Phathom's Fourth Quarter Outperformance: Did the Market Anticipate the Growth?

Market Reaction: Was Growth Already Anticipated?

Phathom’s fourth-quarter performance raised a key question for investors: had the company’s growth already been factored into its share price? Although the results surpassed expectations, the market’s muted response indicated that the outcome was largely anticipated.

For the fourth quarter, $57.6 million in net revenue was reported, slightly ahead of the $57.05 million consensus. The margin of outperformance was slim—just over half a million dollars. For the full year, revenue reached $175.1 million, also narrowly beating the expected $174.36 million. This pattern of modest outperformance is not new; in the previous quarter, Phathom delivered an EPS beat of 63.41%, yet the stock still declined, suggesting strong results were already reflected in the price.

This dynamic has played out in the stock’s recent trajectory. Over the last 20 days, PHAT shares have dropped 13.42%, despite the company exceeding both quarterly and annual revenue forecasts. This is a textbook example of “sell the news”—the market had already priced in a robust finish to 2025, and the actual results were not enough to lift expectations further. It’s possible that internal expectations were even higher than the official consensus, but the reported numbers didn’t clear that higher bar.

In summary, the company’s growth was widely expected. The slight beat did little to surprise investors, and the stock’s decline reflects a forward-looking market that had already anticipated positive news.

2026 Guidance: Ambition Meets Skepticism

Phathom’s management has set a bold target for 2026, but analysts remain cautious. The company is forecasting net revenues between $320 million and $345 million for the year, representing an approximate 80% increase from 2025. Achieving this would require sustained commercial momentum and a clear path to profitability, with management aiming for operating profits starting in the third quarter of 2026.

However, analyst sentiment has softened. Over the past three months, consensus estimates for 2026 revenue have dropped from $316.86 million to $314.48 million. This creates a gap between management’s optimistic guidance and the market’s more conservative outlook. The company’s projections exceed the lowered consensus, setting up a scenario where management is promising to outperform expectations that have already been revised downward.

The most ambitious aspect of the plan is the goal to achieve operating profitability by Q3 2026—just 11 months after reporting a GAAP net loss of $221.2 million in 2025. This will require not only strong revenue growth but also tight control over non-GAAP operating expenses, which are projected to be $235–$250 million. The company’s aim to reach positive cash flow in 2027 adds further complexity, signaling a period of reinvestment before achieving financial independence.

Ultimately, there is a clear tension between management’s confident outlook and the market’s growing doubts. The guidance range is wide, but its midpoint sits above current expectations. The central question is whether investors will embrace the company’s optimistic timeline, or if the recent decline in consensus estimates reflects deeper concerns about execution.

Financial Health: Impressive Growth, Persistent Cash Burn

While Phathom’s revenue growth is notable, the company continues to burn through cash at a significant rate. For the full year, Phathom posted a GAAP net loss of $221.2 million. Although this loss narrowed compared to the previous year, the business remains far from profitability. The cash position is particularly concerning: cash and equivalents dropped to $130 million at year-end, down from $297.3 million a year earlier, highlighting the disconnect between revenue growth and cash generation.

To address this, management completed a $130 million equity offering in January and restructured its term debt in February, reducing the principal and extending maturity to 2029. These moves have strengthened the capital structure but also underscore the company’s reliance on external funding as it works toward profitability.

The feasibility of the 2026 targets depends on Phathom’s ability to rein in cash burn. Achieving operating profitability by Q3 2026 and positive cash flow in 2027 will require a substantial improvement in operating margins. With non-GAAP operating expenses expected to remain high, revenue growth must accelerate further to cover costs. The recent cash depletion suggests the company’s financial runway is limited, and investors will be watching closely to see if Phathom can deliver on its cost management and commercial execution.

Key Catalysts and Risks on the Road to Q3 2026

Phathom’s journey to profitability is now defined by several near-term milestones. The most critical is achieving operating profitability by the third quarter of 2026. Meeting this target would validate management’s strategy, likely boost market confidence, and could drive the stock higher.

The main risk is the company’s cash burn and the need to reach positive cash flow in 2027 to avoid further dilution. With cash reserves already down sharply from nearly $300 million to $130 million, recent financing and debt restructuring have helped, but the company still needs to generate cash from operations. The market will be focused on whether revenue growth can outpace high operating expenses, allowing Phathom to hit its 2027 cash flow goal without another capital raise.

- Prescription Growth: Continued momentum for VOQUEZNA prescriptions is essential. The company has surpassed 1.1 million total prescriptions, but sustaining 217% year-over-year revenue growth will require deeper engagement with gastroenterologists.

- Sales Force Effectiveness: Management reports the sales team is now over 95% staffed, but the challenge is to translate this into consistent prescription growth.

In summary, Phathom faces a binary outcome. The catalyst is clear: achieve profitability by Q3 2026. The risk is that the company’s cash reserves may not last if execution falters. The stock’s future will depend on whether Phathom can transform its commercial momentum into a sustainable financial model before its capital buffer is depleted.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Arcutis Management to Present at TD Cowen's 46th Annual Health Care Conference

NVIDIA vs. Broadcom: The Smarter AI Stock to Buy for March 2026

TRG Latin America Acquisitions Corp. Completes $200 Million Initial Public Offering

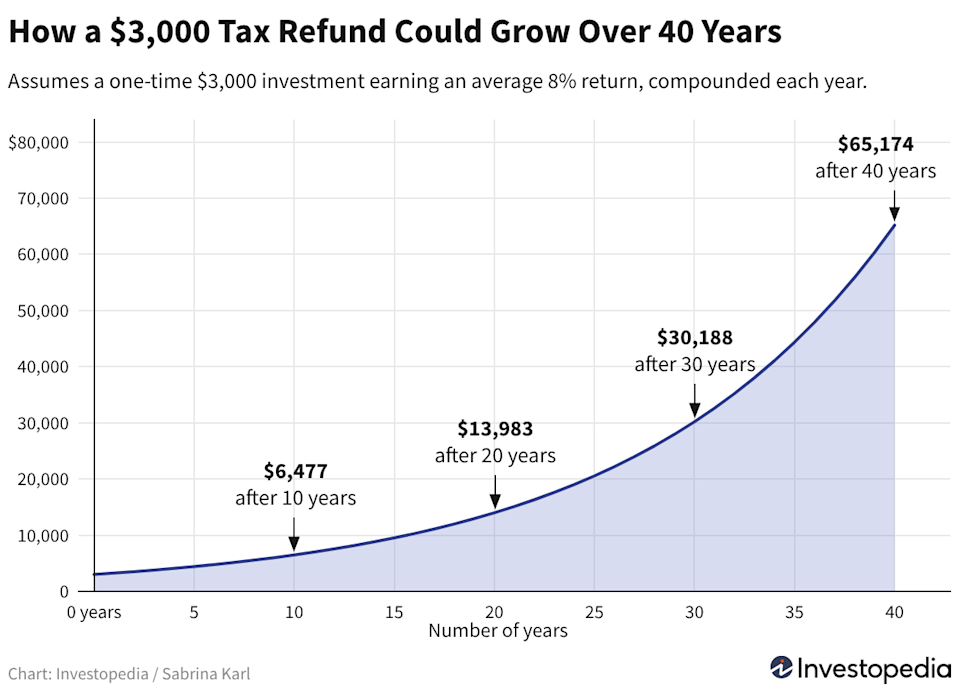

That $3,000 tax return might have a greater impact on your retirement than you realize