Japanese Bond Market Crash, Yen Undergoing Latin Americanization

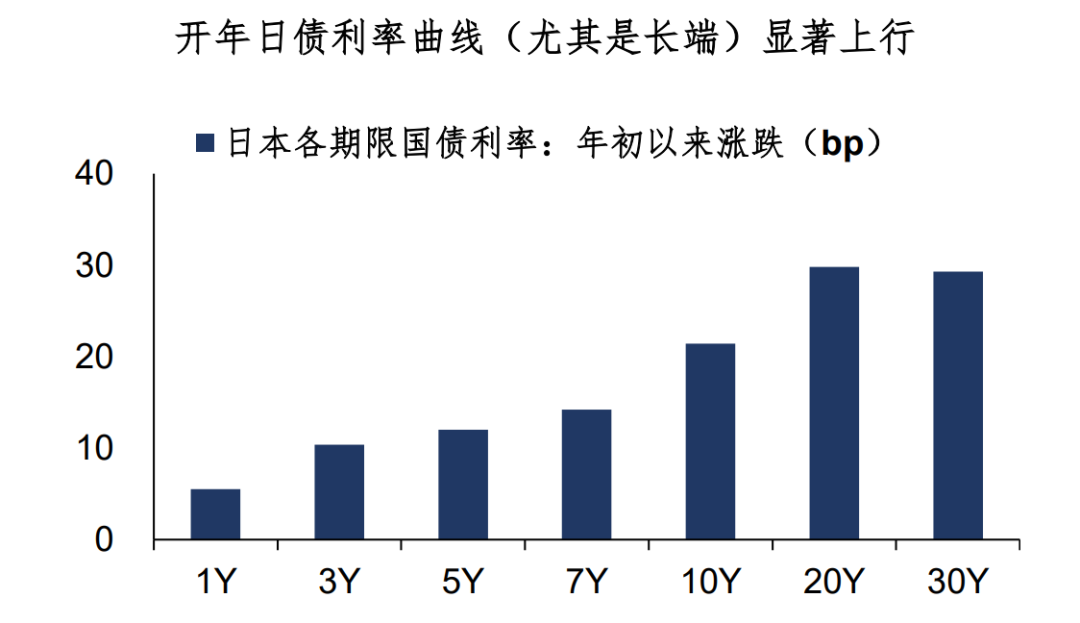

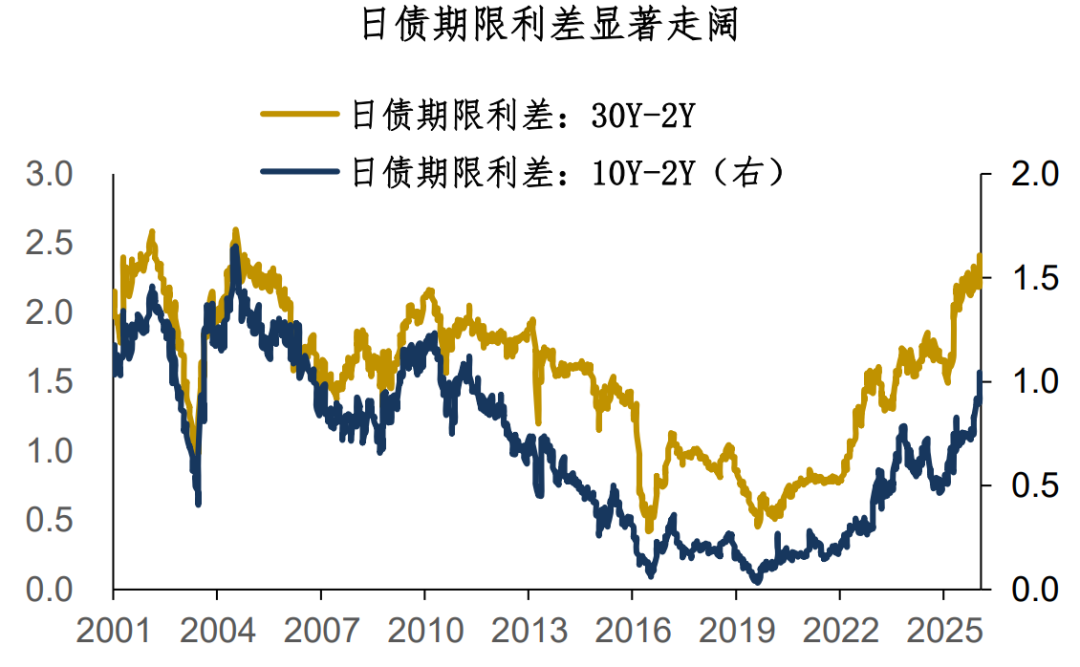

Describing the Japanese bond market in January 2026 as a "collapse" is no exaggeration—in less than a month, the 10Y Japanese bond yield rose by 20bp, and the 20-30Y bond yield rose by 30bp. The monthly increase in yields set a new high since 2004, the Japanese bond yield curve steepened significantly, and the long-term bond spread rose to 2010 levels.

Why did Japanese bond yields rise so rapidly, accompanied by yen depreciation (USDJPY 158)? In our previous sharing, "Talking about the Yen Exchange Rate at the Beginning of the Year", we discussed the logic behind the yen. The logic for Japanese bonds shares some similarities:

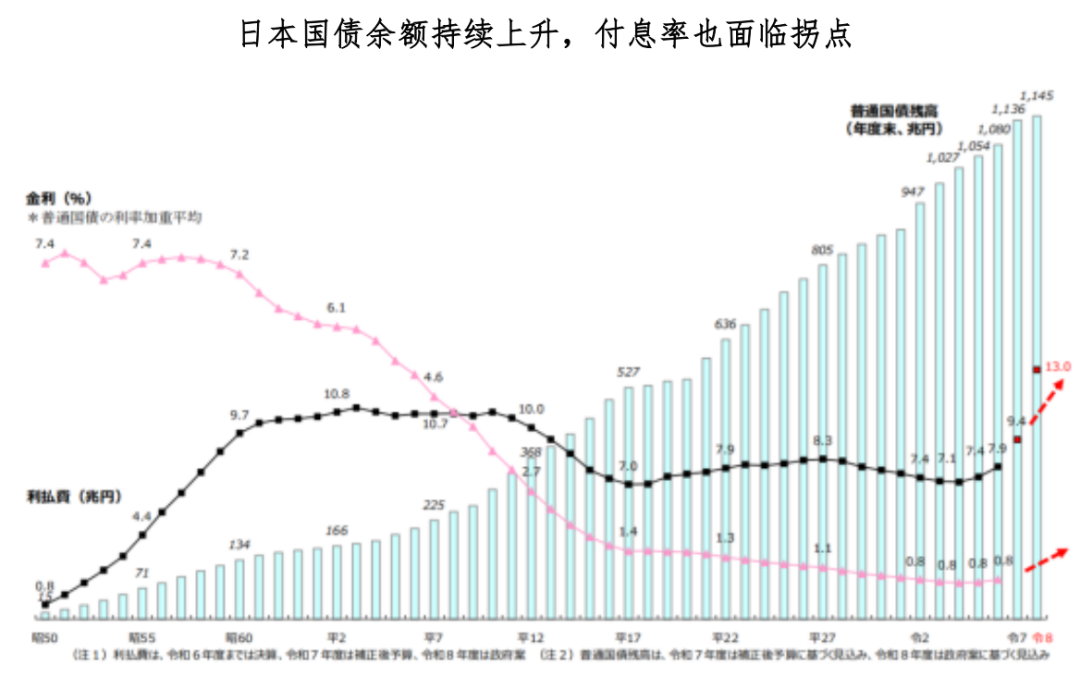

1. The fundamental reason for the Japanese bond collapse is fiscal stimulus during an interest rate hike cycle. This includes the previous 122 trillion yen draft budget for fiscal year 2026, with Japanese government bond balances expected to reach 1,145 trillion yen and interest expenses expected to balloon to 13 trillion yen. Recent announcements by the Kishida administration include dissolving the parliament for re-election and considering food consumption tax cuts (estimated at 5 trillion yen per year) and so on...

All these policies point to the so-called "Kishida trade," which is to go long Japanese equities + short Japanese bonds + short yen.

2. As for the Japanese bond market, a fragile supply-demand structure amplifies long bond volatility. Japanese banks and insurance institutions are already facing large unrealized losses in their securities accounts and, due to capital and regulatory constraints, find it difficult to substantially increase their holdings; overseas institutions, due to exchange rate issues (yen depreciation), are also unlikely to significantly increase their Japanese bond positions...

Dealing with such a collapsing market still requires policy support. On January 21, Japan’s second-largest bank, Sumitomo Mitsui Financial Group (SMFG), publicly announced plans to expand its Japanese bond holdings from the current 10.6 trillion yen to around 20 trillion yen. Such a "public pledge to increase holdings" inevitably raises speculation that there is a government endorsement behind it.

However, SMFG did not release a concrete plan for increasing its holdings. From its executives' statements, SMFG's actions may be conditional and gradual. In a recent Bloomberg interview, SMFG's Global Markets Head Arihiro Nagata estimated the fair value of the 10Y Japanese government bond yield to be between 2.5% and 3% (currently at 2.3%).

By the way, this Japanese executive not only predicted the 10Y Japanese bond yield—in the same interview, he also predicted the yen exchange rate: USDJPY could reach 180 in the coming years.

Soaring interest rates, currency depreciation, and the need for major financial institutions (possibly backed by the central bank) to step in to stabilize the market—it seems the yen is no longer behaving like an emerging market currency. To call it an emerging market currency may even be giving it too much credit; the yen is becoming Latin American.

To summarize today’s sharing:

1. The Japanese bond market in January 2026 can only be described as a "collapse." The 10Y Japanese bond yield rose by 20bp, the 20-30Y bond yield rose by 30bp, and the rate of increase is the fastest since 2004;

2. The fundamental reason for the Japanese bond collapse is fiscal stimulus during an interest rate hike cycle. "Kishida trade" catalyzed the steep rise in Japanese bond yields. In addition, the fragile supply-demand structure of the Japanese bond market amplified the volatility of long-term bonds. Recently, Japan’s second-largest bank, SMFG, publicly announced it would increase its holdings of Japanese government bonds, possibly with policy endorsement behind it;

3. Soaring interest rates, currency depreciation, and the need for major financial institutions (possibly backed by the central bank) to step in to stabilize the market—it seems the yen is no longer behaving like an emerging market currency. To call it an emerging market currency may even be giving it too much credit; the yen is becoming Latin American.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Gap’s Margin Guidance Tied to Tariffs Sets Up Opportunity for Tactical Mispricing

Top Analyst: Cardano (ADA) is Building Foundation for Major Rally