Illumina (NASDAQ:ILMN) Announces Strong Fourth Quarter Results for Fiscal Year 2025

Illumina Surpasses Expectations in Q4 2025

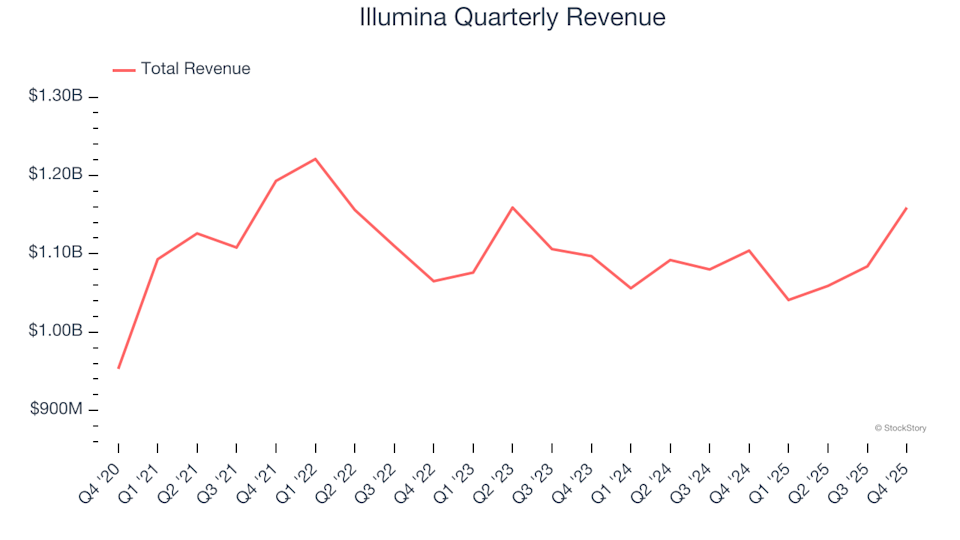

Illumina (NASDAQ: ILMN), a leader in genomics, exceeded analyst forecasts for revenue in the fourth quarter of 2025, posting $1.16 billion in sales—a 5% increase compared to the previous year. The company’s projected full-year revenue of $4.55 billion (at the midpoint) was 3.1% higher than consensus estimates. Adjusted earnings per share reached $1.35, outpacing analyst expectations by 8.3%.

Should You Consider Investing in Illumina?

Curious if now is the right moment to invest in Illumina?

Highlights from Illumina’s Q4 2025 Performance

- Revenue: $1.16 billion, surpassing the $1.12 billion analyst estimate (5% year-over-year growth, 3.2% above expectations)

- Adjusted EPS: $1.35, exceeding the $1.25 consensus (8.3% beat)

- Adjusted Operating Income: $275 million, topping the $253 million forecast (23.7% margin, 8.7% above estimates)

- 2026 Adjusted EPS Guidance: $5.13 at the midpoint, 1.1% higher than analyst projections

- Operating Margin: 17.4%, up from 15.9% in the prior year’s quarter

- Free Cash Flow Margin: 23%, down from 30.3% a year ago

- Organic Revenue: Increased 5% year over year

- Market Cap: $20.5 billion

“Our team delivered a strong close to 2025, returning to growth by executing our strategy with discipline,” commented Jacob Thaysen, Illumina’s CEO.

About Illumina

Illumina (NASDAQ: ILMN) is at the forefront of genomic technology, providing advanced DNA sequencing and microarray solutions that empower researchers and clinicians to study genetic variation and function with unprecedented speed and affordability.

Revenue Trends and Growth

Consistent revenue growth is a hallmark of a high-quality business. While Illumina’s sales have increased at a compound annual rate of 6% over the past five years, this pace falls short of the healthcare sector’s benchmark and is considered lackluster for long-term evaluation.

Although long-term growth is crucial, especially in healthcare, focusing solely on five-year trends may overlook recent innovations or shifts in demand. Illumina’s revenue has declined by an average of 1.1% per year over the last two years, indicating that earlier gains have not been sustained.

To provide a clearer picture, Illumina also reports organic revenue, which excludes the effects of acquisitions and currency changes. Over the past two years, organic revenue has also declined by an average of 1.1% annually, suggesting that the core business—not external factors—has driven recent results.

Recent and Projected Revenue Performance

In the latest quarter, Illumina achieved a 5% year-over-year increase in revenue, beating Wall Street’s expectations by 3.2%.

Looking forward, analysts anticipate a 1.7% revenue increase over the next year. While this reflects optimism about new offerings, it remains below the industry average.

For investors seeking the next big platform winner—much like Microsoft and Apple in the past—enterprise software companies leveraging generative AI are emerging as strong contenders.

Profitability: Adjusted Operating Margin

The adjusted operating margin is a key indicator of profitability, reflecting earnings after core expenses like R&D and marketing, while excluding one-off costs for a clearer view of ongoing performance.

Over the past five years, Illumina has maintained an average adjusted operating margin of 23.2%, positioning it among the more profitable companies in healthcare. However, this margin has declined by 4.7 percentage points over five years, though it has improved by 3.2 points in the last two. Investors will be watching for further gains in efficiency.

This quarter, Illumina’s adjusted operating margin rose to 23.7%, a 4-point improvement from the previous year, signaling increased operational efficiency.

Earnings Per Share (EPS) Analysis

While revenue growth highlights expansion, the trajectory of earnings per share (EPS) reveals how profitable that growth truly is. Illumina’s EPS has grown at a modest 1.5% compound annual rate over the last five years, trailing its revenue growth rate. Despite this, the company’s adjusted operating margin has improved, indicating that factors such as interest and taxes have weighed on net earnings.

A closer look shows that, although operating margins have expanded this quarter, they have dropped by 4.7 percentage points over five years. Additionally, Illumina’s share count has increased by 4.8%, leading to some shareholder dilution and less efficient use of operating expenses.

For Q4, adjusted EPS reached $1.35, up from $0.86 a year earlier and 9.7% above analyst expectations. Wall Street projects full-year EPS to rise 4.5% to $4.85 over the next twelve months.

Summary and Investor Considerations

Illumina’s upbeat full-year revenue outlook and strong organic revenue performance stood out this quarter. Despite these positives, the stock dipped 1.4% to $131.70 following the results, suggesting investors were hoping for even more robust growth.

Is Illumina a compelling investment at its current valuation? Prospective investors should weigh the company’s valuation, business fundamentals, and latest earnings before making a decision.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Quantum Leap Energy: Selecting the Designer for a Nuclear Fuel S-Curve

Burlington (NYSE:BURL) Surpasses Q4 CY2025 Forecasts, Shares Surge

Saudi Arabia Begins Redirecting Oil Shipments to the Red Sea Amid Growing Hormuz Disruptions

Olaplex (NASDAQ:OLPX) Reports Q4 CY2025 Sales Surpassing Expectations, Yet Shares Decline