Central banks' gold buying spree contradicted by data! Is there another driver behind gold's rally?

The Financial Times published an article on Tuesday exploring the gold-buying behavior of central banks around the world. As previously noted by the newspaper’s columnist Robert Armstrong, “Some believe that global central banks are shifting their foreign exchange reserves from the US dollar to gold, a move that is a more effective gauge of ‘currency debasement’ than the bond market.”

Indeed, many people hold this view. Bridgewater Associates founder Ray Dalio is among them, and he stated last week at the World Economic Forum:

“There are currently serious imbalances in the global economy, and there is a high degree of interdependence between countries. The United States needs substantial capital inflows, while other countries are worried that their dollar assets could be frozen. This inherent trend is playing a key role, and is now clearly manifesting as central banks shifting to gold allocations. We are seeing central banks increase their gold reserves, which is the traditional approach in times of major conflict.

This is the beginning of the end for the monetary system as we know it. It’s not just the US dollar that’s affected; all fiat currencies—including the UK, the Eurozone, and Japan—face similar debt issues and exist within the same international framework. This is also why central banks are turning to gold.”

Perhaps Dalio is correct, but Bryce Elder, editor of FT Alphaville—the daily news commentary service founded by the Financial Times—points out that there is currently a lack of empirical evidence supporting this narrative.

Fund flows into gold ETFs allow retail investors’ gold demand to be tracked almost in real time, but central banks’ gold demand is much harder to quantify. Central banks report their reserves to the IMF annually under Article IV consultation as part of their annual health assessment, and only need to disclose more details when borrowing or applying for IMF emergency financing. This leads to a delay of up to six months in the release of relevant data.

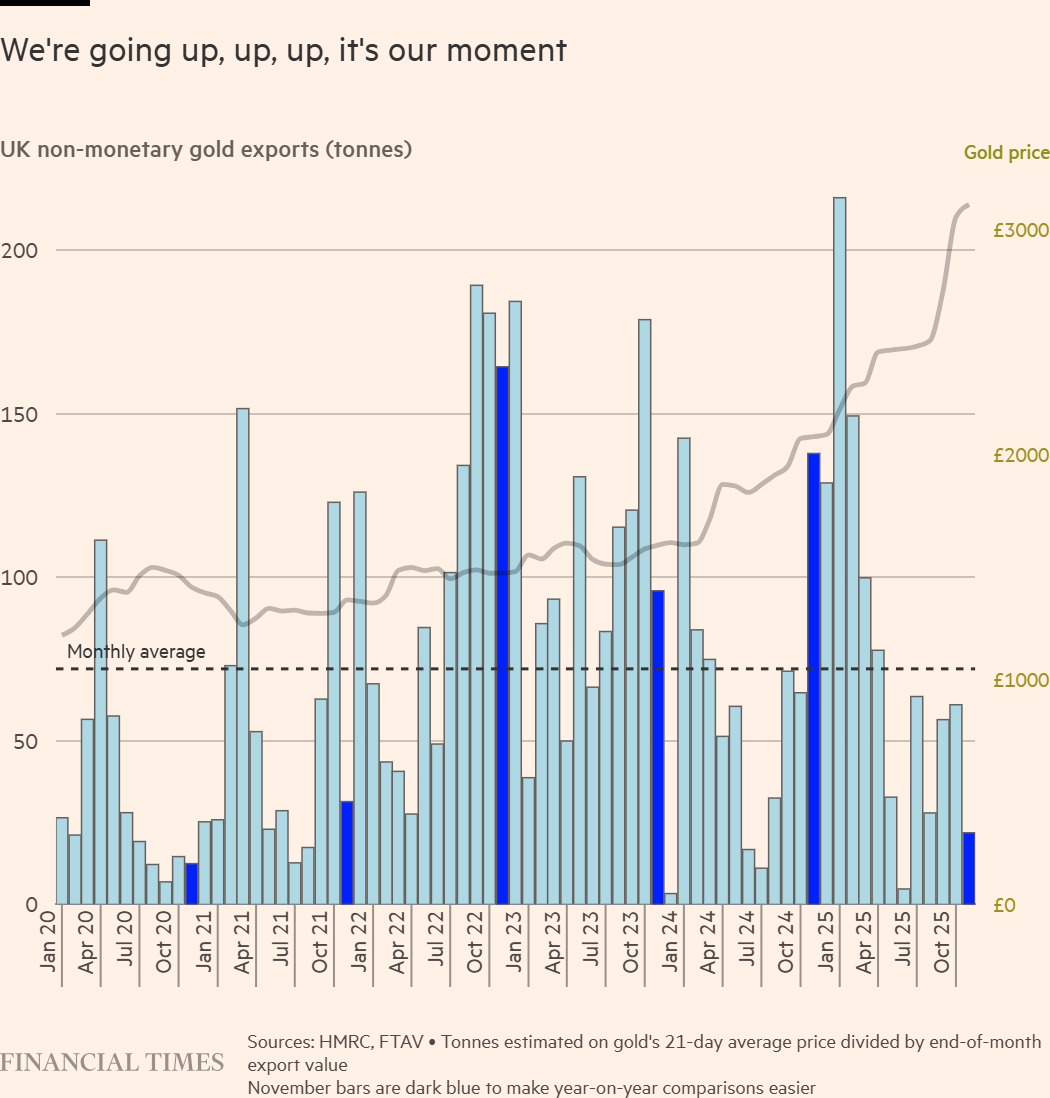

To get a quicker sense of central bank gold purchases, analysts look at overseas trade data from the UK’s HM Revenue & Customs. London is the world’s largest gold trading hub, so the UK’s monthly non-monetary gold export data serves as an important indicator of central bank gold buying activity.

Overall, the UK’s gold export data aligns closely with subsequently released figures on actual central bank gold purchases. As can be seen from the chart below, after Russia launched its special military operation against Ukraine in 2022, central bank gold buying nearly doubled, with annual purchases surpassing 1,000 tons.

More notably, after adjusting for price factors, the scale of UK gold exports has shown a steady downward trend for a full year.

UK Non-Monetary Gold Exports

UK Non-Monetary Gold Exports Of course, such monthly data can be highly volatile and should be interpreted with caution. Nevertheless, the UK’s gold exports in November last year plunged by more than 80% year-on-year by weight, casting doubt on the argument that “central banks are still ramping up their gold allocations.”

It’s not surprising that China has become the largest gold buyer. As of December 2025, China’s gold reserves have surpassed 2,300 tons, accounting for 8.5% of total foreign exchange reserves at current prices, and the People’s Bank of China has increased its gold holdings for 14 consecutive months.

However, based on UK export data, the People’s Bank of China bought less than 10 tons of gold in November last year, well below its recent and long-term average purchase levels.

In a report last week, Morgan Stanley analysts pointed out that it is reasonable and somewhat predictable for central banks to slow gold purchases as the value of their gold assets appreciates.

For a long time, it has been widely assumed that central banks set a target ratio of gold reserves to foreign exchange reserves. As gold prices rise, central bank demand for gold naturally declines over time. For example, in August this year, Poland’s central bank announced plans to increase the proportion of gold reserves from 21% to 30%. At current gold prices, this target has essentially been achieved.

However, Poland’s central bank last week approved a plan to increase gold holdings by 150 tons, which would bring its total reserves to 700 tons. This shift means Poland’s central bank moved from a “ratio target” to an “absolute tonnage target” for gold reserves, highlighting its intention to continue increasing gold holdings even as prices remain high. If other central banks follow suit, global central bank gold buying could continue to grow in the coming years, even if gold prices remain elevated.

Yet, reality appears otherwise. Poland imported only 0.00002 tons of gold from the UK last November, a figure that clearly fails to support the notion that it is indifferent to gold price movements.

For cross-verification, Michael Haigh and his team at Societe Generale reference monthly vault inventory data released by the London Bullion Market Association shortly after each month-end, which closely matches UK HMRC export data.

The data show that the London Bullion Market Association’s vault inventories increased by 199 tons in December last year.

Michael Haigh and his team wrote in their report:

Historically, when the London Bullion Market Association’s vault inventories rise sharply, gold export volumes tend to be very low—sometimes only 4 tons for an entire month. From a seasonal perspective, based on average data since 2022, December’s gold exports would normally be around 100 tons. In fact, of the 10 months with the highest vault inflows, gold export activity—as an indicator of central bank buying—remained subdued, with an average monthly export volume of just 12.2 tons. Conversely, when vault inventories experience net outflows, gold export volumes rise, averaging 152 tons per month.

Taking all the data together, Bryce Elder points out that the process of central banks rebalancing foreign exchange reserves—that is, shifting from the US dollar to gold—may be nearing its end. As Rob Armstrong said, momentum chasing seems the most convincing explanation for gold’s recent price strength.

Whether this frenzy for gold investment is rational is an entirely different question. And as with any form of extreme dogmatism, Bryce Elder prefers to stay out of the debate.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Breaking: Iran says no more attacks against neighbouring countries “unless they attack first”

Pundit Describes How $10,000 In XRP Could Become $1,000,000

Nvidia Releases Financial Results. Investors on Wall Street Respond, "Is That All?"