The Costliest Inquiry Investors Make

Understanding Market Cycles and Investor Decisions

Having witnessed numerous stock market cycles over the years, I've noticed a familiar scenario for investors: you check your portfolio, see a drop, and immediately wonder whether to buy more of the declining stock or sell it. While these choices might seem logical at first glance, they're often made in response to emotional triggers rather than sound judgment. By the time this dilemma arises, discipline has usually slipped, and the stock’s movement is dictating your actions. It’s important to recognize that averaging down or selling a losing position are not investment strategies in themselves—they are simply tools. Their effectiveness depends entirely on the context in which they’re used. When applied incorrectly, averaging down can amplify mistakes and lead to substantial losses. Used wisely, however, it can quietly enhance returns. The key difference isn’t conviction, but rather the underlying structure of the investment—a distinction where many investors lose capital.

Common Pitfalls of Averaging Down

On paper, increasing your stake in a falling stock seems logical: if the business remains solid and the price is lower, buying more should improve your returns. In reality, this approach fails more often than it succeeds. Stocks rarely decline without cause. Sometimes the reason is misunderstood, but more often it’s rooted in structural issues. A frequent error is mistaking a low price for genuine value. Companies in decline often appear cheap based on past earnings, just before those earnings vanish. Management may downplay problems as temporary, while their interests drift from those of shareholders. Risks quietly accumulate on the balance sheet, and capital is misallocated to preserve the status quo rather than invest in future growth. In such cases, buying more isn’t patience—it’s increasing your exposure to a deteriorating situation.

Anchoring to your original purchase price only makes matters worse. Investors often treat their entry price as a benchmark, but the market is indifferent. What truly matters is the company’s future earnings and how those will be realized.

For years, large conglomerates have traded at discounts because their complexity obscures accountability. Businesses in terminal decline may look attractive until their cash flow dries up. For example, PayPal (PYPL) fits this pattern. Cyclical stocks that suffer permanent damage rarely recover, as the cycle never repeats in the same way. Ultimately, value is created by structure, not by price alone.

Related Market Insights

Knowing When to Sell

Many investors view selling a losing stock as an admission of failure, but it shouldn’t be. Exiting a position isn’t about avoiding discomfort—it’s about safeguarding your capital and reallocating it to better opportunities. Sometimes, price fluctuations are just noise; other times, they indicate a fundamental shift. The real challenge is telling the difference.

You should consider selling when your original investment thesis no longer holds up—not because the price has changed, but because the underlying rationale has broken down. This could be due to poor capital allocation by management, a weakening balance sheet, the disappearance of a key catalyst, or a shift in company structure that no longer favors shareholders. Holding on through these changes isn’t conviction—it’s a mistake. The market rewards those who position themselves correctly, not those who are loyal to a stock. Selling provides flexibility, frees up resources, and allows you to pursue situations where the odds are in your favor.

The Overlooked Factor: Structure

Debates about whether to average down or cut losses often ignore the most crucial element: structure. Structural alpha isn’t about optimism—it’s about capitalizing on forced changes. Sometimes, prices move not because of deteriorating fundamentals, but due to mechanical reasons: index funds are required to sell, institutions must reduce exposure, or analysts drop coverage. Liquidity can dry up simply because the pool of buyers shrinks, not because the asset has lost value. These scenarios create mispriced assets, not narrative-driven stocks. Recognizing this distinction transforms the entire discussion around averaging down versus selling.

How Spinoffs Create Opportunity

Spinoffs are a prime example of structural alpha, an area I’ve studied for over two decades. Typically, spinoffs are sold off indiscriminately at first—index funds dump them, large investors reduce their holdings, and many shareholders never wanted the new asset. This initial selling pressure can make the price action look weak, which can scare off investors who focus solely on charts.

What sets spinoffs apart is the transformation that occurs beneath the surface. Management teams become aligned with the right incentives, strategic focus sharpens, capital allocation improves, and balance sheets become more transparent. Accountability increases, and in many cases, the company’s fundamentals are getting stronger even as the stock price falls. This is the real advantage of spinoffs.

Recent examples include the breakup of General Electric (GE), where value was unlocked not because sentiment improved, but because the company’s structure changed. Western Digital (WDC) and SanDisk (SNDK) experienced similar patterns, with forced selling creating opportunities before the broader market caught on. Illumina’s (ILMN) separation from Grail (GRAL) led to years of market dislocation unrelated to the core business. Smaller spinoffs often need time for selling pressure to subside and for new investors to step in. In these cases, averaging down can be justified—not because the price is lower, but because the investment thesis is strengthening as temporary noise creates opportunity. Here, patience works in your favor as you wait for structural improvements to be recognized.

Recognizing the Limits of Structure

While structure can be a powerful driver of value, it’s not a guarantee. Spinoffs can fail if they’re saddled with excessive debt, lack a competitive advantage, have untrustworthy management, or suffer from poor strategy and execution. Simply separating a business doesn’t create value—it only opens the door for value to be realized. Understanding this difference is what distinguishes true investors from those who merely collect stock symbols.

A Practical Decision-Making Framework

Deciding whether to buy more, hold, or sell doesn’t have to be complicated. Ask yourself these three questions:

- Has the structure improved?

- Is the investment thesis stronger or weaker?

- Is there a clear path to realizing value?

If you can answer “yes” to all three, adding to your position may be sensible. If not, selling and reallocating your capital is likely the wiser move. The goal isn’t to be bold, but to remain disciplined.

Focus on the Right Opportunities

The real advantage in investing doesn’t come from knowing when to average down or when to exit—it comes from choosing environments where these tools are effective. Spinoffs, corporate breakups, forced selling, and structural dislocations are areas where a margin of safety exists and patience is rewarded. The most successful investors don’t argue with price—they seek out the best arenas for their capital.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Pound Sterling weakens to near 1.3300 as geopolitical risks bolster US Dollar

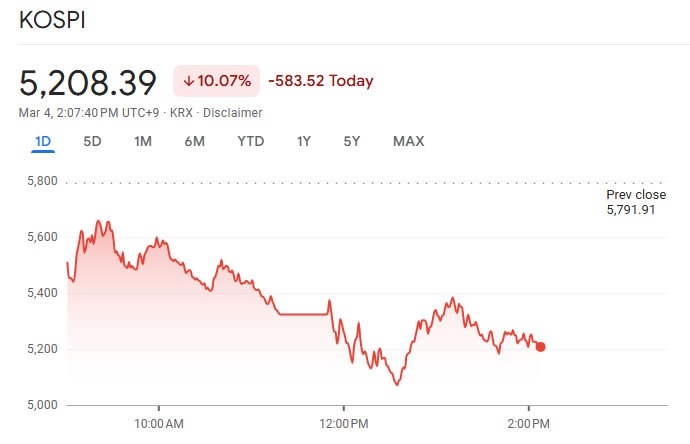

Korea halts trading as key indexes drop 10% on Middle East crisis

DigitalOcean's Agentic Inference Cloud: Creating the Infrastructure for Deploying AI in Production