3 Reasons to Steer Clear of QSR and One Alternative Stock Worth Buying

Restaurant Brands: Recent Performance and Investment Outlook

Over the past half-year, Restaurant Brands has mirrored the S&P 500’s upward movement, with its share price advancing 9.4% to reach $68.50, compared to the index’s 7.2% gain.

Is now a good moment to invest in Restaurant Brands, or could it pose a risk to your holdings?

Why We’re Not Enthusiastic About Restaurant Brands

We approach Restaurant Brands with caution. Here are three reasons why we believe investors should be wary of QSR, along with a stock we prefer instead.

1. Modest Revenue Growth Expectations

Wall Street’s revenue forecasts offer a glimpse into a company’s future prospects. While projections aren’t always precise, accelerating growth tends to lift valuations and share prices, whereas decelerating growth can have the opposite effect.

Analysts anticipate Restaurant Brands will increase its revenue by just 4.3% over the coming year—a lackluster outlook that suggests the company’s menu may struggle to attract greater demand.

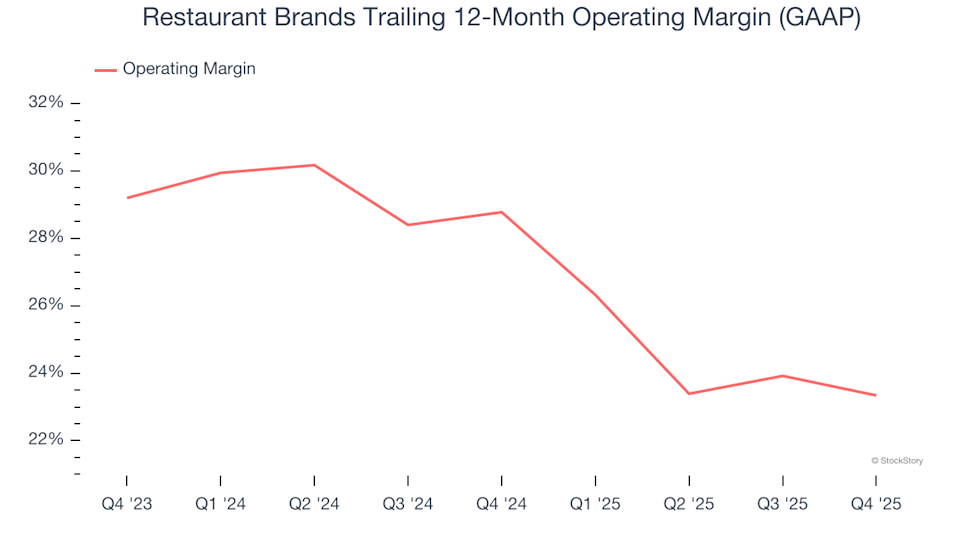

2. Declining Profit Margins

Operating margin is a crucial measure of profitability, reflecting all costs required to keep the business running, such as ingredients, labor, rent, marketing, and administrative expenses.

Examining recent trends, Restaurant Brands’ operating margin dropped by 5.4 percentage points over the past year. This decline is concerning, as higher revenues should have helped the company better absorb fixed costs and improve profitability. Over the last twelve months, its operating margin stood at 23.3%.

3. Stagnant Earnings Per Share Growth

We monitor long-term changes in earnings per share (EPS) to assess whether a company’s growth is translating into higher profits for shareholders.

Restaurant Brands’ EPS has grown at a modest 5.1% compound annual rate over the past six years, trailing its 9.1% annualized revenue growth. This indicates that, as the company expanded, its profitability per share diminished.

Our Verdict

While Restaurant Brands is not a poor business, it doesn’t meet our investment criteria. The stock currently trades at a forward price-to-earnings ratio of 16.7 (or $68.50 per share), which is reasonable, but we lack conviction in the company’s future. We believe there are better opportunities available and suggest considering one of our top software stock picks instead.

Resilient Stocks for Every Market Environment

Building your portfolio on outdated trends can be risky, especially as certain crowded stocks become increasingly volatile.

Discover the Next Generation of Market Leaders

The companies poised for substantial growth are featured in our Top 5 Strong Momentum Stocks for this week. This handpicked selection of high-quality stocks has delivered an impressive 244% return over the past five years (as of June 30, 2025).

Our list includes well-known names like Nvidia, which soared 1,326% from June 2020 to June 2025, as well as lesser-known companies such as Comfort Systems, which achieved a 782% five-year return. Start your search for the next breakout stock with StockStory today.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Top 5 Altcoins Printing 1000x Gains Despite Market Dumps — YTD Winners Worth Watching

Imperium Labs and MSV Protocol Forge Strategic Partnership to Bridge Real-World Assets with Decentralized Finance

China Approaches Final Stages of the World’s Biggest Pumped Hydroelectric Storage Project

Why did Netflix decide not to proceed with its acquisition of Warner Bros.?