Middle East conflict triggers global 'deficit panic': 30-year U.S. Treasury yield approaches 4.9%, wiping out all gains in this year's bond market!

Concerns over fiscal spending triggered by the US-Iran war are sweeping through the global bond market, with long-term government bonds facing a new wave of sell-offs.

On Friday, the 30-year US Treasury yield climbed to nearly 4.90%, approaching a new one-month high. Since the war broke out on February 28, this yield has surged more than 20 basis points, wiping out all year-to-date gains in US Treasury bonds. The Bloomberg index tracking US Treasury returns has nearly returned to zero for the year.

This sell-off is not unique to the United States. From the UK to Germany, from Australia to Japan, global bond yields have surged across the board, with long-term government bonds under general pressure.

Investors are concerned that, as war-related expenditures continue to rise, governments worldwide will have to resort to heavy borrowing to cover defense spending and subsidize households impacted by energy price shocks. This prospect, combined with inflationary pressure from surging oil prices, poses a dual threat to the fixed income market.

Dual Pressure of Fiscal and Inflation Squeeze Long-End Rates

The recent rise in long-term yields has been driven by both inflation expectations and concerns over fiscal deterioration.

Notably, 30-year Treasury Inflation-Protected Securities (TIPS) yields rose by 7 basis points this week. At the same time, actual short-term rates fell due to expectations for slowing growth—this divergence shows that market worries about long-term fiscal sustainability now go beyond purely cyclical economic concerns.

“Long-end rates tell a fiscal story, and a government credibility story,” said Gang Hu, managing partner at Winshore Capital Partners. “They reflect expectations that Trump will have to spend to pay for the war and subsidize consumers facing higher oil prices.”

The US Congress is currently debating up to $50 billion in additional war appropriations, but the government has not yet disclosed estimates for military expenditures. Meanwhile, the US budget deficit remains about $1 trillion for the five months through February. The Supreme Court’s reversal of the trade tariff ruling has also caused a sudden loss of a revenue source that could have provided tens of billions to the fiscal balance.

“This is happening at an inflection point for tariff revenue—and tariffs themselves are inflationary, and so is war,” said Matt Eagan, portfolio manager at Loomis, Sayles & Co., which manages more than $430 billion in assets. "This will only worsen the deficit problem."

Thursday's $22 billion 30-year Treasury auction saw decent demand after yields rose sharply, but market participants are not optimistic about the outlook. “I don’t see much appeal in 30-year Treasuries unless yields break above 5%,” Eagan added.

Global Borrowing Surges, Bond Market Stress Spreads Outward

Fiscal pressures are not limited to the United States. In Europe, governments face the twin pressures of rising defense spending and potential energy subsidies. European Commission President Ursula von der Leyen this week proposed several countermeasures, including a gas price cap. Nomura’s Senior European Economist Andrzej Szczepaniak noted that European governments may repeat the playbook from the 2022 energy crisis and use joint EU debt issuance to finance crisis spending, which would create structural pressure on the Eurozone bond market.

Asia is also unable to remain unaffected. Australia, Singapore, and other countries have successively increased defense budgets, and Japan’s defense spending this year is expected to reach a record high. Commonwealth Bank of Australia strategist Carol Kong pointed out that the Iran conflict may further boost long-term spending pressures on Asian governments, making fiscal consolidation more complicated. “Rising inflation expectations will also push up bond yields, and Asia—including Japan—is no exception.”

Chris Arcari, head of capital markets at Hymans Robertson, noted that compared to the 2022 energy crisis triggered by the Russia-Ukraine conflict, governments' current fiscal space is even more limited, with both debt burdens and interest costs higher. This time, bond markets may be less willing to bankroll such large-scale fiscal expansion and will at least demand higher real yields as compensation.

Investors broadly believe that if the conflict continues and governments keep ramping up spending, the ongoing expansion of global government bond supply will maintain pressure on long-end yields. Demanding higher risk premiums for long-term bonds will become the new normal in the market.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Veon's core profit rises on digital services as it prepares Starlink deployment in Bangladesh

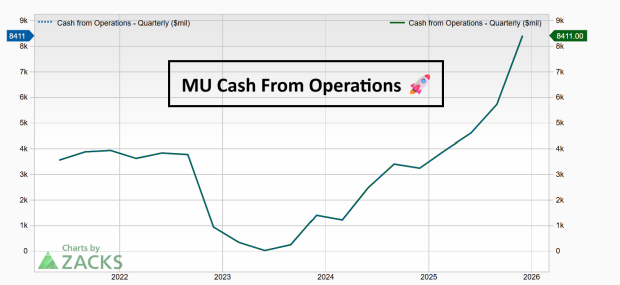

Bull Pick Today: Micron (MU)

Bitcoin surges to $72K: ETF investments and sudden supply gaps

TRUMP ($TRUMP) 24-hour fluctuation 40.3%: Whale accumulation drives rebound from lows