Sypris Rises 47% Over Half a Year: Is Now the Time to Invest?

Sypris Solutions, Inc.: Recent Stock Performance and Industry Comparison

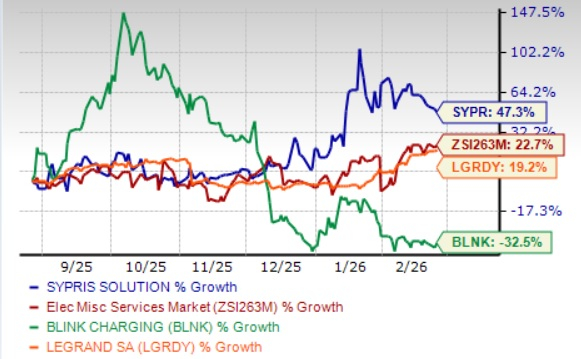

Over the past half-year, shares of Sypris Solutions, Inc. (SYPR) have surged by 47.3%, significantly outpacing the industry average growth of 22.7%. This impressive performance has surpassed peers such as Blink Charging Co. (BLNK) and Legrand SA (LGRDY), with LGRDY rising 19.2% and BLNK dropping 32.5% during the same period. The company’s momentum is fueled by robust demand in aerospace and defense, a growing backlog linked to the Artemis program, new reshoring contracts, a broad customer base, and enhanced liquidity from operational improvements.

Image Source: Zacks Investment Research

Inside Sypris Solutions’ Business Model

Established in 1997, Sypris Solutions operates as a diversified manufacturer, serving sectors such as commercial vehicles, energy pipelines, aerospace, and defense through its two main divisions: Sypris Technologies and Sypris Electronics. The company specializes in producing forged, machined, welded, and heat-treated components, high-pressure pipeline products, and reliable electronic assemblies, often under long-term, exclusive contracts. Its clientele includes leading original equipment manufacturers and top aerospace and defense contractors. Sypris prioritizes lean manufacturing, advanced quality systems, engineering expertise, and ongoing innovation to boost efficiency, lower costs, and ensure product reliability. With operations in both the United States and Mexico, the company is committed to strategic partnerships and expanding its value-added services.

Growth Drivers for Sypris Solutions

Sypris Solutions is well-positioned to capitalize on increasing long-term demand in the aerospace and defense sectors. As of September 28, 2025, Sypris Electronics reported $76.9 million in outstanding performance obligations, most of which are scheduled for delivery in 2026 and 2027. This backlog provides strong visibility for production and cash flow planning. In January 2026, the company secured an expanded follow-on contract related to NASA’s Artemis program, extending its backlog through 2027 and solidifying its presence in high-reliability space electronics. Continued U.S. defense spending and deep-space initiatives remain important growth catalysts.

Additionally, Sypris Technologies is benefiting from reshoring trends and exclusive contract opportunities. In January 2026, the company entered a long-term, sole-source agreement with a global truck manufacturer to supply critical AMT components for heavy-duty trucks in North America, with production expected to start in 2027. This partnership supports the customer’s reshoring efforts and positions Sypris as a key manufacturing and logistics partner.

The company’s diverse exposure across commercial vehicles, energy infrastructure, aerospace, defense, and space systems also provides resilience. While the Class 8 truck market remains soft, Sypris has expanded into automotive, sport-utility, and off-highway programs to reduce volatility. In the energy sector, ongoing geopolitical factors and infrastructure investments are driving demand for high-pressure pipeline components. This diversification helps buffer the company from downturns in any single market and offers flexibility as different industrial cycles recover at different times.

Operational improvements and financial actions are also contributing to Sypris’ progress. In 2025, the company completed a sale-leaseback transaction, generating a $2.5 million gain and approximately $2.9 million in net proceeds, which enhanced liquidity and financial flexibility. Inventory reductions further improved cash flow during the first nine months of 2025.

Ongoing Challenges for Sypris Solutions

Despite its strengths, Sypris Solutions faces several challenges, particularly in its Sypris Technologies segment. The company’s net revenues fell by 16% during the first nine months of 2025, mainly due to weaker demand in the North American Class 8 commercial vehicle market. Management also points to ongoing inflationary pressures on raw materials, logistics, labor, and utilities, as well as tariff uncertainties and supply chain disruptions expected to persist through 2025.

Liquidity and leverage remain concerns. The company reported a net loss of $2.4 million and negative operating cash flow of $4.6 million for the first nine months of 2025. Additionally, supply chain delays and program timing issues in Sypris Electronics have increased working capital volatility and reduced operational efficiency.

Valuation Overview

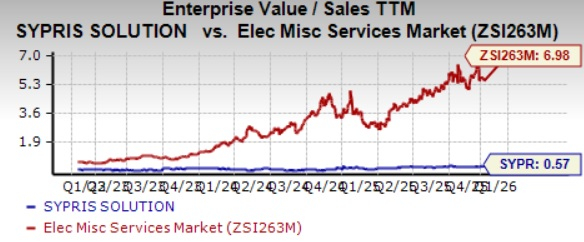

Sypris Solutions is currently trading at a discount compared to its industry peers. The company’s trailing 12-month EV/sales ratio stands at 0.57X, well below the industry average of 6.98X. While this is slightly higher than Blink’s 0.52X, it remains much lower than Legrand’s 4.93X, highlighting Sypris’ attractive valuation.

Image Source: Zacks Investment Research

Summary and Investment Perspective

Although Sypris Solutions continues to navigate cyclical weakness in the North American Class 8 truck market, inflationary pressures, tariff uncertainties, and recent liquidity challenges, the company’s strong aerospace and defense backlog—bolstered by NASA Artemis-related contracts extending into 2027—provides a solid foundation for long-term revenue and cash flow stability.

Given its solid fundamentals and attractive valuation, Sypris Solutions presents a compelling opportunity for investors seeking to add value stocks to their portfolios.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

China’s yuan rebounds after central bank raises midpoint to highest level in half a year

Unusual Options Activity: AMD, CRWV and Others Attract Market Bets, AMD V/OI Ratio Reaches 138.9

Seadrill's 2026 Outlook: Maintaining Stability Amid a Level Market

Adyen at Morgan Stanley: Assessing the Platform Moat and AI-Driven Valuation

Trending news

MoreNegotiation breakdown details revealed, US envoy: Iran rejected the "ten years of zero enriched uranium" proposal! Iran releases footage of attack on US military base, US Secretary of State: The next stage of US strikes against Iran will be even stronger

China’s yuan rebounds after central bank raises midpoint to highest level in half a year