Progressive Posts Robust Earnings Despite 0.12% Share Decline; $550M Trading Volume Places It at 242nd

Overview of Market Activity

On March 2, 2026, shares of The Progressive Corporation (PGR) experienced a slight dip of 0.12%, despite the company reporting impressive financial results for the year-end. Trading activity was subdued, with volume decreasing by 22.88% from the prior session and a total of $550 million in shares exchanged, ranking PGR 242nd in market volume for the day. This minor decline in share price stands in contrast to Progressive’s strong performance, which included $11.54 billion in parent company revenue and $11.31 billion in net income for the fiscal year ending December 31, 2025. The divergence between robust earnings and stock movement indicates investors may be exercising caution due to broader market trends or industry-specific challenges.

Main Influences on Performance

Progressive’s annual report for 2025 highlighted solid profitability, largely fueled by $10.15 billion in dividends from its subsidiaries and ongoing operational enhancements. Leadership credited revenue gains to heightened demand for its core insurance offerings and a strategic pivot toward digital and direct-to-consumer sales, reducing dependence on wholesale channels. These efforts reflect industry-wide shifts toward greater efficiency and technology-driven customer acquisition. However, the company’s undistributed subsidiary income of $1.22 billion pointed to some cash flow limitations from affiliate operations, which may have dampened investor enthusiasm regarding liquidity.

Operational hurdles also played a significant role in the stock’s lackluster performance. In the third quarter of 2025, Progressive missed analyst expectations, reporting earnings per share (EPS) of $4.45—an 11.88% shortfall—and revenue of $21.38 billion. This earnings miss triggered a 7.76% decline in pre-market trading, signaling investor disappointment. Company executives cited external challenges such as legal reforms in Florida, escalating vehicle repair expenses, and competitive pricing pressures as major obstacles. These factors complicate Progressive’s efforts to implement substantial rate hikes without negatively impacting policyholder growth, a delicate balance for insurers facing high claim severity.

Persistent underwriting challenges continue to influence investor sentiment. Rising claim costs, driven by medical inflation, increased litigation, and higher repair expenses, have compelled Progressive to focus on raising rates rather than expanding policy volumes. Although the combined ratio improved to 89.5% in the third quarter of 2025, experts caution that ongoing profitability will depend on the company’s ability to sustain these rate increases and effectively manage risk. Progressive’s initiatives in commercial insurance and data analytics, while promising, require considerable investment and may not yield immediate results.

From a technical perspective, PGR’s stock remains under pressure. It has traded below its 200-day moving average since early July 2025 and has lagged behind the State Street Financial Select Sector SPDR Fund (XLF) by 6.2% over the past year. The stock’s 27.1% drop from its 52-week high and a 12.7% decline over six months highlight ongoing concerns about sector profitability. Despite a “Moderate Buy” consensus from 25 analysts and an average price target of $247.48—representing a 15.8% upside from current levels—technical signals point to continued volatility amid unresolved underwriting and economic risks.

Outlook

In summary, Progressive’s strong core earnings and digital advancements offer long-term potential, but ongoing challenges in claims management, pricing strategies, and market conditions are likely to continue weighing on investor sentiment in the near future.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

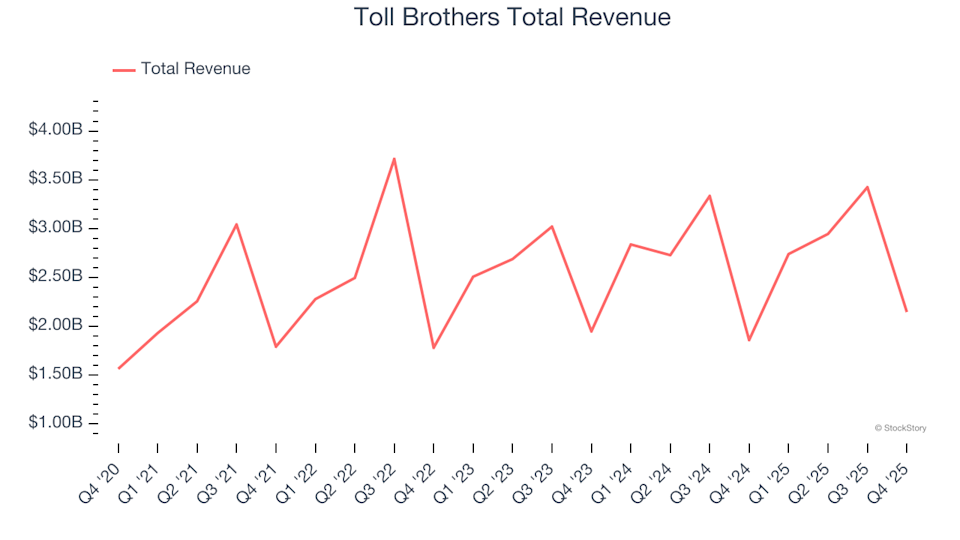

Q4 Top Earnings Performers: Toll Brothers (NYSE:TOL) and Other Leading Home Builder Stocks

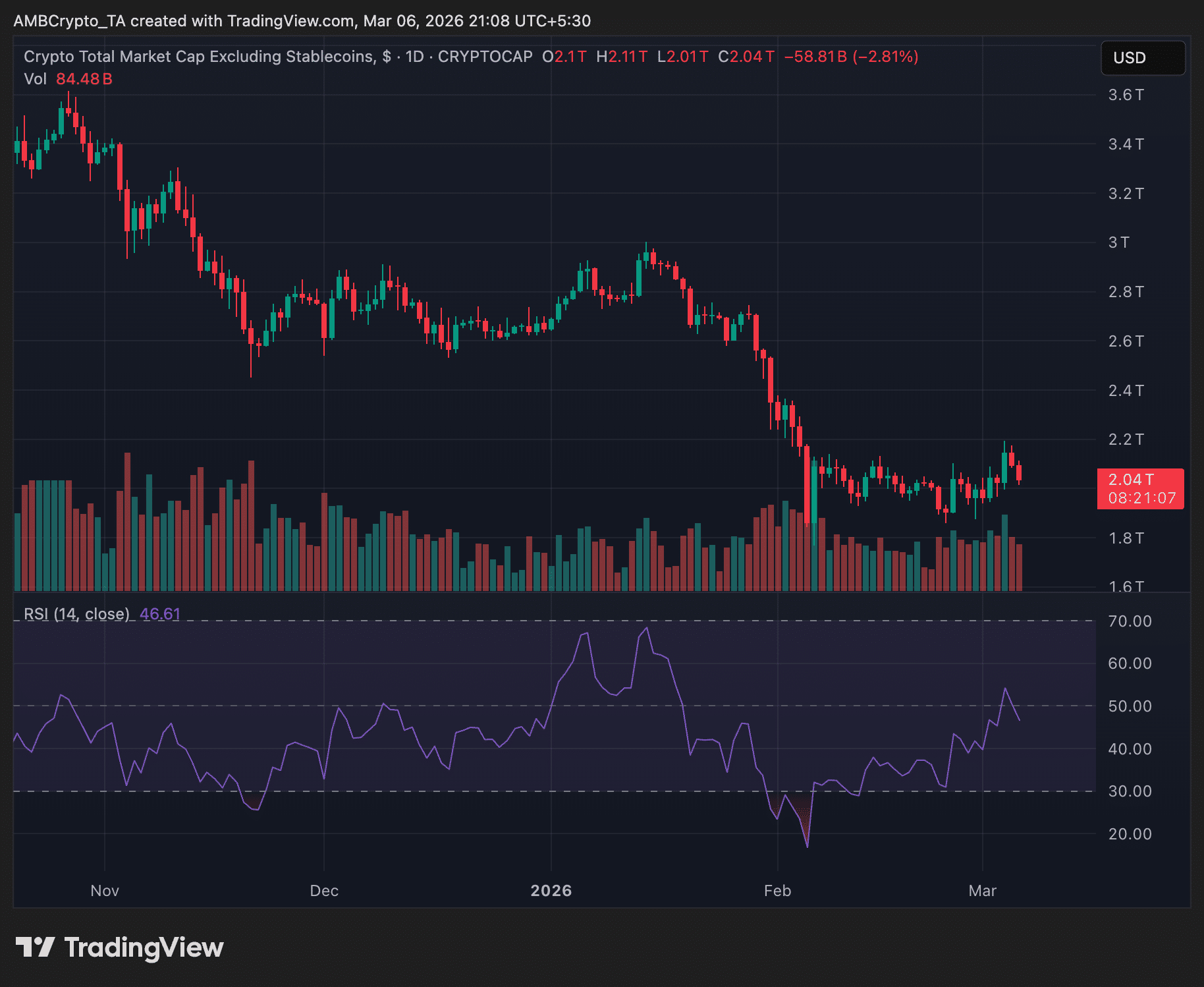

Crypto market holds $2T after U.S. jobs unexpectedly fall by 92K

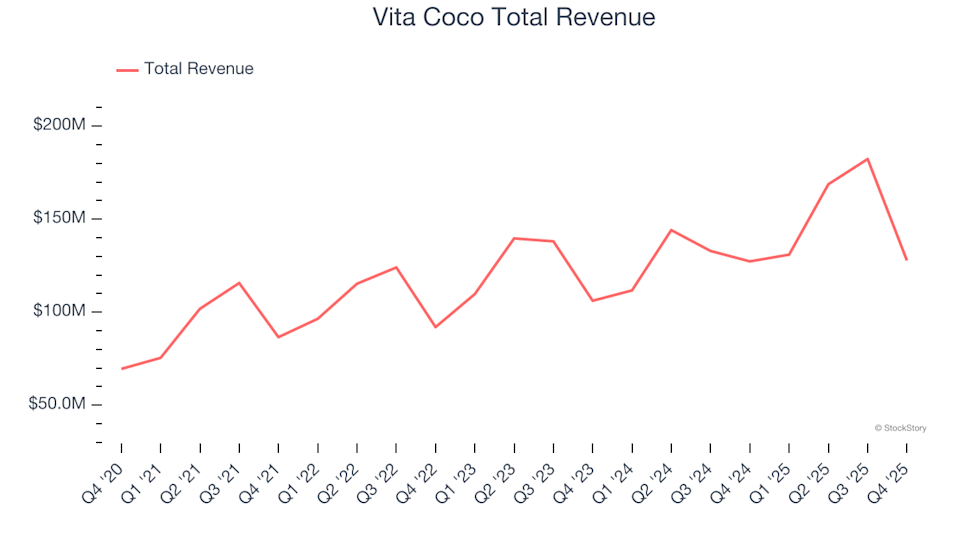

Q4 Top Performers: Vita Coco (NASDAQ:COCO) and Other Leading Beverage, Alcohol, and Tobacco Stocks

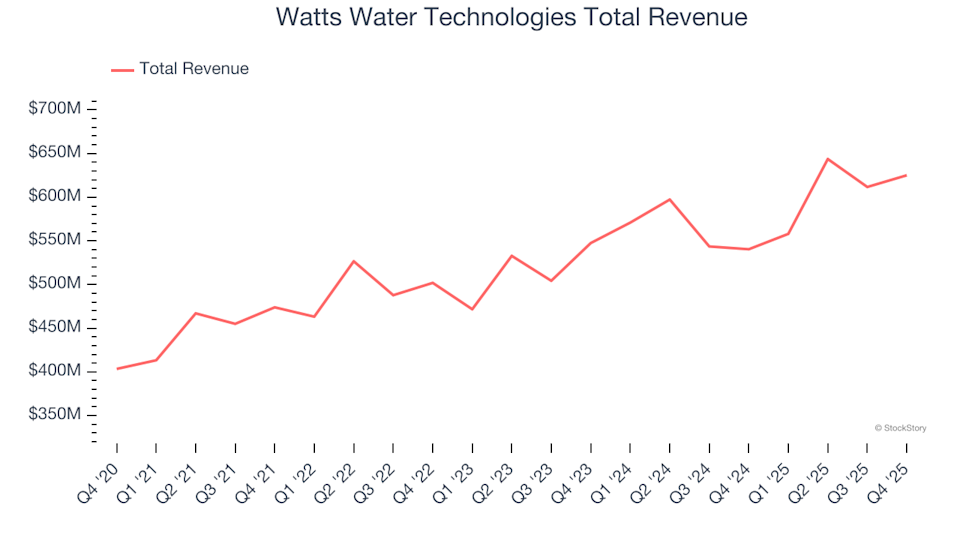

Water Infrastructure Q4 Results: Watts Water Technologies (NYSE:WTS) Stands Out as the Top Performer