3 Motives to Consider Selling ICFI and One Alternative Stock Worth Buying

ICF International: Recent Performance and Investor Considerations

ICF International shareholders have faced a challenging half-year, with the stock tumbling 29.5% to its current price of $70.32. This significant decline may leave investors questioning their next move regarding the company.

Should you consider adding ICF International to your holdings, or is it wiser to proceed with caution?

Reasons We Expect ICF International to Lag Behind

Despite the recent drop in share price, we remain wary of ICF International’s prospects. Below are three key factors that temper our enthusiasm for ICFI, along with an alternative stock we prefer.

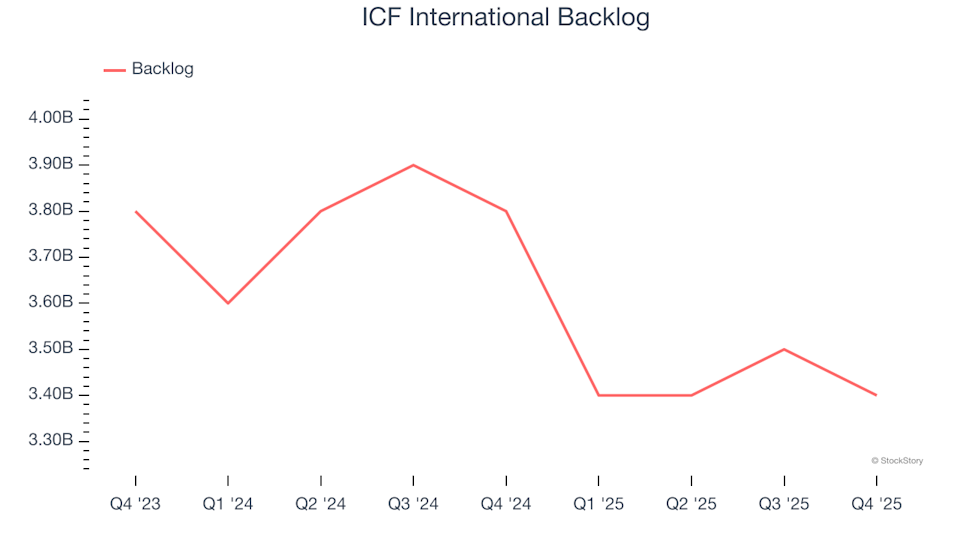

1. Shrinking Backlog Reflects Fewer New Orders

For companies in the Government & Technical Consulting sector, backlog figures offer insight into future revenue potential. This metric represents the total value of contracts yet to be fulfilled, serving as an indicator of upcoming business for ICF International.

In the most recent quarter, ICF International reported a backlog of $3.4 billion. Over the past two years, this figure has declined at an average annual rate of 7.4%. Such a trend suggests the company is struggling to secure new contracts, possibly due to heightened competition or a saturated market.

2. Modest Revenue Growth Outlook

Analyst forecasts provide a glimpse into a company’s growth trajectory. While these predictions are not always precise, accelerating revenue growth often leads to higher valuations, whereas sluggish growth can have the opposite effect.

Wall Street expects ICF International’s revenue to increase by just 2.2% over the next year. Although this suggests some improvement from new offerings, the growth rate remains below the industry average.

3. Earnings Growth Fails to Impress

While long-term earnings trends are important, we also examine recent earnings per share (EPS) growth for signs of change within the business.

ICF International’s EPS has grown at a modest 2% compound annual rate over the past two years. On a positive note, this outpaces the company’s 2.3% annual revenue decline, indicating that management has adjusted costs to cope with weaker demand.

Our Verdict

ICF International does not meet our criteria for a high-quality investment. Following its recent decline, the stock trades at a forward P/E of 10.2 (equivalent to $70.32 per share). This valuation suggests much optimism is already reflected in the price, and we believe more attractive opportunities exist. For example, consider one of our top-rated software stocks.

Stocks We Prefer Over ICF International

ALSO RECOMMENDED: Top 5 Momentum Stocks. The optimal moment to invest in a standout company is when the market begins to recognize its potential. These businesses not only exhibit strong fundamentals but are also experiencing a surge in momentum right now—making them especially compelling.

Discover which stocks our AI-driven platform is highlighting this week. Explore the latest Strong Momentum stocks for free.

Our selections have included well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Kadant, which delivered a 351% return over five years. Start your search for the next breakout stock with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Top 5 RWA Cryptos With Up to 80% Social Activity Surge in 24H: Are These Coins Set for a Big Week?

CZ goes after Etherscan for displaying address poisoning scams, offers up Trust Wallet solutions

OXY Jumps, Yet Negative Indicators Prevail

Ethereum Long-Term Price Outlook: Will Tokenization Boost Price?