DXP (NASDAQ:DXPE) Delivers Impressive Q4 CY2025

Industrial distributor DXP Enterprises (NASDAQ:DXPE)

Is now the time to buy DXP?

DXP (DXPE) Q4 CY2025 Highlights:

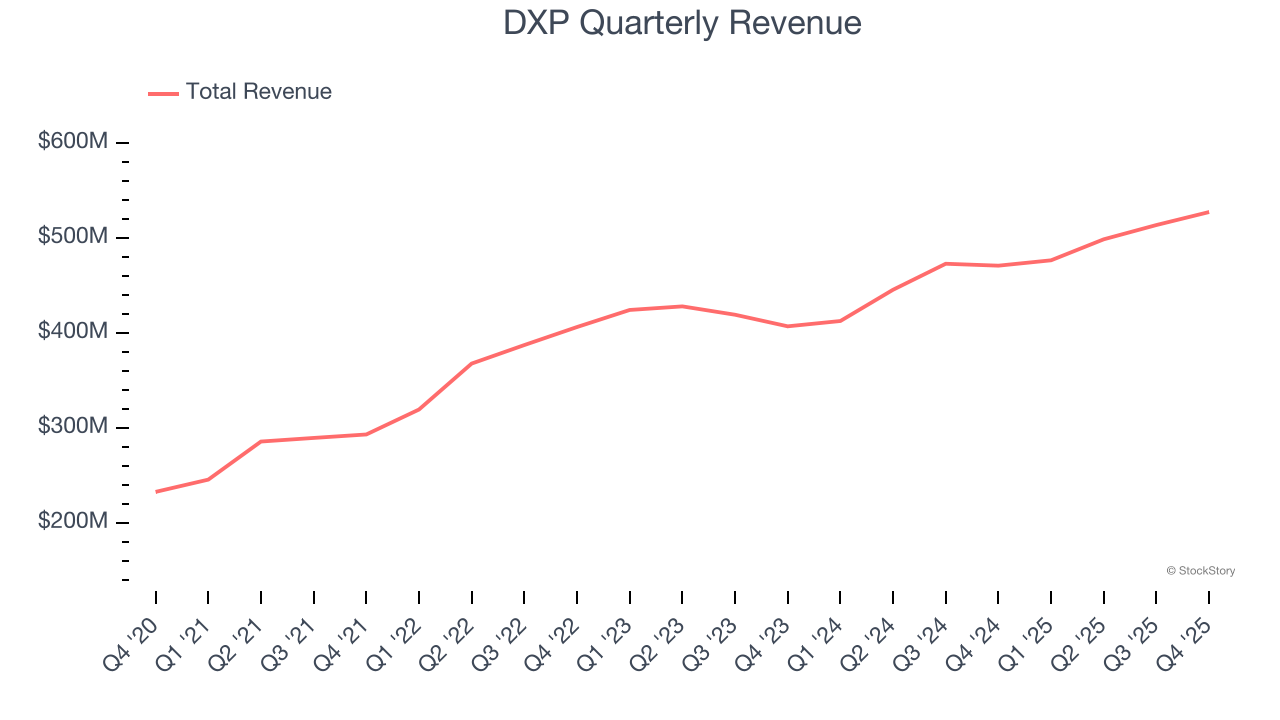

- Revenue: $527.4 million vs analyst estimates of $499 million (12% year-on-year growth, 5.7% beat)

- Adjusted EPS: $1.39 vs analyst estimates of $1.30 (6.9% beat)

- Adjusted EBITDA: $58.97 million vs analyst estimates of $55 million (11.2% margin, 7.2% beat)

- Operating Margin: 8.8%, in line with the same quarter last year

- Free Cash Flow Margin: 6.5%, up from 4.8% in the same quarter last year

- Market Capitalization: $2.50 billion

Company Overview

Founded during the emergence of Big Oil in Texas, DXP (NASDAQ:DXPE) provides pumps, valves, and other industrial components.

Revenue Growth

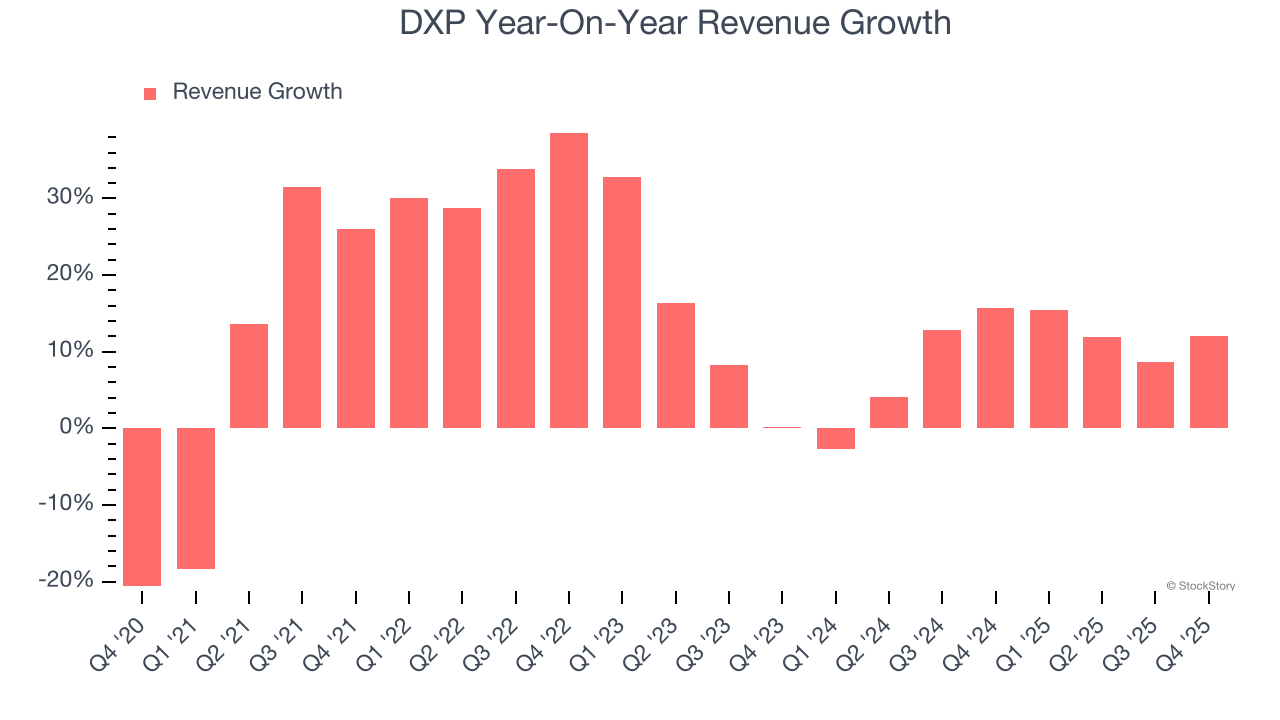

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, DXP’s 14.9% annualized revenue growth over the last five years was exceptional. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. DXP’s annualized revenue growth of 9.6% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, DXP reported year-on-year revenue growth of 12%, and its $527.4 million of revenue exceeded Wall Street’s estimates by 5.7%.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

DXP was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.4% was weak for an industrials business.

On the plus side, DXP’s operating margin rose by 5.2 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, DXP generated an operating margin profit margin of 8.8%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

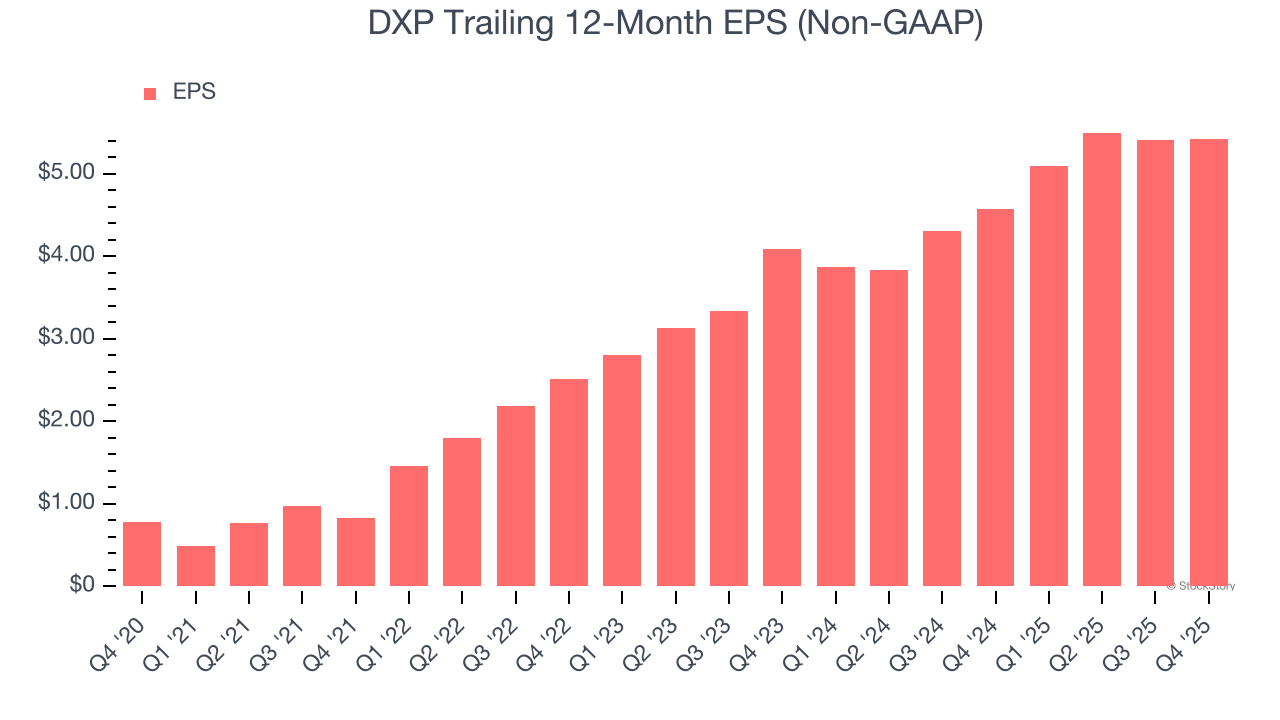

DXP’s EPS grew at an astounding 47.4% compounded annual growth rate over the last five years, higher than its 14.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

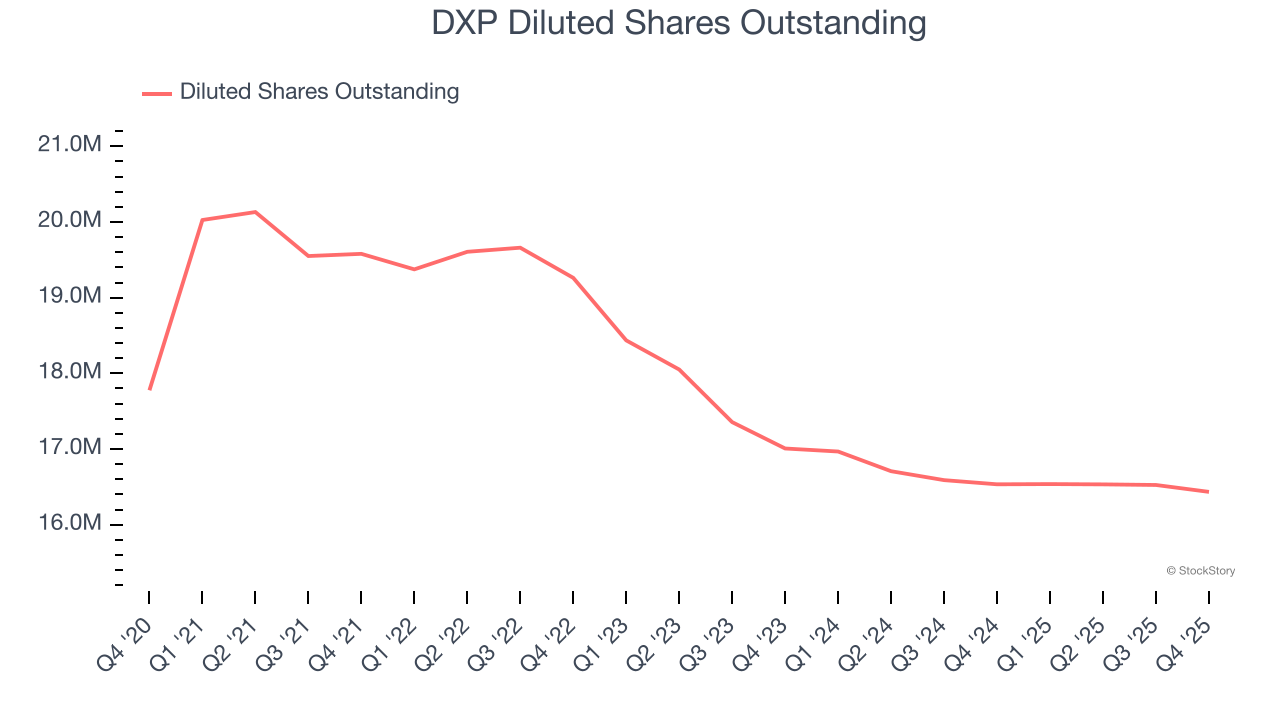

We can take a deeper look into DXP’s earnings to better understand the drivers of its performance. As we mentioned earlier, DXP’s operating margin was flat this quarter but expanded by 5.2 percentage points over the last five years. On top of that, its share count shrank by 7.5%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For DXP, its two-year annual EPS growth of 15.2% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, DXP reported adjusted EPS of $1.39, up from $1.38 in the same quarter last year. This print beat analysts’ estimates by 6.9%. Over the next 12 months, Wall Street expects DXP’s full-year EPS of $5.42 to grow 18.6%.

Key Takeaways from DXP’s Q4 Results

We were impressed by how significantly DXP blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $155.36 immediately after reporting.

Indeed, DXP had a rock-solid quarterly earnings result, but is this stock a good investment here? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Futu Holdings Surges 5.38% Despite 31.48% Volume Plunge to 320M Ranked 416th in Market Activity

Lennox Plunges 3.29% as Volume Surges 151% to Rank 423rd Amid Profit-Driven Strategy Doubts

Private Investment in New Capital and Projected Spending, Australia, December 2025