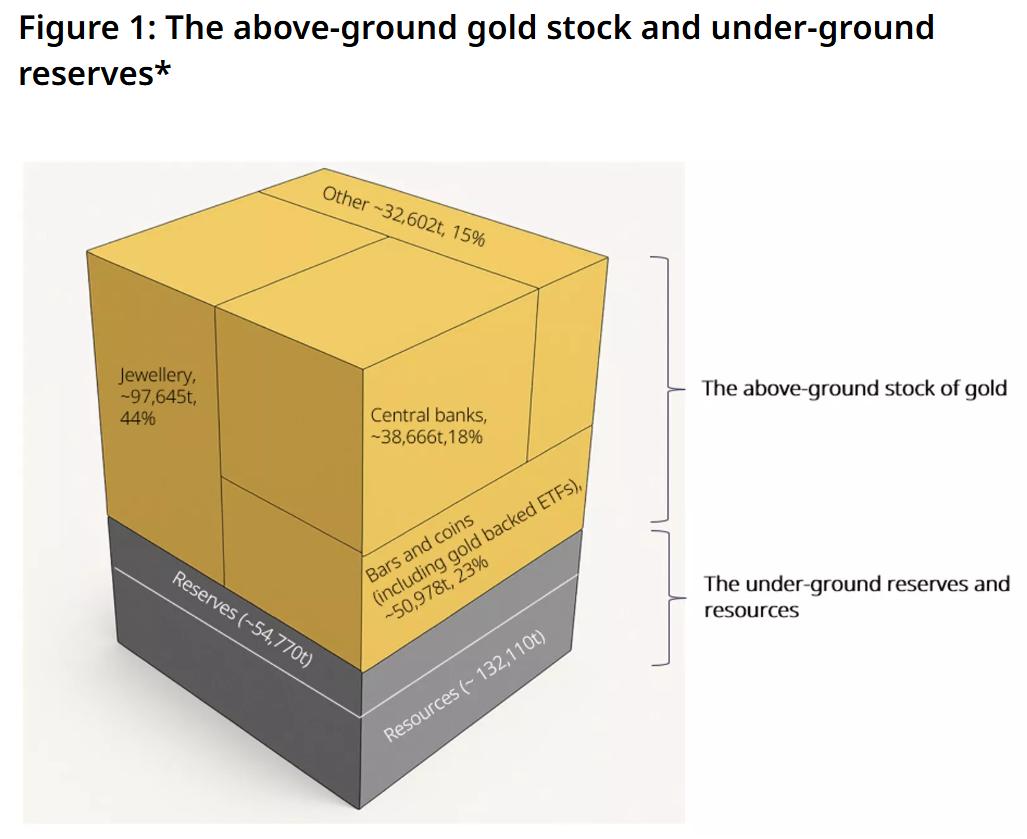

First, Reade and Jia assert that the world is not likely to run out of overall gold supply, as mined gold is not the only source. “While mined gold may be plateauing as noted previously, recycled gold supply comes from various sectors,” they said. “[T]otal above-ground gold amounts to 219,891t. And because gold is virtually indestructible, almost all of it is available to come back to the market under certain market conditions.”

“For instance, when the gold price is high, it may trigger sellbacks of gold jewellery from consumers and more industrial recycling – factors that are far more responsive to price than mined gold production.”

Secondly, Reade and Jia said the market is unlikely to run out of gold deposits to mine either.

“Metals Focus estimates that there are 54,770t of gold reserves by the end of 2025, i.e. the portion of an ore deposit that can be economically extracted under conditions as of 2025, whereas the US Geological Survey (USGS) data estimates gold reserves to be around 64,000t,” they noted. “And resources – the total potential of gold deposits based on geological evidence and sampling, including the part that is economically minable and the part that is not – are estimated to be 132,110t, based on data from Metals Focus.”

“There is a common misconception that proven gold reserves can only last ~15 years at the 2025 rate of production,” they said. “But it is important to note that estimates of below-ground reserves have remained stable for decades even as gold is being continually mined out.”

Reade and Jia attribute this stability is explained by several factors, which they say will likely continue.

“Lower-grade deposits once unprofitable become economically viable – in other words, they move from resources to reserves as the gold price increases,” they wrote. Another factor is new discoveries, even if they occur at a slower pace. “When a gold deposit is discovered, sufficient reserves are drilled out to justify the project construction. But as some of the deposits deplete, further exploration often takes place, keeping total resources relatively stable.” Also, after a mine is brought into production, “exploration geologists start to look for near-to-mine resources (often small deposits, sometimes known as satellite deposits), that can supplement reserves.” And the advancement of mining technology also has the effect of making new discoveries more viable and extending current usable supply.

“In conclusion, while there is a slim possibility that we run out of “easy” and “cheap” gold to mine – if all discoveries stopped, technological advancement and a price that is high enough could see gold extracted from previously unfeasible supply sources,” they said.

A related question for investors is how major changes in gold mining output could impact the price of the yellow metal. Reade and Jia point out that even when this does occur, it happens with a considerable delay.

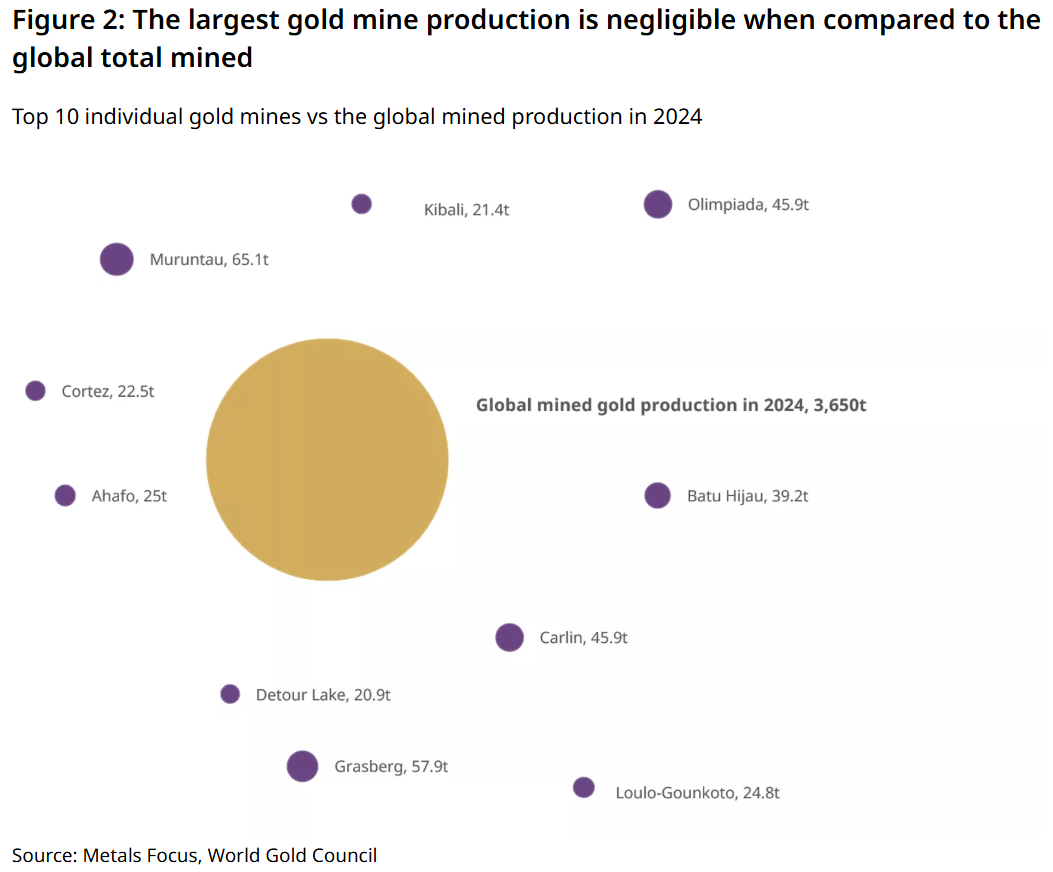

“Changes to gold production are normally only reflected in changes to the price over the long term; any immediate impact will likely be mild,” they said. “First, any new discovery is unlikely to be large enough to move the needle. Based on data from Metals Focus, the Muruntau mine in Uzbekistan was the largest in the world in 2024, producing 65t of gold during that year. But compared to the world total of 3,650t, it is small. Second, as we previously noted, any new discovery is likely to take more than a decade to be explored, permitted, built and ramped up to full production. The market will have had time to absorb the news and may gradually price in such expectations, making little impact in the short term.”

The authors cite modelling from Qaurum, which suggests that “every ~25t gold supply increase/decrease leads to a c.1% decline/rise in the gold price during the same period,” but they argue that the WGC’s own modelling and real world work differently. “For instance, any decline in the gold price caused by a rise in mine production may lift demand for gold jewellery and industrial use, offsetting the negative price impact, they noted. “Furthermore, recycled gold supply may also taper off as the gold price declines, counteracting the increase in mine production. Lastly, changes that feed through each segment may not happen during the same period, further complicating the impact.”

“It is important to note that it is the overall supply and demand conditions that collectively impact the gold price,” they added.

Another concern for precious metals investors is the possibility that gold producers could collectively manipulate or control gold prices through concerted action to impact mined gold supply.

The authors argue that in the real world, this is probably not possible.

“First, gold supply comes from various sources, including mine production and recycling,” they said. “If we assume that gold miners collectively limit production to drive up the price, recycled gold supply is likely to rise in response to the higher gold price as it often does, potentially inserting pressure on the price. With above-ground gold holdings at 219,891t, the potential for recycled gold supply is vast – although not all of it can be mobilised quickly – compared to mined gold supply.”

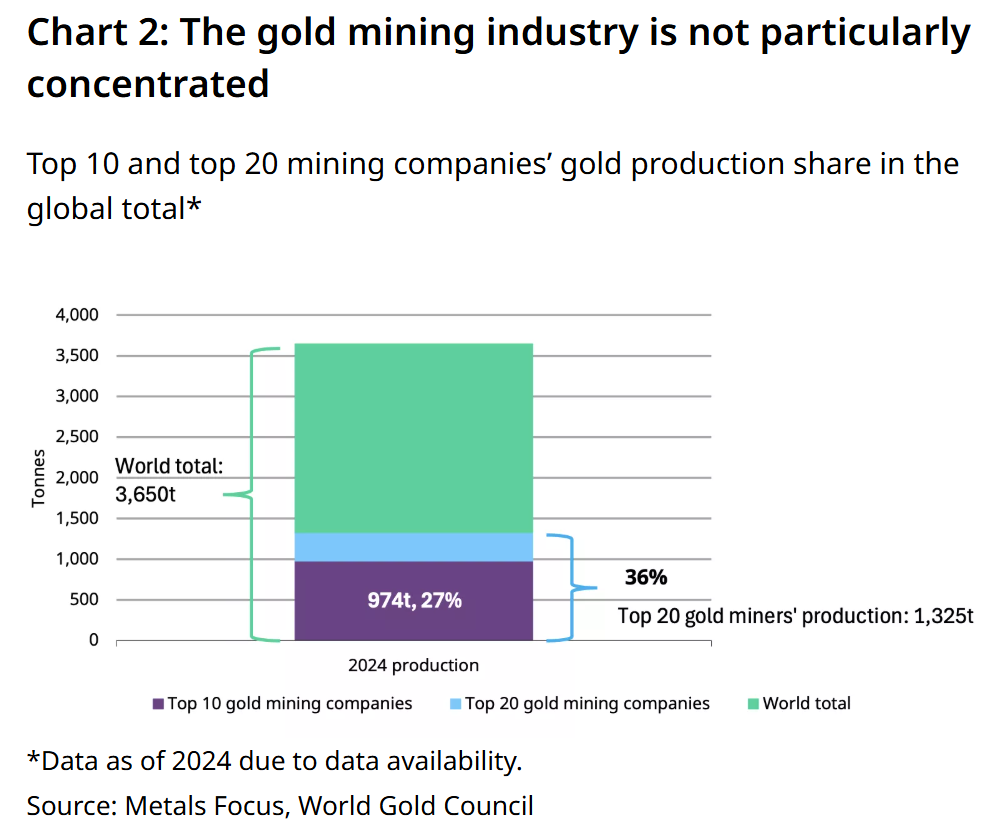

The second factor that mitigates the possibility of producers successfully manipulating gold prices or the gold supply is the relatively diverse and diffuse nature of the global gold mining sector.

“The top ten gold producers accounted for 27% of total global production,” they noted. “It would be difficult to persuade all gold miners to act collectively, not to mention ASGM supply, which accounted for around 20% of the global total in 2024, based on our estimate; these ASGM sources are even less likely to be responsive to attempts to constrain production. Lastly, monopolistic actions, such as co-ordinating production cuts across the gold industry, are illegal in many jurisdictions.”

Reade and Jia said that when all of the mitigating factors on the mining supply side are taken together, they suggest that overall supply is likely to remain relatively stable even as known reserves are depleted, while the supply/price delay and decentralized nature of the gold mining industry also serve to reinforce gold’s long‑term market stability.