That $3,000 tax return might have a greater impact on your retirement than you realize

Main Insights

-

Investing a single $3,000 tax refund at an 8% annual return could potentially grow to around $65,000 over four decades, thanks to the power of compound interest.

-

Making a habit of investing your refund each year can have an even greater effect, possibly resulting in a retirement fund worth six figures over time.

-

Roth IRAs, Traditional IRAs, and 401(k) plans each provide unique tax benefits for investing your refund.

For many Americans, tax season isn’t just about forms—it’s about the anticipation of a refund. Last year, the average federal refund exceeded $3,100, making it one of the largest single cash infusions many families receive annually.

Receiving this money can offer relief—a chance for a trip, a home upgrade, or catching up on expenses.

However, there’s another path: using your refund to boost your retirement savings. The choice isn’t just between spending and saving; it’s about weighing immediate gratification against the long-term benefits of compounding, which can significantly enhance your financial well-being.

The Impact on Your Financial Future

A $3,000 refund can be spent quickly, or it can quietly accumulate wealth over decades. The outcome depends on what you choose to do each year.

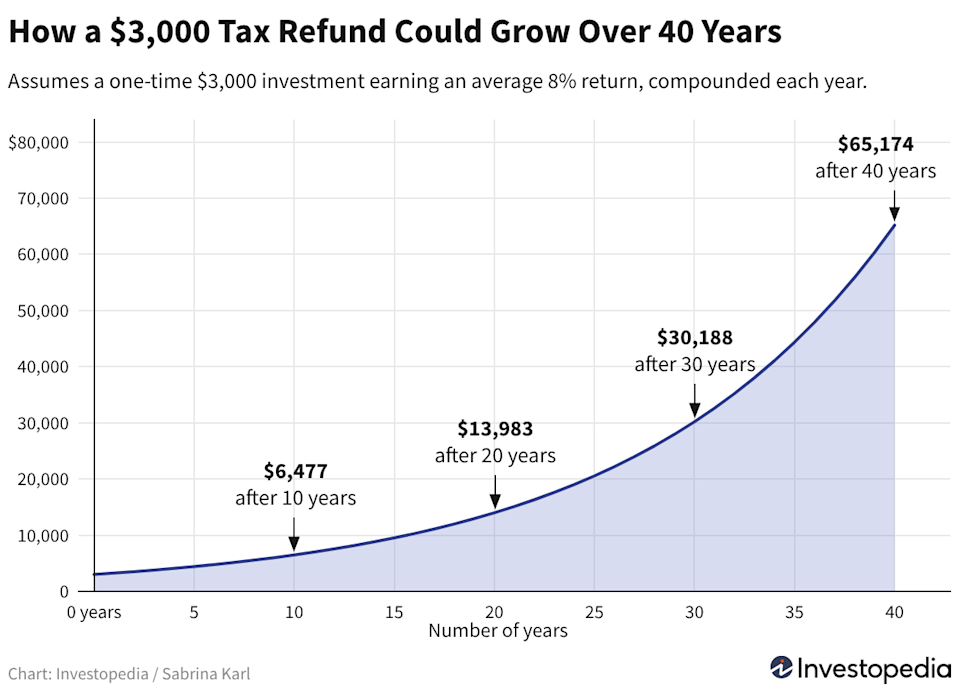

Potential Growth of a $3,000 Refund at 8% Return

Suppose you invest $3,000 and achieve an average annual return of 8%. While market returns fluctuate, 8% is a commonly used estimate for a diversified, stock-heavy portfolio, reflecting the long-term performance of the U.S. stock market.

As illustrated below, growth starts slowly but accelerates over time. After 20 years, your $3,000 could become roughly $14,000. If left untouched for 40 years, it could surpass $65,000.

This rapid increase is due to compounding. In the early years, your returns are modest, but as time passes, your earnings generate their own earnings, causing your balance to grow more quickly.

Even smaller refunds can make a difference. For example, investing $1,000 at 8% annually could grow to about $21,725 in 40 years, while $5,000 could exceed $108,000. The most important factor is time—the sooner you invest, the longer compounding can work for you.

What Happens If You Invest Your Refund Every Year?

Now, imagine you invest $3,000 from your refund each year instead of just once.

Assuming the same 8% average return, the chart below shows how consistent annual contributions can accumulate. After 20 years, your yearly $3,000 investments could total over $151,000. Over 40 years, your balance could grow beyond $842,000.

The real difference comes from consistency. Each year’s investment has less time to grow than the first, but together, they build a much larger nest egg.

Investing a single refund is beneficial, but making it an annual practice can lay the groundwork for a significant retirement account.

Keep in mind, though, that 8% returns aren’t guaranteed. Markets can rise or fall in any given year. However, investors who stay diversified and remain invested for the long term have historically benefited from compounding growth.

Changing Your Perspective

It’s easy to view a refund as “bonus” money. But if you plan ahead and treat it as part of your retirement strategy, it becomes a tool for your future rather than just a windfall.

For some, investing the entire refund may not be feasible. Even splitting it—putting half toward investments and using the rest for current needs—can help you make progress without neglecting present obligations.

Where Should You Invest: Roth IRA, Traditional IRA, or 401(k)?

If you choose to invest your refund for retirement, the next step is deciding which account to use.

Roth IRA

A Roth IRA is a good option if you expect to be in a higher tax bracket later. Contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free. This can be especially advantageous for younger workers. Investing your refund in a Roth IRA allows it to grow for decades without future taxes on qualified withdrawals.

Traditional IRA

A Traditional IRA typically provides a tax deduction now, reducing your current taxable income. However, withdrawals in retirement are taxed as ordinary income, making this a tax-deferral strategy. If you expect to be in a lower tax bracket in retirement, this trade-off can be beneficial.

401(k)

If your employer offers a 401(k), you might increase your contributions and use your refund to offset smaller paychecks. This is especially valuable if you’re not contributing enough to receive your employer’s full match. In that case, directing your refund toward retirement could unlock additional employer contributions and boost your compounding potential.

There’s no universal answer—the best choice depends on your current finances and long-term goals.

Final Thoughts

While a tax refund is an annual event, your decision on how to use it can have lasting effects. Whether your refund is $800, $3,000, or $5,000, investing it gives compounding more time to work for you.

There’s nothing wrong with spending your refund. But if retirement is still years or decades away, using that yearly windfall as part of your long-term plan could be one of the simplest ways to steadily build your financial security.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Sluggish Fourth Quarter Expansion and Prospects for Inflation in Switzerland

XRP Price if 30% of XRP Is Staked from Current Circulating Supply

India Gold price today: Gold increases, based on FXStreet data

Australian Dollar closes weekly downward gap as USD pulls back; AUD/USD climbs back above 0.7100