Futu Holdings Surges 5.38% Despite 31.48% Volume Plunge to 320M Ranked 416th in Market Activity

Market Snapshot

Futu Holdings (FUTU) rose 5.38% on February 25, 2026, despite a 31.48% decline in trading volume to $0.32 billion, ranking 416th in market activity. The stock closed at $168.47, slightly below its 52-week high of $202.53, reflecting mixed investor sentiment. While the price surge suggests short-term optimism, the sharp drop in volume indicates reduced liquidity or participation compared to prior sessions.

Key Drivers

The stock’s 5.38% gain follows a strong earnings report for Q3 2025, where the company exceeded expectations with an EPS of 22.8 HKD (26.67% above forecast) and revenue of $6.4 billion (46.79% above forecast). Net income surged 143% year-over-year to $3.2 billion, driven by a 6.0 percentage-point improvement in gross margin to 87.8%. Management highlighted strategic expansion in Hong Kong, Singapore, Malaysia, and the U.S., reinforcing confidence in its global footprint.

However, the post-earnings price trajectory was muted, with a pre-market decline of 0.06% observed. This may reflect investor caution despite strong fundamentals. The company’s emphasis on crypto trading as a growth engine and openness to M&A to accelerate client base expansion likely contributed to the rally. Executives also noted the firm’s sensitivity to interest rate changes, estimating a $7 million monthly pre-tax profit impact per 25 basis point shift in Federal Reserve rates—a factor that could weigh on future performance if monetary policy tightens.

Institutional activity further contextualizes the stock’s movement. While 192 institutional investors added shares in Q4 2025, 233 reduced their stakes, with major exits including UBS AM and POINT72 Hong Kong. This divergence in institutional sentiment suggests a polarized view of Futu’s near-term prospects. Analysts, however, remain bullish: Citigroup and Barclays issued “Buy” or “Overweight” ratings, with price targets ranging from $201 to $236, reflecting confidence in the company’s digital brokerage model and long-term growth potential.

The upcoming Q4 2025 earnings report on March 12, 2026, will be critical. The company has scheduled a conference call for the same day at 7:30 AM U.S. Eastern Time, though participants must pre-register—a procedural detail that may limit immediate transparency. Investors will likely scrutinize guidance for 2026, as the current data lacks explicit forecasts. Meanwhile, the firm’s integration of social media tools into its platforms and its focus on user engagement underscore its innovative approach in the competitive online brokerage space.

Despite these positives, challenges persist. The requirement for pre-registration for the earnings call and the absence of specific Q4 2025 metrics in the recent announcement could dampen investor enthusiasm ahead of the report. Additionally, the company’s reliance on interest rate dynamics and the mixed institutional ownership signal potential volatility. As the market awaits March’s results, the stock’s performance will hinge on whether FutuFUTU+5.38% can sustain its margin expansion and execution against its aggressive growth targets.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

BTC volatility climbs near one-year peak

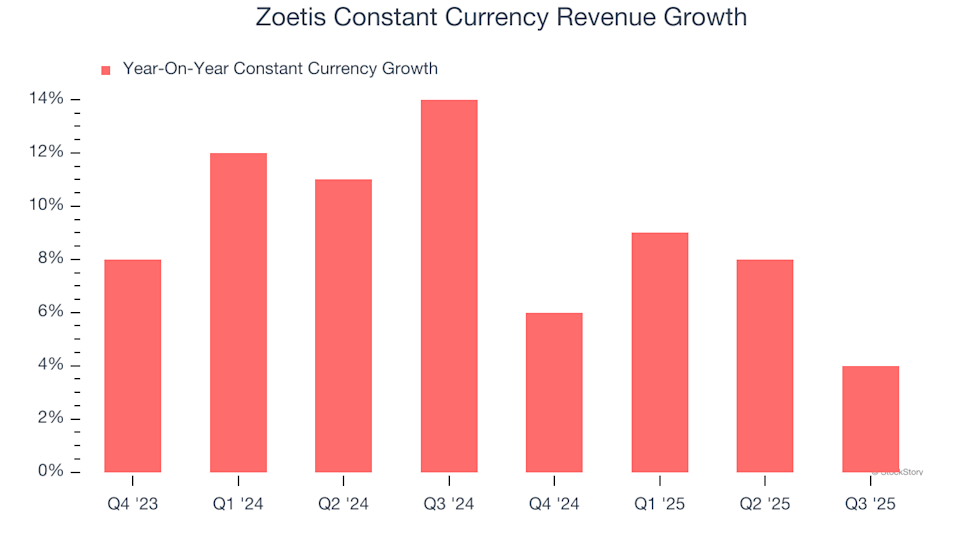

2 Reasons to Appreciate ZTS (and 1 Reason for Caution)

Diversified Energy TR-1

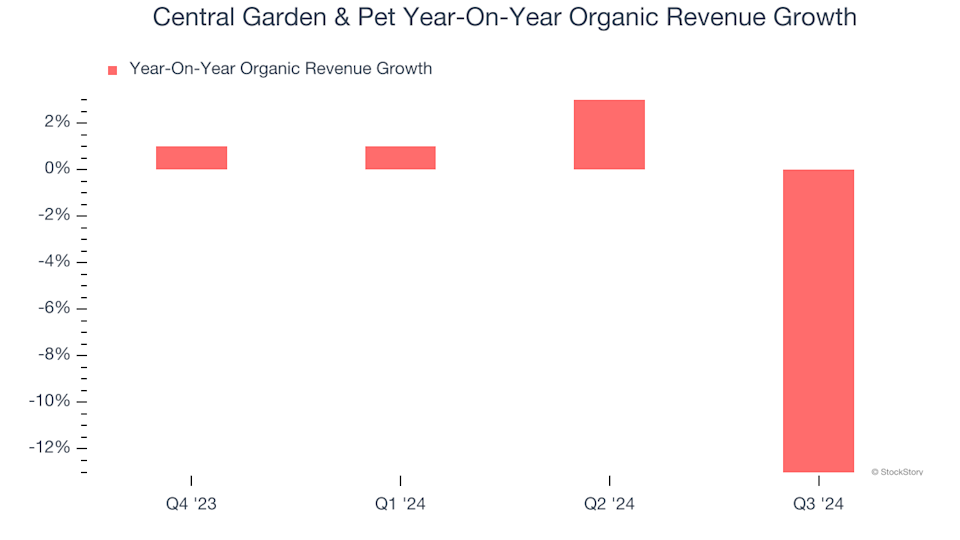

Central Garden & Pet (CENT): Should You Buy, Sell, or Hold After Q4 Results?