DraftKings Slumps to 425th in Volume Amid Strategic Pivot to $55B–$80B Market

Market Snapshot

DraftKings (DKNG) posted a marginal decline of 0.08% on March 2, 2026, with a trading volume of $0.32 billion, marking a 24.76% drop from the prior day’s activity. The stock ranked 425th in volume among U.S. equities, reflecting subdued investor interest despite the company’s recent strategic announcements. While the price movement was minimal, the sharp contraction in volume suggests mixed sentiment among traders, potentially linked to the broader market’s volatility and the company’s ongoing challenges balancing growth initiatives with operational execution.

Key Drivers

DraftKings unveiled an expanded growth strategy targeting a $55 billion to $80 billion industry gross revenue opportunity by 2030, driven by state-level legalization of sports betting and casino operations, as well as the expansion of its federally regulated DraftKingsDKNG-0.08% Predictions platform. This initiative aims to capture nearly the entire U.S. population by offering event contracts in states lacking regulated online wagering, a key differentiator in an increasingly competitive market. The company emphasized that this growth framework is underpinned by its ability to leverage existing infrastructure and regulatory partnerships, including its No. 1-rated sportsbook, to scale efficiently.

Central to the strategy is the launch of a unified "Super App" branded as DraftKings Sports & Casino, integrating sports betting, predictions, casino, and lottery services into a single, jurisdiction-tailored platform. The app is designed to enhance user engagement through a seamless experience, leveraging DraftKings’ established brand equity and technological infrastructure. Phase one of the rollout is slated for the March Madness tournament, with incremental upgrades planned throughout 2026. The company anticipates this integration will strengthen cross-selling, deepen customer relationships, and optimize unit economics, particularly through AI-driven personalization and operational efficiency.

The strategic pivot toward AI deployment is another critical component of DraftKings’ long-term vision. Management highlighted increased use of artificial intelligence across the platform to drive cost efficiencies, improve customer targeting, and accelerate innovation in product development. These advancements are expected to bolster the company’s "lifetime value flywheel," a model that combines product quality, technology, trust, and marketing to sustainably increase customer lifetime value. By automating processes and refining user experiences, DraftKings aims to reduce customer acquisition costs while enhancing retention, a vital metric in the high-churn gaming sector.

Financially, the company outlined ambitious margin expansion targets, aiming for at least 30% Adjusted EBITDA margins in the long term, with potential for upside as scale grows. This guidance hinges on the successful execution of the Super App and AI initiatives, which are projected to reduce operational costs and unlock new revenue streams. However, investors remain cautious about short-term hurdles, including regulatory uncertainties, legal challenges, and the company’s recent underperformance relative to peers. The modest stock price decline, despite the bullish revenue outlook, may reflect skepticism about the timeline and feasibility of achieving these margin goals, particularly in a sector marked by high capital expenditures and regulatory risks.

The mixed investor reaction underscores the tension between DraftKings’ long-term ambitions and its near-term execution challenges. While the $55B–$80B revenue opportunity and margin targets signal confidence in the company’s strategic direction, the stock’s muted performance and declining volume suggest that market participants are awaiting concrete progress on key initiatives. The Super App’s successful rollout, coupled with measurable improvements in unit economics and regulatory clarity, will likely determine whether the market revalues the stock higher in the coming quarters. For now, the focus remains on whether DraftKings can translate its expansive vision into tangible, scalable growth without overextending its operational and financial resources.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

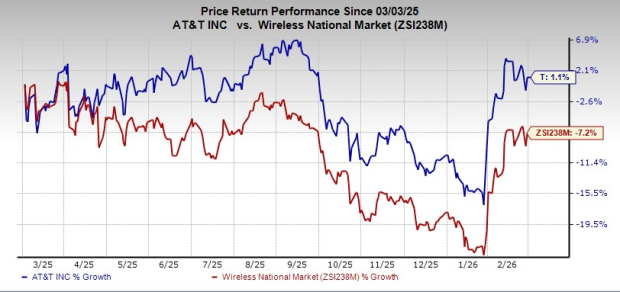

T Unveils Intelligent Manufacturing Solution: Can It Enhance Future Growth?

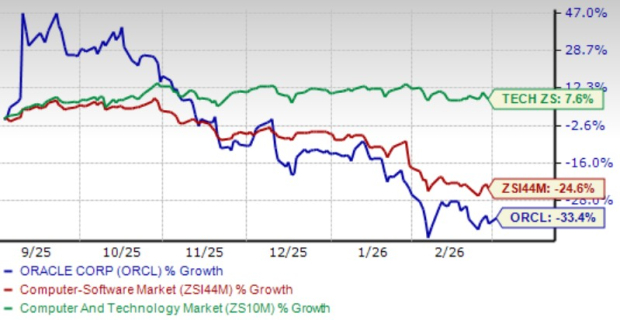

Oracle’s AI Pipeline Expands: Can Continued Growth Be Expected?