3 Arguments for Selling VNT and One Alternative Stock Worth Buying

Vontier Stock Performance: Recent Trends and Investor Concerns

In the past half-year, Vontier’s share price dropped to $36.21, resulting in a 15.3% loss for investors. This decline stands in contrast to the S&P 500’s 2.3% gain over the same period, leaving shareholders questioning their investment strategy.

Should you consider adding Vontier to your portfolio, or is it a potential liability?

Reasons We Expect Vontier to Lag Behind

Despite the lower valuation, we remain cautious about Vontier’s prospects. Below are three key factors that make us prefer other investment opportunities over VNT.

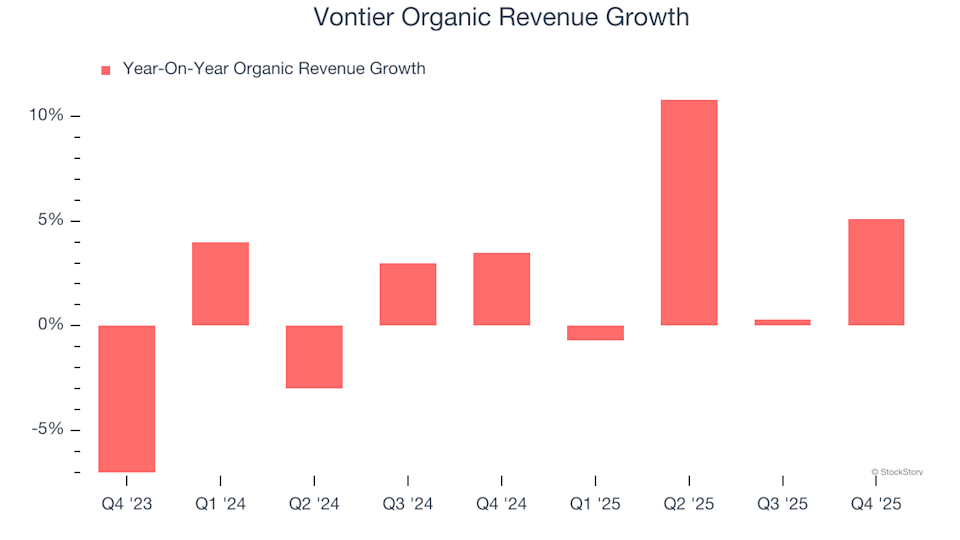

1. Modest Organic Growth Points to Weakening Core Demand

Organic revenue, which excludes the effects of acquisitions, divestitures, and currency changes, is a critical measure for evaluating companies in the Internet of Things sector. It offers a clearer view of Vontier’s underlying business performance.

Over the past two years, Vontier’s organic revenue has grown at an average annual rate of just 2.9%. This lackluster growth suggests the company may need to enhance its offerings, pricing, or sales approach, potentially complicating its operations.

2. Limited Revenue Expansion Forecasted

Analyst projections for future revenue provide insight into a company’s growth outlook. While forecasts are not always precise, accelerating sales typically support higher valuations, whereas slowing growth can have the opposite effect.

Wall Street expects Vontier’s revenue to increase by only 1.6% over the next year. Although this suggests some improvement from new products and services, the growth rate remains below the industry average.

3. Stagnant Earnings Per Share

Tracking changes in earnings per share (EPS) over time reveals whether a company’s additional sales are translating into profits. Sometimes, revenue can rise due to heavy spending on marketing, which doesn’t always benefit the bottom line.

Vontier’s EPS has remained flat over the last five years, even as its annual revenue grew by 2.6%. This indicates that profitability per share has declined as the company expanded.

Our Takeaway

While we appreciate companies that deliver value to their customers, we are not optimistic about Vontier’s outlook. The stock is currently trading at 10.9 times forward earnings (or $36.21 per share), a reasonable valuation. However, the company’s fundamental weaknesses introduce significant downside risk. We believe there are more attractive investment options available. For example, consider exploring .

Alternative Stocks Worth Considering

WHILE YOU’RE HERE: Discover the Top 9 Consistently Outperforming Stocks. The most successful stocks don’t just beat the market once—they do it repeatedly. These companies are characterized by strong revenue growth, increasing free cash flow, and exceptional returns on capital. The market has already recognized their achievements.

Our AI-driven platform indicates that these stocks still have room to run. See which nine companies made our list this week—completely free.

Our selections include well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Exlservice, which delivered a 354% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

High Roller Q4 Profits Increase Year Over Year Due to Expense Management and Strategic Changes

CNTX Breaks Out — But Volume Remains a Question Mark

EUR/USD: Forecasts cut on energy shock – Rabobank

Corporate Bitcoin Accumulation Sparks Debate On Delayed Market Impact