3 Reasons to Steer Clear of TXT and One Alternative Stock Worth Buying

Textron’s Recent Performance: A Closer Look

In the last half-year, Textron has delivered impressive returns, outperforming the S&P 500 by 10.1%. The stock has risen to $92.42, marking a robust 12.4% gain. Such results may leave investors questioning their next move.

Should you consider adding Textron to your portfolio, or is it a potential risk?

Why Textron Fails to Impress

While shareholders have benefited from Textron’s recent price appreciation, we remain cautious. Below are three key reasons why we’re not enthusiastic about TXT and prefer alternative investments.

1. Underwhelming Long-Term Revenue Growth

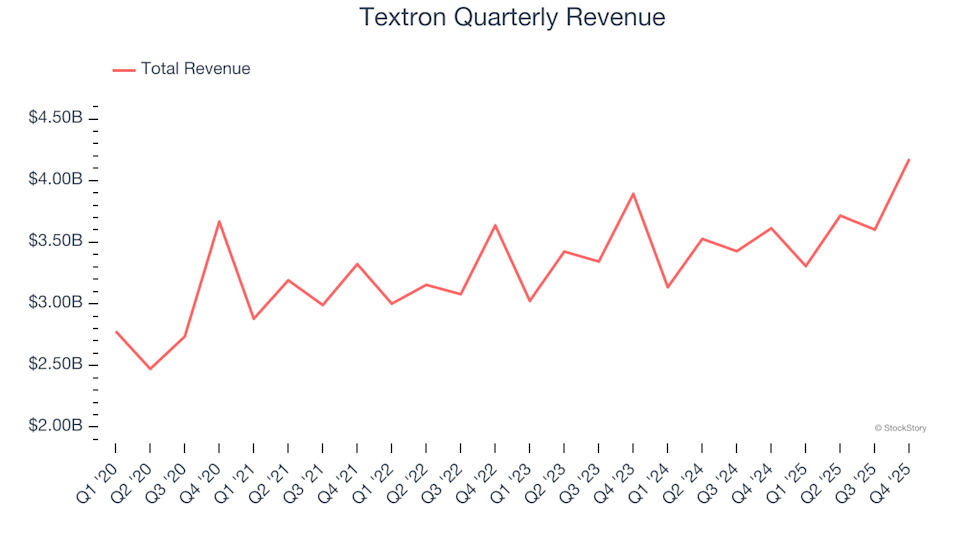

Consistent, long-term growth is a hallmark of high-quality companies. Although any business can post strong results for a few quarters, sustained expansion is what sets the best apart. Over the past five years, Textron’s sales have grown at a modest 4.9% compound annual rate, which falls short of our expectations for the industrial sector.

2. EPS Growth Lags Behind Expectations

While long-term earnings trends are important, we also examine recent earnings per share (EPS) to spot any shifts in the company’s trajectory.

Textron’s EPS has increased by just 4.5% annually over the last two years, mirroring its slow revenue growth. This indicates the company has maintained its profitability per share as it expanded, but without notable acceleration.

3. Declining Free Cash Flow Margin

At StockStory, we place significant emphasis on free cash flow, as it ultimately determines a company’s financial flexibility—unlike accounting profits, cash flow pays the bills.

Textron’s free cash flow margin has dropped by 3.4 percentage points over the past five years. If this trend persists, it could suggest rising capital requirements and greater investment needs. For the most recent twelve months, the free cash flow margin stood at 6.3%.

Our Verdict

Textron is not a poor business, but it doesn’t meet our standards for quality. Despite its recent outperformance and a forward P/E of 14.4 (with shares at $92.42), we don’t see a compelling buying opportunity at this time. We believe there are more attractive options available. For example, consider exploring one of Charlie Munger’s favorite companies.

Stocks We Prefer Over Textron

Don’t Miss: This Week’s Top 6 Stock Picks—In today’s fast-moving market, distinguishing between genuinely strong stocks and overpriced ones is crucial. With AI shaking up entire industries, you need more than just a list of reputable companies.

- Our AI identified Palantir before its 1,662% surge.

- It flagged AppLovin ahead of its 753% rally.

- Nvidia was spotted before its 1,178% climb.

Each week, our system highlights six new stocks that meet our rigorous criteria.

Our recommendations have included well-known names like Nvidia (up 1,326% from June 2020 to June 2025) and lesser-known companies such as Kadant, which delivered a 351% return over five years.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Analyst Revives IMF SDR Theory Around XRP and Ripple

Energy is no longer a wasted investment — this is what investors are actually purchasing

Is Workiva Stock Worth Buying After Investment Firm 13D Initiated a $4.5 Million Stake?

Blockchain Campaign Turns Epstein File Obsession Into Funding for Women’s Shelter