OXY Surpasses Sector Performance Over the Last Month: Should You Buy, Hold, or Sell?

Occidental Petroleum Outpaces Industry Peers

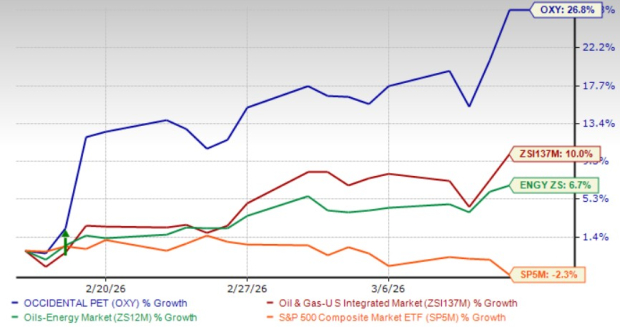

Over the past month, Occidental Petroleum Corporation (OXY) has seen its stock price climb by 26.8%, notably outpacing the Zacks Oil and Gas-Integrated-United States industry, which rose by 10% during the same period. OXY has also surpassed the performance of its broader sector and the Zacks S&P 500 composite index.

As a cost-efficient operator with substantial assets in the Permian Basin, Occidental Petroleum stands to benefit from the recent surge in oil prices, particularly as geopolitical tensions persist in the Middle East. While the company maintains international operations, it does not rely on the Strait of Hormuz for oil transport, which reduces its exposure to regional disruptions.

One-Month Price Movement

Source: Zacks Investment Research

Comparing Industry Players

Devon Energy Corporation (DVN), another key player in the sector, has no direct exposure to the Middle East crisis and focuses on U.S. domestic basins. Over the past month, Devon’s stock has increased by 3.4%.

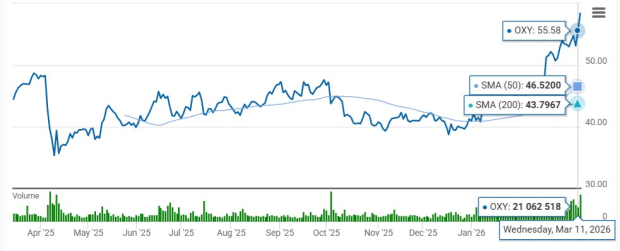

Currently, OXY’s share price is trading above both its 50-day and 200-day simple moving averages (SMA), a technical signal often interpreted as bullish. These SMAs are widely used by traders and analysts to identify potential support and resistance levels, and are considered early indicators of a stock’s trend direction.

OXY’s 50 and 200-Day Moving Averages

Source: Zacks Investment Research

Is OXY a Buy Based on Recent Gains?

Should investors consider adding OXY to their portfolios solely because of its recent price momentum? Let’s explore the underlying factors that could influence whether now is an opportune time to invest in OXY.

Key Factors Driving Occidental Petroleum’s Performance

- Rising Oil Prices: The ongoing Middle East conflict has pushed oil prices higher, which is expected to boost Occidental’s near-term margins due to its low-cost operations in the Permian Basin.

- Debt Reduction: The company has been actively selling non-core assets and using the proceeds to pay down long-term debt, having reduced its debt by $13.9 billion over the past 20 months and cutting annual interest expenses by $740 million.

- Cost Management: Occidental’s disciplined approach to cost control has resulted in $2 billion in annualized savings since 2023 across its U.S. onshore operations, with a target of achieving $500 million in sustainable cost reductions by 2026.

- Strategic Acquisitions: The acquisition of CrownRock L.P. is set to further strengthen Occidental’s footprint in the Permian Basin, providing a decade’s worth of high-return drilling opportunities under current market conditions.

Upward Revisions in Earnings Forecasts

Recent analyst consensus estimates for Occidental Petroleum’s earnings per share in 2026 and 2027 have been revised upward by 8.47% and 5.64%, respectively, over the last two months.

Source: Zacks Investment Research

In contrast, Devon Energy’s earnings projections for 2026 and 2027 have been revised downward by 18.87% and 15.27% during the same period.

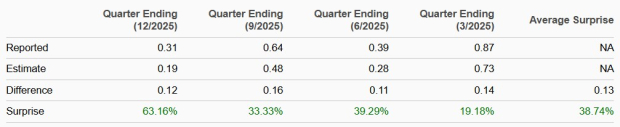

Consistent Earnings Surprises

Occidental Petroleum has exceeded earnings expectations in each of the last four reported quarters, with an average positive surprise of 38.74%.

Source: Zacks Investment Research

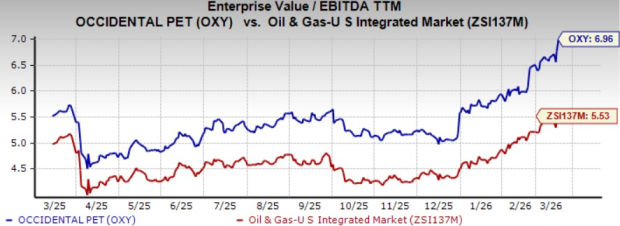

Valuation: OXY Shares Trade at a Premium

OXY’s shares are currently valued at a trailing 12-month EV/EBITDA multiple of 6.96, which is higher than the industry average of 5.53. This suggests the stock is trading at a premium relative to its peers.

Source: Zacks Investment Research

Meanwhile, ConocoPhillips (COP), another industry competitor with Middle East exposure, is trading at a 6.47 EV/EBITDA multiple, also above the industry average.

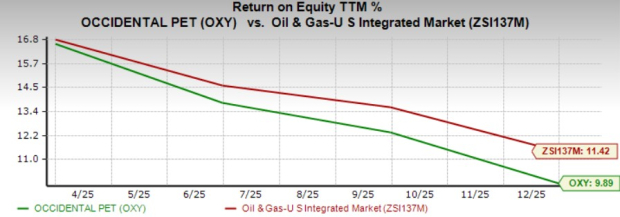

Return on Equity: OXY Lags Behind Industry Average

Return on equity (ROE) is a key metric for assessing a company’s profitability and efficiency in using shareholder capital. Over the past year, OXY’s ROE stood at 9.89%, which is below the industry average of 11.42%.

Source: Zacks Investment Research

By comparison, ConocoPhillips currently reports an ROE of 11.9%, outperforming the industry benchmark.

Summary and Outlook

Occidental Petroleum’s ongoing efforts to reduce debt, combined with its strong U.S. operations and the benefits of recent acquisitions, are expected to support its future growth. The company’s position as a low-cost producer should also help it capitalize on higher oil prices.

However, OXY continues to face stiff competition within the industry, and its return on equity remains below the sector average. Despite these challenges, the company’s solid presence in the Permian Basin and robust domestic operations make it a reasonable holding for investors, as reflected by its Zacks Rank #3 (Hold).

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Are Asian ETFs Facing Risks Due to the Combined Impact of War and Tariffs?

Is USA Rare Earth Stock the Key to Becoming a Millionaire?

UiPath and Unified Automation: Key Factors Behind ARR Expansion

AbraSilver CEO wins Kitco award as 350Moz Diablillos advances toward 2026 FID