Berkshire Hathaway's Most Recent Purchases During Warren Buffett's Tenure as CEO

Motley Fool Money Podcast Highlights

On this episode, contributors Travis Hoium, Lou Whiteman, and Rachel Warren cover several key topics:

- Berkshire Hathaway’s investment activity prior to Warren Buffett’s departure.

- Current trends in the homebuilding sector.

Note: This discussion was recorded before Netflix withdrew its offer for Warner Bros. Discovery.

Full transcript below.

Warren Buffett’s Final Moves at Berkshire Hathaway

Recorded on February 18, 2026.

Travis Hoium: This week, we got a look at Warren Buffett’s last stock purchases before stepping down. What did his final decisions reveal? Welcome to Motley Fool Money. I’m Travis Hoium, joined by Lou Whiteman and Rachel Warren. As recent filings show, we’re seeing which stocks major funds and corporations held at the close of 2025. Notably, Warren Buffett added shares of the New York Times and Chubb. Lou, what insights can we draw from these filings, and how does Berkshire’s strategy look now that Greg Abel is officially at the helm?

Lou Whiteman: It’s important to remember that Berkshire’s investment decisions aren’t made by one person alone, though Buffett is certainly kept in the loop. The recent shift from tech stocks to media is a classic move for a mature portfolio. Greg Abel now faces the challenge of managing a company so large that even significant investments barely make a dent in overall performance. Even a major stake in a company like GameStop during its meme stock surge wouldn’t have moved the needle for Berkshire. The conglomerate’s sheer size limits its ability to generate outsized returns, and with Buffett no longer the shield, the pressure is on to deliver results. The question remains: how can Berkshire continue to outperform the market when even trades involving giants like Apple have minimal impact?

Travis Hoium: To put some numbers to it, Berkshire Hathaway trimmed its Apple holdings by 4.3% and reduced its Amazon stake by 77%. On the buying side, they picked up shares in Liberty Media, the New York Times, Domino’s Pizza, Chubb, and Chevron. It’s a diverse mix, and interestingly, some of these traditional businesses may be outperforming tech stocks so far in 2026.

Rachel Warren: It’s fascinating to see Buffett’s last moves as CEO, which really reflect his value-driven approach. While he focused on stock selection, Greg Abel is known for his operational expertise. Investors may see a greater emphasis on growing Berkshire’s operating businesses rather than dramatic changes to the investment portfolio. The core pillars—insurance, railroads, energy, and Apple—remain, and with over $380 billion in cash, Abel has significant flexibility. We might see more activity in industrial and infrastructure sectors, areas where Abel has deep experience. There are hints that Abel could be more decisive in exiting underperforming legacy positions, such as the potential sale of the long-troubled Kraft Heinz stake.

Lou Whiteman: That particular filing came after the quarter ended, so it wouldn’t appear in the latest reports.

Rachel Warren: Exactly. As we move into upcoming quarters, we’ll likely see Abel put his own stamp on Berkshire’s strategy. Buffett remains chairman, so his influence on major capital decisions will persist for now. Still, investors are curious whether Abel will introduce a dividend or make other significant changes. Expectations are high for his leadership.

Travis Hoium: With Berkshire valued at around $1.1 trillion and holding roughly $380 billion in cash, what should their capital allocation strategy be going forward?

Lou Whiteman: That’s a substantial reserve. I believe Berkshire can maintain a large cash buffer for future opportunities while also starting to pay a dividend. A dividend could be well received by the market. While buybacks are possible, they’re less likely to have a major effect given Berkshire’s scale. Buffett has long credited his team for investment decisions, and as chairman, his presence will still be felt. The bigger question is how Berkshire can continue to deliver market-beating returns. A combination of growth and income, including a dividend, may be the way forward.

Travis Hoium: We’ve seen major shifts after founders leave, like when Tim Cook took over from Steve Jobs at Apple and began returning capital to shareholders. Berkshire could easily afford a 5% dividend yield for a decade, or even more if they chose.

Lou Whiteman: Most of Berkshire’s peers in insurance, railroads, and aerospace pay dividends, and doing so wouldn’t significantly deplete their cash reserves. It’s a logical next step.

Streaming Industry Shake-Up: Netflix, Warner Bros. Discovery, and Paramount

Travis Hoium: Next, let’s discuss the ongoing saga involving Warner Bros. Discovery and Netflix. Paramount is still pursuing an acquisition of Warner Bros. Discovery. Rachel, what’s the latest as of now?

Rachel Warren: The situation is evolving quickly. Netflix granted Warner Bros. Discovery a seven-day window for Paramount to submit their final offer by February 23rd, with a board vote scheduled for March 20th. Despite renewed talks, the board still favors the Netflix merger, and Netflix retains the right to match or exceed any Paramount bid. Netflix is interested in acquiring the studios and HBO, planning to spin off the cable channels. Paramount’s bid stands at $108 billion, or $30 per share in cash, and they may go as high as $31 per share. They’ve also offered a $2.8 billion breakup fee to Netflix. Paramount’s offer is backed by Larry Ellison of Oracle, Red Bird Capital, and several Middle Eastern sovereign wealth funds. However, the deal is heavily leveraged, which raises concerns. Netflix remains the frontrunner unless Paramount significantly sweetens its proposal. Warner Bros. may be allowing Paramount to bid again to avoid legal challenges over fiduciary duties. The outcome remains uncertain.

Lou Whiteman: Nothing fundamental has changed—Netflix is still in the driver’s seat. Paramount has been vocal about the process, but Netflix holds significant advantages, including the right of first refusal. They could also partner with Comcast to handle the cable assets. Given Netflix’s size, they can outbid Paramount with less financial strain. Regulatory approval and the stability of Paramount’s backers, especially with Oracle’s stock under pressure, are also factors the Warner Bros. Discovery board must consider.

Travis Hoium: There are creative options, like giving Comcast access to Warner Bros. Discovery content. Ultimately, Netflix’s larger scale gives it more flexibility to increase its offer if needed. The board must also weigh the reliability of Paramount’s financing, especially if Oracle’s stock continues to decline.

Lou Whiteman: Paramount has agreed to pay a monthly fee to Warner Bros. Discovery shareholders if the deal drags past the end of 2026, but the uncertainty remains. The high debt load in Paramount’s bid could actually help Netflix’s case with regulators, as it limits future investment in programming. Netflix simply has more resources to bring to the table.

Travis Hoium: Netflix’s stock has also faced a 42% decline. If the deal falls through, it might even benefit Netflix’s share price in the short term. We’ll keep an eye on how this unfolds. Up next, we’ll look at the housing market.

Homebuilder Update: Toll Brothers and the Luxury Housing Market

Travis Hoium: Turning to real estate, Toll Brothers, a major U.S. homebuilder, just reported earnings. Rachel, what did their results reveal about the current housing landscape?

Rachel Warren: Toll Brothers primarily serves the luxury segment, making them a good indicator for that market. In their Q1 2026 report, they exceeded expectations despite a mixed environment. Although they delivered fewer homes, their focus on high-end buyers and strategic land sales led to double-digit revenue and profit growth. Earnings per share reached $2.19 on $2.2 billion in revenue, and the average price of homes in their backlog rose to $1.2 million. They’re selling their apartment living portfolio to Kennedy Wilson for $330 million, exiting the multifamily sector to concentrate on luxury homes. While contract values increased slightly, the number of units in backlog dropped 20% year-over-year. Wealthier buyers are less affected by high interest rates—28% pay cash, and those with mortgages have a low loan-to-value ratio. The luxury market is being fueled by generational wealth transfers, creating a pool of cash-rich buyers. Even their first-time buyers are typically older and more affluent. Despite building fewer units, rising prices are driving revenue and profits.

Lou Whiteman: Does this reflect the “K-shaped” economy you often mention?

Travis Hoium: It certainly seems that way. The high-end market is holding up better, but even there, contract signings are down. Homebuilders face rising costs, and their main lever is to raise prices. However, there may be limits to how much even luxury buyers are willing to pay. Any weakness at the top end could signal broader economic concerns.

Lou Whiteman: The fact that Toll Brothers is building fewer homes in 2026 than in 2025, despite widespread calls for more housing, is worrisome. It suggests demand is softening, even among affluent buyers.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Pound Sterling weakens to near 1.3300 as geopolitical risks bolster US Dollar

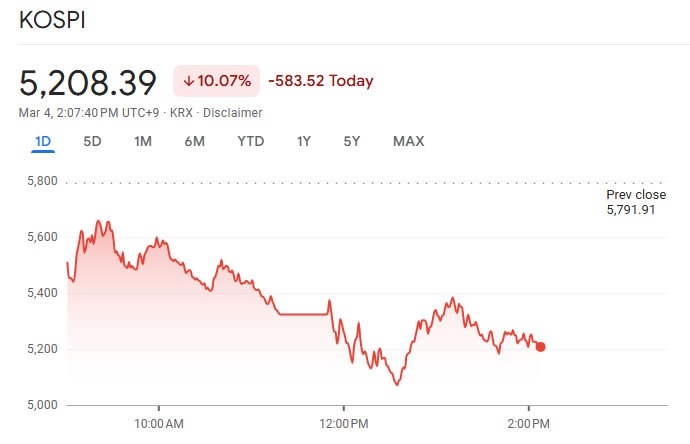

Korea halts trading as key indexes drop 10% on Middle East crisis

DigitalOcean's Agentic Inference Cloud: Creating the Infrastructure for Deploying AI in Production